Update: 9 August 2021

A reminder to shareholders who are voting for the CapitaLand resolutions that the date and time for the EGM and Scheme Meeting are 10 August at 2:00 p.m. and 2:15 p.m., respectively.

If approved, CapitaLand’s shares will go “ex” on 3 September and the cash consideration will be paid out on 16 September.

The crediting for CapitaLand Investment Management and CapitaLand Integrated Commercial Trust shares will also be done on 16 September.

————————————————————–

Around four months ago, CapitaLand Limited (SGX: C31) surprised the market with a proposal to privatise its property development arm to restructure itself into a real estate investment manager (REIM).

This move will split the company into two, with the development division fully owned by CLA Real Estate, a unit of Temasek Holdings.

CapitaLand’s investment division will be separately spun off as “CapitaLand Investment Management” or CLIM and will be listed on the Singapore stock exchange.

The group has provided a more comprehensive presentation on the benefits of this corporate action, as well as a definitive timeline on when this will take place.

Here are five benefits that investors can expect.

1. Healthy growth potential in Asia

The spin-off of CLIM will create a global REIM with a presence in more than 30 countries and over 230 cities.

CapitaLand’s core markets remain Singapore, China and India, and the group is present in the five key verticals of retail, integrated developments, office, lodging and new economy.

The group’s strength remains in Asia, as it has around 87% of its assets under management (AUM) and 85% of its funds under management (FUM) in Asia.

CLIM’s future growth is backed by interest from institutional investors who have steadily increased their allocation to real estate in Asia over the last eight years.

In 2013, this allocation stood at 8.9% but has since grown to 10.6% by 2020 and is expected to hit 10.9% this year.

2. Scaling up fee income

CapitaLand currently has two platforms for fee income generation — its fund management platform, consisting of listed and unlisted funds, and its lodging management platform.

The fund management arm has access to numerous opportunities by tapping on the group’s global platform.

The lodging arm intends to diversify into adjacent sectors such as purpose-built student accommodation (PBSA) and multi-family asset classes.

Its business is also global and consists of reputable brands such as Citadines, Somerset and Ascott.

Together, these two platforms can ramp up CapitaLand’s recurring fee income by scaling up their fee-generating AUM.

Both divisions have a healthy growth track record.

FUM had grown from S$46 billion in 2015 to S$78 billion by 2020, including S$18 billion in new economy funds, a new category not present five years ago.

Lodging’s AUM experienced an impressive 20% per annum growth from 72,000 units in 2017 to 123,000 units in 2020.

For FUM, the fee-related earnings amount to around 0.4% of the funds’ value while for lodging, it is 0.7% of the operational units under management.

3. Nurture the growth of listed and unlisted funds

CapitaLand has adopted a disciplined approach to investing and has designated three strategic growth areas for its fund management strategy.

These are new economy (primarily comprising data centres, logistics and business parks), commercial and integrated developments, and lodging.

These funds consist of a mix of both listed and unlisted funds, with the intention of nurturing growth in both.

CapitaLand currently has more than 20 active unlisted funds with diversified themes, vintages and fund structures.

Unlisted FUM has grown from S$20.8 billion in 2016 to S$25.8 billion in 2020.

The recent announcement of the launch of its second India Logistics Fund adds yet another feather to CapitaLand’s cap by contributing to the further growth of its unlisted FUM.

The group has been active in acquisitions for its listed REITs such as Ascendas REIT (SGX: A17U) and Ascott Residence Trust (SGX: HMN).

The former had acquired the remaining 75% stake in Galaxis back in May, while the latter had concluded the purchase of three freehold rental housing properties in Japan last month for S$85.2 million.

4. Potential re-rating of CLIM

The listing of CLIM may also trigger a re-rating, as the new company has now shed its development arm.

Public markets generally value REIMs differently from developers, as evidenced by the average price to book value (P/B) accorded to REIMs.

The P/B for listed REIMs was around 2.9 times versus just 0.9x for CapitaLand at present.

On a price-earnings basis, REIMs also trade at a slight premium to developers in Asia.

The average forward price to earnings ratio (P/E) of Singapore, Hong Kong and China developers was just 8.7 times versus 21.8 times for listed REIMs.

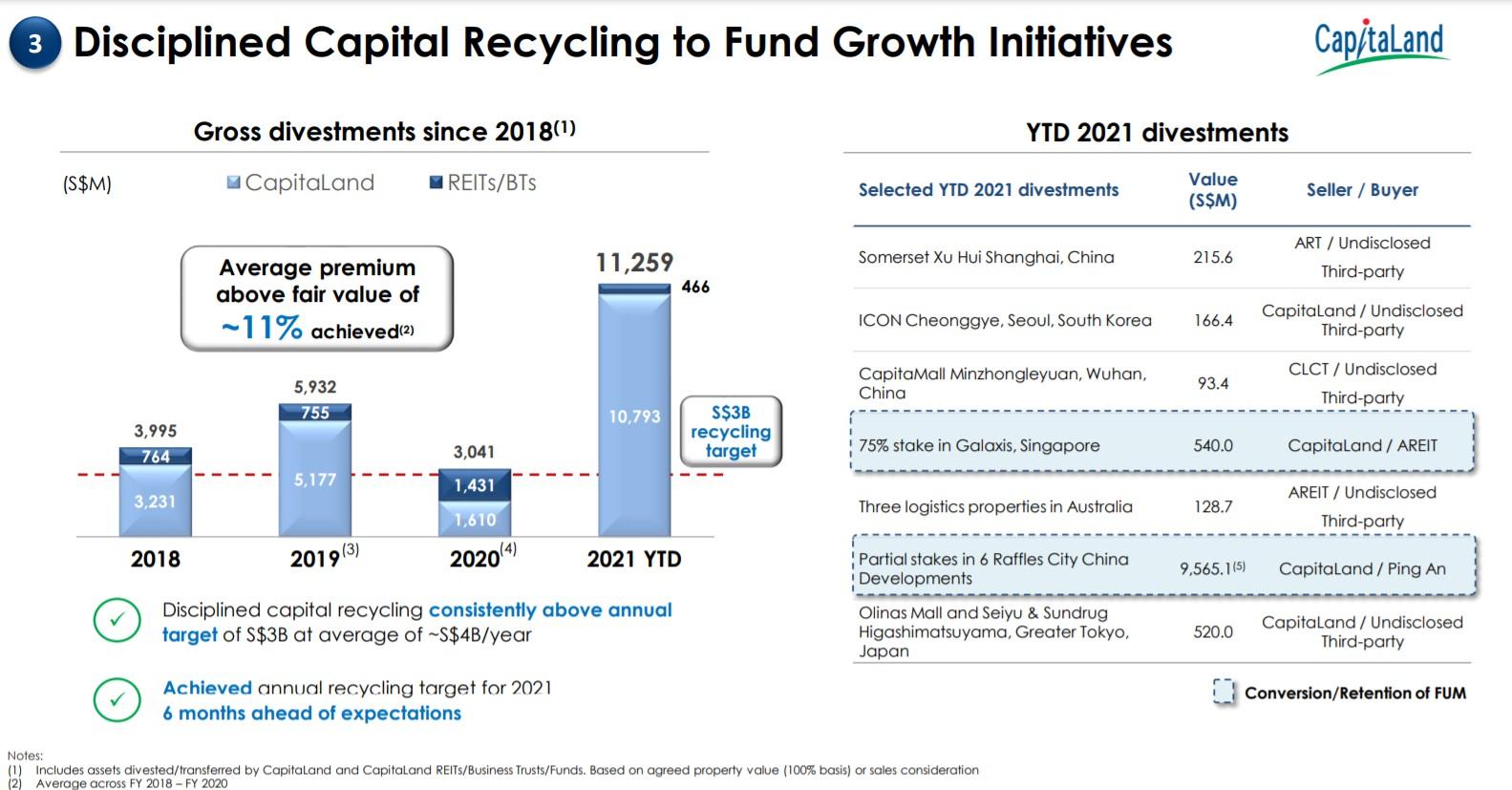

5. Active capital recycling to unlock further value

Source: CapitaLand’s Presentation Slides

CapitaLand is actively recycling capital to maximise value for shareholders.

Since 2018, the group has consistently exceeded its annual S$3 billion target for divestments.

For the 2021 year to date, a total of S$11.2 billion worth of divestments has been conducted, significantly above the S$3 billion target set.

From 2018 to the year to date for 2021, CapitaLand sold its assets at an average premium of 11% above fair value.

In effect, CapitaLand is steadily growing its capital base through targeted divestments.

To add icing to the cake, some of the divestments have also increased FUM as the property stakes are sold to either joint venture partners or REITs.

This could be our riskiest (and weirdest) move in years.

Recently, we polled the public for 3 dividend stocks.

And we’ll be buying one of them for our portfolio.

They picked Keppel DC REIT (SGX: AJBU), Frasers Logistics & Commercial Trust (SGX: BUOU), and DBS (SGX: D05).

Now, it might sound crazy to stake our money on the public’s opinion.

But we’re not leaving this decision to chance.

To make the most optimal decision, we’re going to deep dive into each stock’s strengths, weaknesses, and long-term income potential.

And you’ll be among the first to see this analysis when you join our webinar on 29 July.

With our money on the line on 3 “random” stocks, this could be one of the most intense presentations we’re having.

If you want to gauge the potential of these 3 stocks for yourself, this webinar is perfect for you.

Click here to register a seat for free now!

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclaimer: Royston Yang does not own shares in any of the companies mentioned.