CapitaLand Investment Limited (SGX: 9CI), or CLI, has just submitted its very first earnings report.

CLI was spun out of the CapitaLand Group last year in an exercise that saw the real estate giant’s development arm being privatised.

The group is taking on a more asset-light stance compared to its predecessor.

We previously compared the now delisted CapitaLand Group with its peer Frasers Property Limited (SGX: TQ5) almost a year ago.

Investors may now be curious as to how CLI compares with another property behemoth — City Developments Limited (SGX: C09), or CDL.

We decided to pit the two real estate conglomerates against each other to determine which makes the better investment choice.

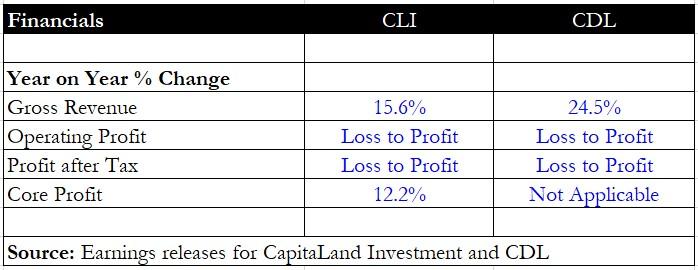

Financials

We start by looking at both companies’ latest fiscal 2021 (FY2021) income statements.

CLI reported a 15.6% year on year rise in revenue to S$2.3 billion while CDL saw a 24.5% year on year jump in revenue to S$2.6 billion.

Because of lower impairment losses, both companies saw their operating and net losses turn to profits in FY2021.

CLI, however, had indicated that its core net profit increased by 12.2% year on year to S$497 million after excluding one-off gains and losses, revaluation adjustments, and impairments.

As CDL did not disclose its core net profit, no meaningful comparison can be made for this metric.

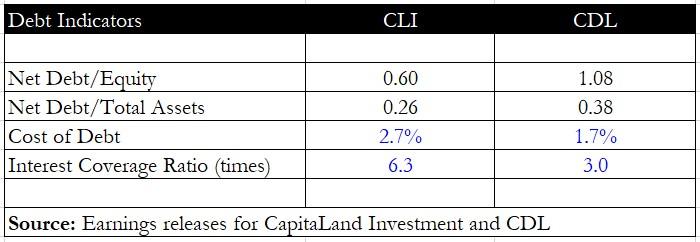

Debt indicators

Next, we move on to the debt indicators.

CLI has a lower net debt to equity as well as a lower net debt to total assets compared with CDL.

For context, a lower ratio implies that a company’s debt load is less burdensome and is also less likely to result in financial troubles.

However, CDL enjoys a lower overall cost of debt than CLI, at 1.7% versus 2.7%.

That said, CLI’s interest coverage ratio is more than double that of its peer, at 6.3 times.

The higher this ratio is, the better, as it assures that a company’s interest expense can be adequately serviced by its operating profit.

Winner: CLI

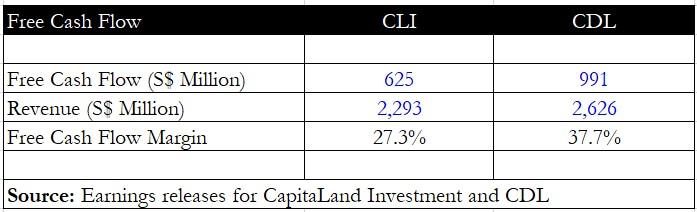

Free cash flow

Another important metric we looked at was free cash flow.

Both CLI and CDL generated positive free cash flow for FY2021.

We went a step further and compared the free cash flow margin for each business.

This financial metric looks at how much free cash flow is generated per dollar of revenue.

CDL, in this case, registered a higher free cash flow margin of 37.7% compared to CLI’s 27.3%.

Winner: CDL

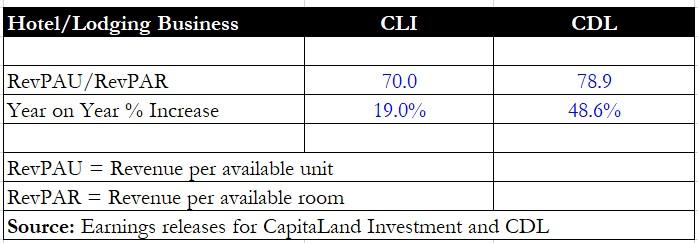

Hotel and lodging division

We were also curious about how each company’s hotel cum lodging division fared in the light of the pandemic.

FY2021 saw an improvement in overall economic conditions as some countries reopened and restrictions were eased.

Travel was also restarted with the introduction of vaccinated travel lanes in the second half of last year.

The one metric that was disclosed by both companies was the revenue per available room or RevPAR.

CDL’s RevPAR, at close to S$79, was higher than CLI’s. The year on year increase, at 48.6% for CDL, was also much sharper, indicating a strong rebound.

Winner: CDL

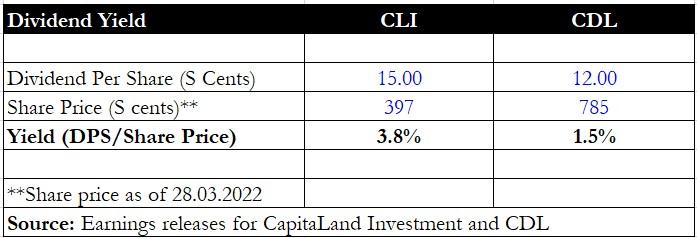

Dividend yield

Finally, we observed each company’s dividend yield based on the total dividend declared for FY2021.

CLI has proposed a final dividend of S$0.12 and a special dividend of S$0.03 for FY2021, bringing the total dividend to S$0.15.

Its shares offer a trailing dividend yield of 3.8%.

Even if we exclude the S$0.03 special dividend, CLI’s shares will still offer a fairly decent historical yield of 3%.

Contrast this to CDL, which has declared a total dividend of S$0.12 for FY2021.

Its trailing dividend yield is just 1.5%.

However, CDL had also declared a dividend-in-specie of units in CDL Hospitality Trust (SGX: J85), or CDLHT, when it announced its FY2021 results.

Eligible shareholders of CDL will receive 0.159 CDLHT units for every CDL share they own.

When the value of this share dividend is accounted for, then the total FY2021 dividend comes up to S$0.311, giving CDL’s shares a yield of nearly 4%.

Winner: CLI

Get Smart: Each has its own merits

It’s been a tough contest for both CLI and CDL, with each snagging two categories.

The conclusion is that each property giant has its investment merits, and investors need to know what they are looking for when choosing either one to invest in.

CLI is rapidly building up both its lodging segment and its funds under management, while CDL has a diversified portfolio that stretches across multiple regions.

Ultimately, the decision depends on how comfortable you are with each company’s growth profile and prospects.

Is now a good time to buy into Singapore REITs? After all, almost 50% of the 44 Singapore REITs were trading close to their 52-week lows in January.

But with the right strategy, mindset and stocks, REITs can still be a powerful source of dividends today and in the years ahead.

Did you know there are 5 REIT sectors with a high potential for creating passive income? If you are building retirement wealth, this is crucial information. We have a new report that details all you need to know about them. Find out which sector to pay attention to, and see if you can fit them into your portfolio. Click HERE to download the guide for free.

Don’t forget to follow us on Facebook and Telegram for the latest investing news and analyses!

Disclaimer: Royston Yang does not own shares in any of the companies mentioned.