As an investor that has a more than 70% concentration of my portfolio in technology stocks, this year hasn’t been all roses and sunshine for me.

Just a few weeks ago, the S&P 500 Index entered a bear market after closing more than 22% below its all time high of 4,818.62 on 4 January 2022.

From the Russia-Ukraine war and COVID-related lockdowns in China that disrupted supply chains to the biggest interest rate hike since 1994, the blows just keep landing.

The worst mistake any investor can make is to sell their shares in panic when nothing is fundamentally wrong with the business.

We will now take a closer look at five technology companies within my portfolio.

Zoom Video (NASDAQ: ZM)

Zoom Video Communications, or Zoom, is a secure and reliable video communications platform that became a verb during the peak of the pandemic due to its popularity.

Its share price has fallen a long way since the all time high of US$588.84 on 19 October 2020.

As of 12th July, Zoom’s share price has fallen 41% year to date.

In its fiscal first quarter 2023 (1Q2023), revenue rose by 12% year on year to US$1.1 billion.

Zoom has seen momentum in Enterprise customers’ growth, with Enterprise revenue rising by 31% year on year to US$560 million during the quarter.

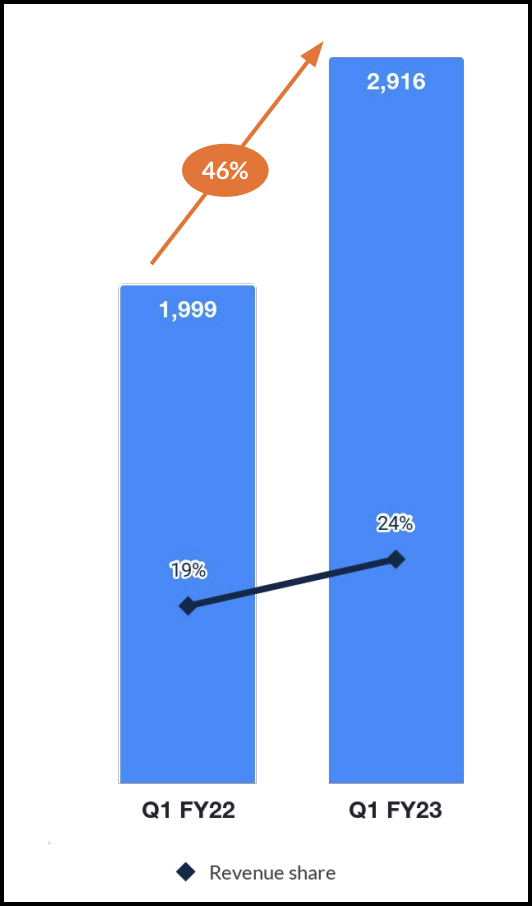

A closely-watched metric is Enterprise customers as it indicates the company’s efforts on growing the customer segment that contributes the bulk of its revenue.

The total number of Enterprise customers that contributed more than US$100,000 in annual billings grew 46% year on year to 2,916.

Source: Zoom, 1Q2023 earnings deck, >US$100k customers breakdown

For the coming quarters, a key aspect to watch will be how Zoom sells through other product offerings such as Zoom Contact Centre, Zoom Phone, Zoom Whiteboard, and Zoom IQ for sales teams.

Tesla (NASDAQ: TSLA)

Tesla is one of the world’s largest all-electric vehicle companies through the sale of cars, pickup trucks in the United States, China, and other countries around the world.

Differing from most of the other automotive manufacturers that sell through franchised dealerships, Tesla sells its cars direct to consumers.

This prevents any potential conflicts of interests which may arise as Tesla owns the showrooms and customers deal only with its staff.

Tesla also sells directly through the internet to consumers where a Tesla can be customised online.

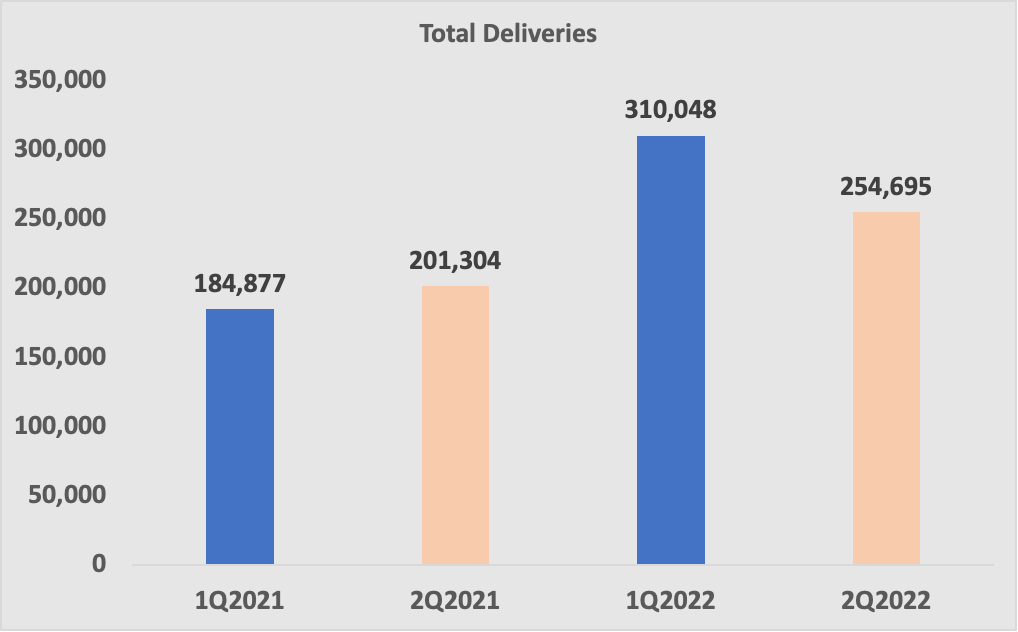

In 1Q2022, Tesla reported an 81% year on year growth in total revenue to US$18.7 billion, and net income rose more than seven-fold to US$3.3 billion.

This growth was largely attributable to increased vehicle deliveries, which grew 68% year on year to 310,048 in 1Q2022.

Tesla also cited increased average selling price as one of the factors contributing to the increased revenue seen, which suggests to me they have strong pricing power.

On 2 July, Tesla released its 2Q2022’s vehicle production and delivery numbers of (Production: 258,580, Deliveries: 254,695), which caused a temporary sell off as investors started to compare it with the production and delivery numbers seen in 1Q2022.

Source: Tesla, 1Q2022 update, 2Q2022 production and delivery update

Although it seems that there is a 17.9% decline in vehicle delivery numbers between 1Q2022 and 2Q2022, investors should note that the delivery numbers are still 26.5% higher than that of 2Q2021.

With its commitment to achieve 50% average annual growth in vehicle deliveries, and seeing what increased delivery numbers mean for its revenue and net income, I remain a patient investor in Tesla.

Tesla’s full set of 2Q2022 numbers will be announced on 20th July, after the US market closes.

Netflix (NASDAQ: NFLX)

Netflix is one of the world’s largest streaming media and entertainment services companies, with 222 million paid memberships in over 190 countries.

Netflix surged to dominance similarly during the COVID-19 period when most countries were on lockdown.

Over the years, it has consistently produced great content that hooked viewers, with popular TV series Stranger Things, Squid Game and Money Heist etc.

With the current bear market and tech sell off that we witnessed not too long ago, the stock has also fallen 70.8% year to date (12 July 2022’s closing price).

Netflix’s 1Q2022 revenue rose 9.8% year on year to US$7.9 billion, while net income for the same period declined 6.8% year on year to US$1.6 billion.

In its 1Q2022 earnings call, Netflix reported a loss of 200,000 subscribers compared with its previous quarter and mentioned that it is guiding for a two million loss in subscribers for its second quarter.

Although the market didn’t react well to this news, there is justification for this guidance and the plans that Netflix has laid out seemed fair.

Netflix is looking to introduce more controls to prevent password sharing outside the household.

More than 100 million households are piggy backing on other paid subscribers

These free loaders are active users as well, so it is reasonable for Netflix to levy an introductory charge on this base of customers.

Such a move, if successful, could open up an additional revenue stream for the streaming giant.

To combat the fierce competition from the likes of Walt Disney (NYSE: DIS) and Amazon (NASDAQ: AMZN), Netflix is looking to offer lower-cost plans with advertising.

This is a win-win model that would not only attract and retain budget-constrained subscribers, but also introduce new revenue streams for the company.

DocuSign (NASDAQ: DOCU)

DocuSign is an e-signature platform provider that enables organisations to automate, sign, and manage agreements electronically across practically any smart device.

It is the world’s number one e-signature solution with a strong base of 1.24 million customers.

For its 1Q2023 ended 30 April 2022, DocuSign reported revenue growth of 25% year on year to US$589 million.

Gross margin was 81%, with operating margin 17% for 1Q2023.

Alongside these strong margins, DocuSign also commands a high net dollar retention rate of 114%.

DocuSign spooked the market when it announced weak guidance for 2Q2023’s billings, between the range of US$599 million to US$609 million.

The market felt that this forecasted increase, even at the top end of its range, was only 2.3% higher than 2Q2022’s US$595.4 million.

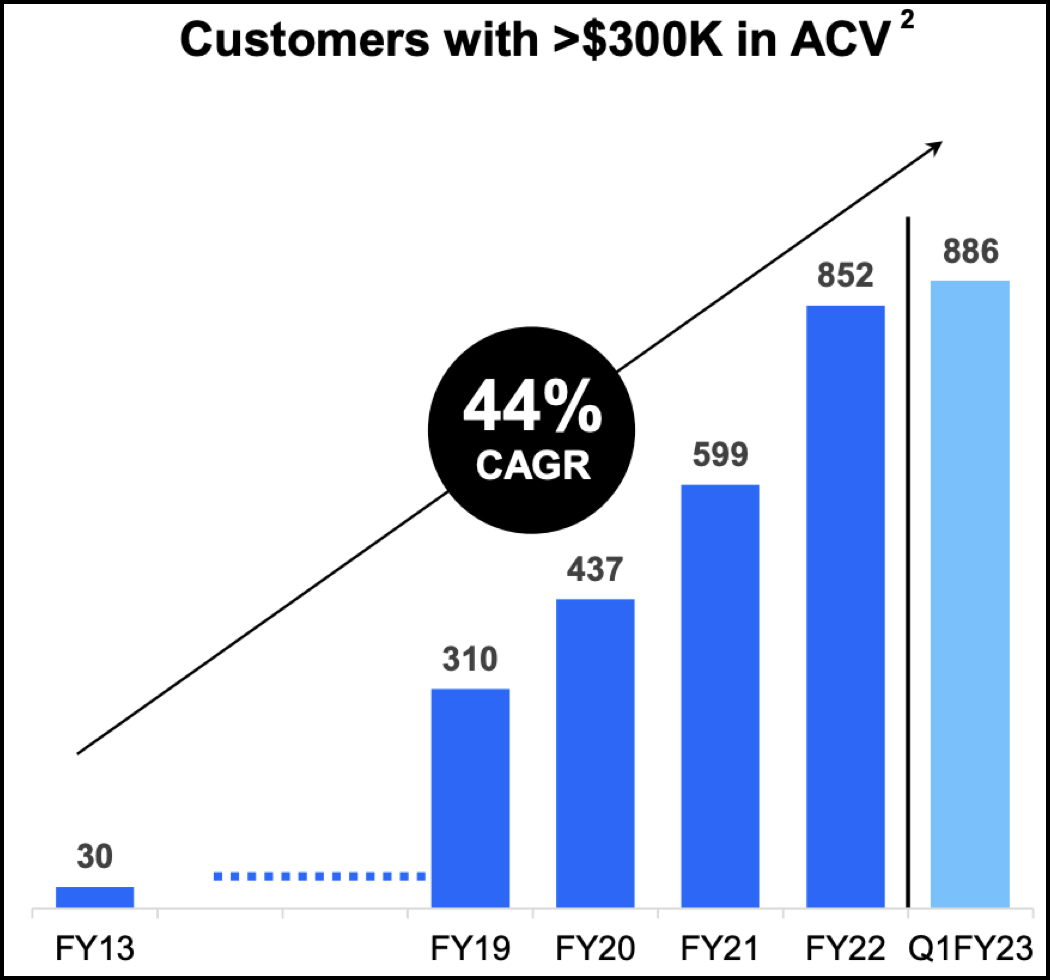

That said, looking at the explosive growth in its total customer base, which has a compound annual growth rate (CAGR) of 40% from FY2013 to 1Q2023, monetisation opportunities are still plenty for DocuSign.

In addition, its strength in gaining enterprise customers that spend more than US$300,000 a year, also saw a CAGR of 44% from FY2013 to 886 in 1Q2023.

Source: DocuSign, 1Q2023 earnings release, customer base breakdown

Last but not least, the strategic partnership that DocuSign announced with Microsoft (NASDAQ: MFST), which will see integration of cross products, means there will be extra momentum that will come from the Enterprise segment.

Apple (NASDAQ: APPL)

Apple is a company that needs no further introduction. It changed the entire era of smartphones and is now one of the most valuable brands in the world.

It is also the largest contributor to the S&P 500 index.

Apple has a strong base of loyal customers and has, over years, created a strong and interlinked ecosystem of products and services on the back of the success of the iPhone.

In its 2Q2022 earnings, we saw how Apple outperformed analysts’ expectations by reporting revenue of US$97.3 billion, above the US$94 billion that was forecasted.

As the COVID-related supply chain woes in China ease, Apple will benefit from the effect in the next few quarters.

As an investor, Apple’s main draw is the ability to innovate and cross sell its other services and products together directly to a strong and loyal customer base.

Although word on the street is pointing at Apple’s possible release of a virtual reality headset, what is certain is that when Apple launches it, this will likely be tied in with services revenue.

Services Revenue was Apple’s fastest growing segment as of 2Q2022 (+17% year on year), with revenue of US$19.8 billion.

Final Thoughts

Although most of the stocks above did fall from a high, a closer look at each stock provides assurance that the business behind each company is doing fine.

It is hard not to feel affected when the same stocks were registering more than 100% gains, but as a long term investor, I’m in for the long term, and I’ll likely strategically add on to these positions whenever there’s a chance.

How do you decide if a growth stock is worth your money? There is no shortage of stock ideas today, but is a particular stock suitable for you? Find out more in our latest FREE report, How To Find The Best US Growth Stocks For Your Portfolio. Click HERE to download the report for free now!

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclaimer: Kent Lee owns shares of Netflix, Apple, Tesla, Zoom Video and DocuSign.