It’s always a useful exercise to compare two REITs to see which makes a better investment choice for yourself.

Last week, we put Mapletree Industrial Trust (SGX: ME8U) and Mapletree Logistics Trust (SGX: M44U) side by side to compare which was a better buy.

This round, we decided to look at two popular REITs with CapitaLand Investment Limited (SGX: 9CI) as their sponsor.

The REITs are CapitaLand Integrated Commercial Trust (SGX: C38U), or CICT; and CapitaLand Ascendas REIT (SGX: A17U), or CLAR.

CICT is a retail cum commercial REIT while CLAR is Singapore’s oldest industrial REIT.

Read on to find out which REIT is the most attractive choice for income investors.

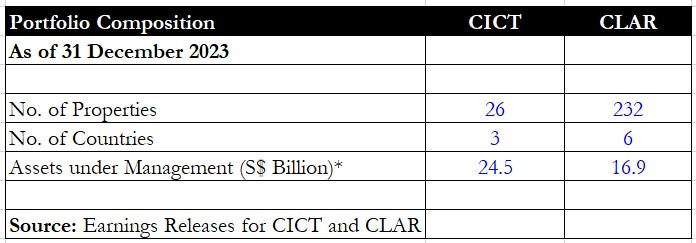

Portfolio composition

First, let’s look at each REIT’s portfolio composition.

CICT has 26 properties within its portfolio covering three countries – Singapore, Australia, and Germany.

CLAR, on the other hand, has nearly nine times more properties at 232 that span seven countries – Singapore, the US, Australia, the UK, France, the Netherlands, and Switzerland.

Although CICT’s assets under management are nearly 50% higher than CLAR, its portfolio loses out in terms of property and regional diversification.

Winner: CLAR

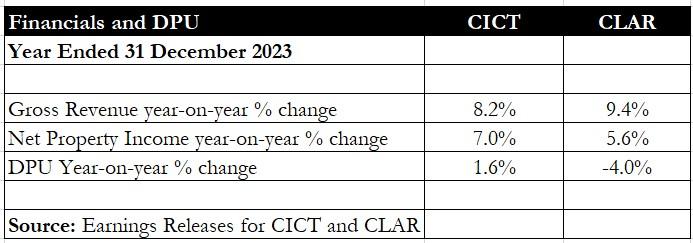

Financials and DPU

Moving on to the financials for each REIT, both CICT and CLAR enjoyed a year-on-year increase in gross revenue for 2023.

CICT saw higher contributions from Raffles City Singapore along with full-year contributions from acquisitions made in 2022.

CLAR’s revenue benefitted from acquisitions made in both 2022 and 2023 as well as higher occupancy and positive rental reversions.

Both REITs, however, suffered from higher interest expenses arising from the high interest rate environment.

Distributable income fell year on year for CLAR but CICT managed to eke out a small year on year rise.

As for distribution per unit (DPU), CICT saw a small 1.6% year-on-year gain to S$0.1075 but CLAR’s DPU fell by 4% year on year to S$0.1516 also due to an enlarged base of units (+2.7% year on year).

Winner: CICT

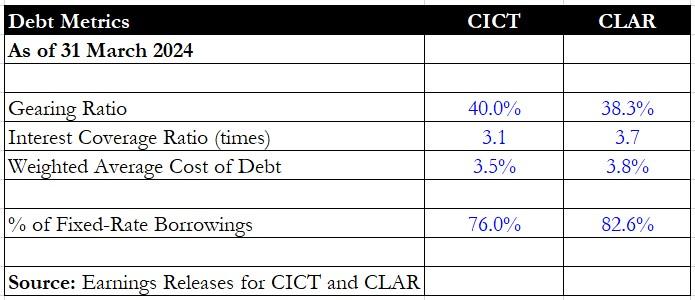

Debt metrics

Next up, we review the debt metrics for each REIT.

CICT has a slightly higher aggregate leverage at 40% compared with CLAR’s 38.3%.

The retail and commercial REIT’s interest cover ratio is also lower at 3.1 versus CLAR’s 3.7 while its proportion of fixed rate borrowings is lower at 76% versus CLAR’s 82.6%.

The only aspect where CICT has the upper hand is its weighted average cost of debt which was 0.3 percentage points lower than CLAR’s.

Taken in totality, CLAR still wins in this area as it is more buffered against future interest rate increases and has an overall lower gearing.

Winner: CLAR

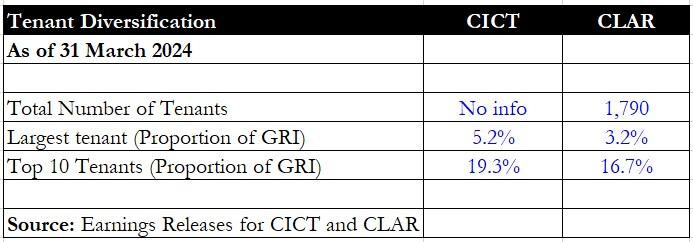

Tenant diversification

The next area we look at is how diversified each REIT’s tenant base is.

A more diversified tenant base will ensure that the REIT is buffered against sharp rental income drops during tough economic times.

CICT did not provide any information on its total number of tenants but CLAR stated that it has 1,790 tenants across all its properties.

The largest tenant took up just 3.2% of gross rental income (GRI) for CLAR versus 5.2% for CICT.

Also, CLAR’s top 10 tenants made up just 16.7% of GRI, lower than CICT’s 19.3%.

Winner: CLAR

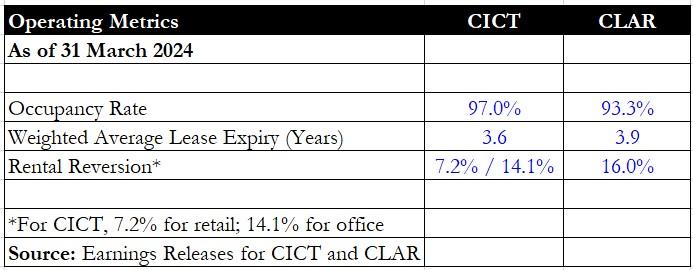

Operating metrics

When it came to operating metrics, it was a mixed bag across both REITs.

CICT’s latest committed occupancy rate stood high at 97% while CLAR’s was a respectable 93.3%.

For rental reversion, CICT saw positive reversions across both its retail (+7.2%) and commercial (+14.1%) divisions.

However, it was not enough to beat CLAR’s impressive 16% positive rental reversion.

CLAR also had a slightly longer weighted average lease expiry because of its industrial tenant leases.

However, occupancy takes precedence in this case as it determines the strength of demand for the REIT’s properties.

For this aspect, CICT has the upper hand as it reported positive rental reversions along with an occupancy rate above 95%.

Winner: CICT

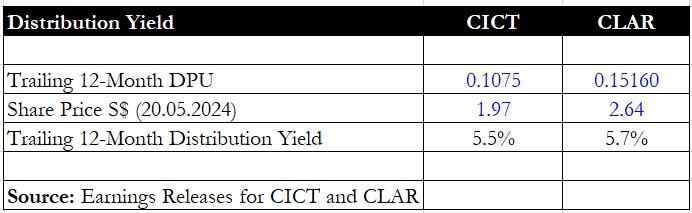

Distribution yield

Finally, we come to arguably the most important aspect of a REIT – its distribution yield.

CLAR has a slightly higher distribution yield of 5.7% versus 5.5% for CICT.

Winner: CLAR

Get Smart: Capital recycling efforts

After listing out the winners for each category, it still was not easy to conclude.

Both CICT and CLAR exhibited strong attributes and are well-managed REITs.

CICT is the winner this round because it demonstrated its ability to raise its DPU and boasts a high occupancy rate along with healthy positive rental reversions.

Investors should also turn their attention to each REIT’s capital recycling efforts as another attribute to consider when deciding which REIT to buy.

CICT’s asset enhancement initiative (AEI) at CQ @ Clarke Quay has been completed and the REIT is not embarking on two new AEIs for the IMM Building in Singapore and Gallileo building in Frankfurt.

CLAR conducted three divestments in the first quarter of 2024 and has a list of five AEIs for properties in Singapore.

Want more dividends in 2024? Our latest FREE report spotlights five Singapore REITs with distribution yields of 5.5% or more, a rare find in today’s market. These are reliable, proven performers. Just one stock inside could boost your portfolio’s returns in the next few months. Download your report today and start reaping the benefits.

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclosure: Royston Yang owns shares of Mapletree Industrial Trust.