Higher interest rates have been a bane for the REIT sector and businesses with heavy debt loads.

However, the three local banks have benefitted greatly from the surge in interest rates that has lifted their net interest margins (NIMs) and net interest income (NII).

The trio have all reported record profits during the latest earnings season.

United Overseas Bank (SGX: U11), or UOB, started the season with a 35% year-on-year rise in net profit for 2023’s second quarter (2Q 2023) excluding the integration costs from its acquisition of Citigroup’s (NYSE: C) consumer banking franchise.

DBS Group (SGX: D05) came along and reported a net profit of S$2.6 billion for 2Q 2023, up 45% year on year.

And finally, OCBC Ltd (SGX: O39) was the last to announce its results and impressed with a 34% year-on-year increase in net profit to S$1.7 billion for the quarter.

With all three banks announcing stellar results, which should investors pick for their portfolio?

We compare all three blue-chip banks on various metrics to try and figure this out.

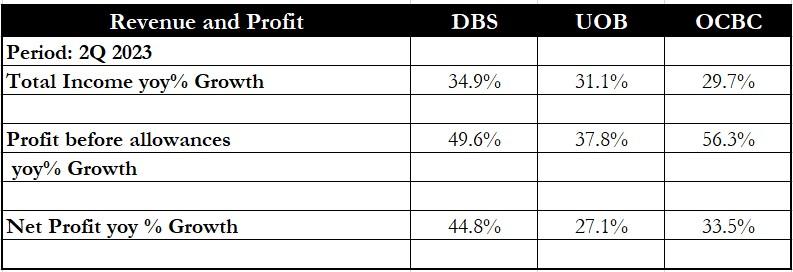

Financials

Starting with the financials for each lender, all three banks saw total income shoot up sharply because of higher NII brought about by higher interest rates.

Consequently, profit before allowances also rose sharply as expenses rose less than total income.

However, DBS is the leader here as it logged the strongest year-on-year rise in total income.

Singapore’s largest bank also clocked up the best year-on-year increase in net profit of 44.8%.

Winner: DBS

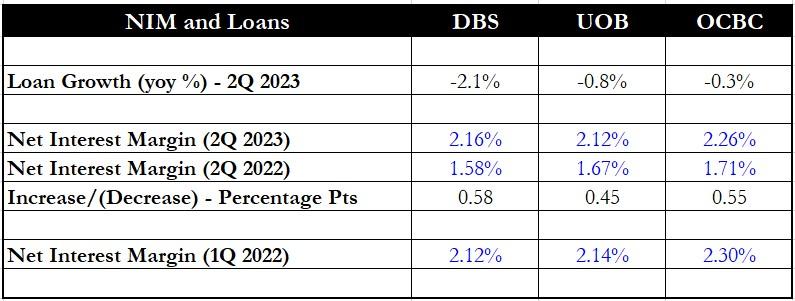

Net interest margin and loan growth

Next, we look at the banks’ NIMs and the growth of their loan books.

All three banks saw their loan books shrink year on year as high interest rates begin to bite, causing individuals and businesses to become hesitant to take on more debt.

DBS saw the worst fall of the three at 2.1% while OCBC experienced the gentlest decline at just 0.3%.

For NIM, OCBC is the clear winner with the highest NIM of the three at 2.26%.

However, DBS managed to chalk up the highest increase in its NIM on a year-on-year basis at 0.58 percentage points.

It was also the only bank to report a quarter-on-quarter increase in NIM, going from 2.12% to 2.16%.

DBS’ CEO Piyush Gupta also believes there could be more upside to NIMs as 20% of DBS’ commercial book has yet to reprice while the US central bank seems intent on further raising interest rates to combat inflation.

Despite these trends, OCBC still emerges as the winner with the lowest loan book decline while sporting the highest NIM.

Winner: OCBC

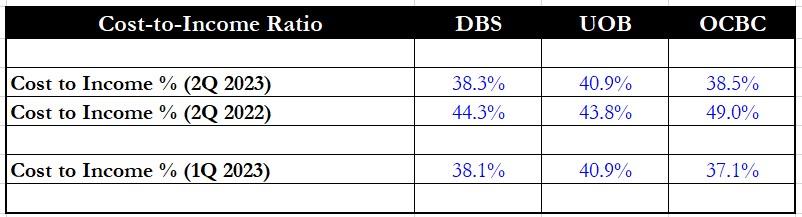

Cost-to-income ratio

The cost-to-income ratio (CIR) measures the efficiency of a bank’s operations by comparing its operating expenses with its total income.

A lower CIR is preferred as it means the bank is running more efficiently compared to its peers.

In this regard, DBS has the lowest CIR of the three at 38.3% but OCBC has come close with a CIR of 38.5%.

That said, DBS saw its CIR increase by just 0.02 percentage points from 1Q 2023 while OCBC’s CIR jumped 0.14 percentage points.

Winner: DBS

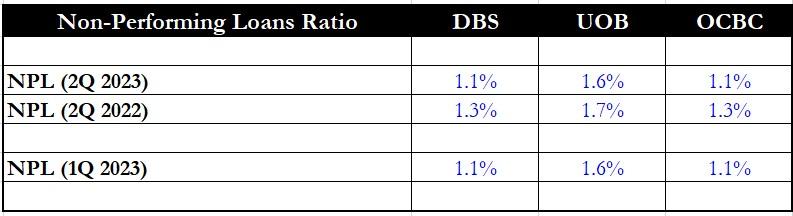

Non-performing loans ratio

Now we come to the non-performing loans ratio, or NPL ratio, which measures the proportion of a bank’s loans that may go sour.

A lower NPL ratio implies that the bank expects less of its loans to go bad and that its borrowers are doing fine.

Both DBS and OCBC are tied with an NPL ratio of 1.1%.

Winner: DBS and OCBC (tie)

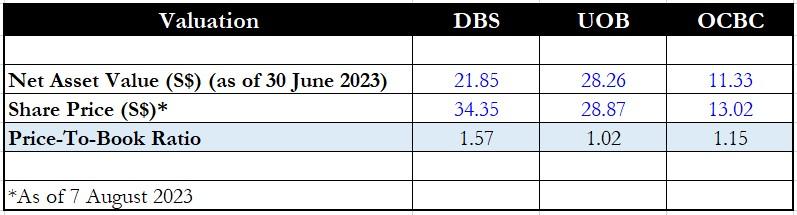

Valuation

When it comes to valuation, DBS has the highest price-to-book (PB) ratio by far at 1.57 times.

UOB, on the other hand, is trading just above its book value of S$28.26.

OCBC remains relatively cheap as well with a PB ratio of 1.15 times.

Winner: UOB

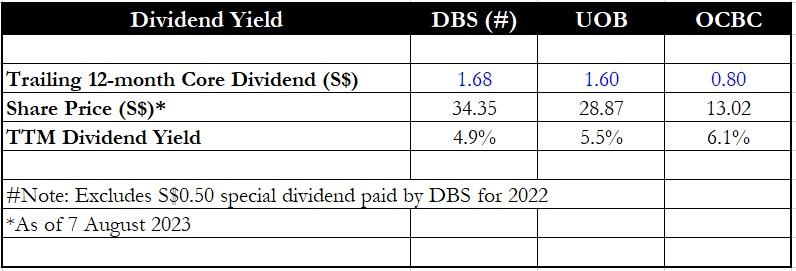

Dividend yield

For dividend yield, we took the trailing 12-month dividend paid out by each lender but excluded any special, one-off dividends.

Using each bank’s core dividend, OCBC had the highest dividend yield at 6.1% with DBS registering the lowest at 4.9%.

However, DBS had just upped its quarterly dividend from S$0.42 in 1Q 2023 to S$0.48 in the current quarter.

Hence, it has an annualised dividend of S$1.92 per share and its forward dividend yield stands at 5.6%.

Investors should note that with the strong results momentum, all three banks could raise their final dividends when they release their earnings in February 2024.

Winner: OCBC

Get Smart: Considering other factors

DBS and OCBC are tied with three winning factors each but investors need to consider other aspects to decide which bank to buy.

For instance, UOB expects to achieve an annualised revenue uplift of S$1 billion from its Citigroup acquisition and integration for 2023.

OCBC introduced a refreshed logo and has identified strategic initiatives to garner S$3 billion in incremental revenue from 2023 to 2025.

Want to protect your child’s money from inflation? Transform your child’s ‘piggy bank’ into a ‘golden goose’ that keeps giving even until they have grandchildren. Our latest FREE report shows you a stress-free method and 3 superstar stocks that could protect your child’s money from inflation. Click HERE to get a copy of our latest guide.

Disclosure: Royston Yang owns shares of DBS Group.