“The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks.”

— Jerome H. Powell, 2024 Speech at “Reassessing the Effectiveness and Transmission of Monetary Policy

The US Federal Reserve Chairman’s speech two weeks ago sent a strong signal that the US central bank will likely cut interest rates in the near future.

As income investors, we are naturally concerned about the potential impact of rate cuts on our recurring dividends.

Banks have benefited from rising interest rates in recent years, but the question remains as to whether they can sustain their dividends in a lower interest rate environment.

Or perhaps it’s time to put some money in the beleaguered REITs sector as REITs are likely to benefit from lower interest rates going forward?

Singapore banks are likely to remain resilient in the near future

Whether Singapore’s three major banks DBS Group (SGX: D05), OCBC Ltd (SGX: O39), and United Overseas Bank Ltd (SGX: U11) can sustain their dividends largely depends on whether they can maintain or grow their income.

Broadly speaking, banks have two main sources of income: net interest income (NII) and non-interest income (Non-II).

If rate cuts do indeed occur in the coming months, it is likely that banks’ net interest margin (NIM) will fall from their current levels.

NII could decline as a result.

But what does that mean?

Let me use an analogy.

Imagine this: there’s a container A filled with 50-cent coins and a larger container B filled with 20-cent coins.

Which container would have a higher amount of money?

You got it.

The answer depends on how much larger container B is.

Similarly, whether NII will drop with a declining NIM depends on how much more the bank can grow its loans.

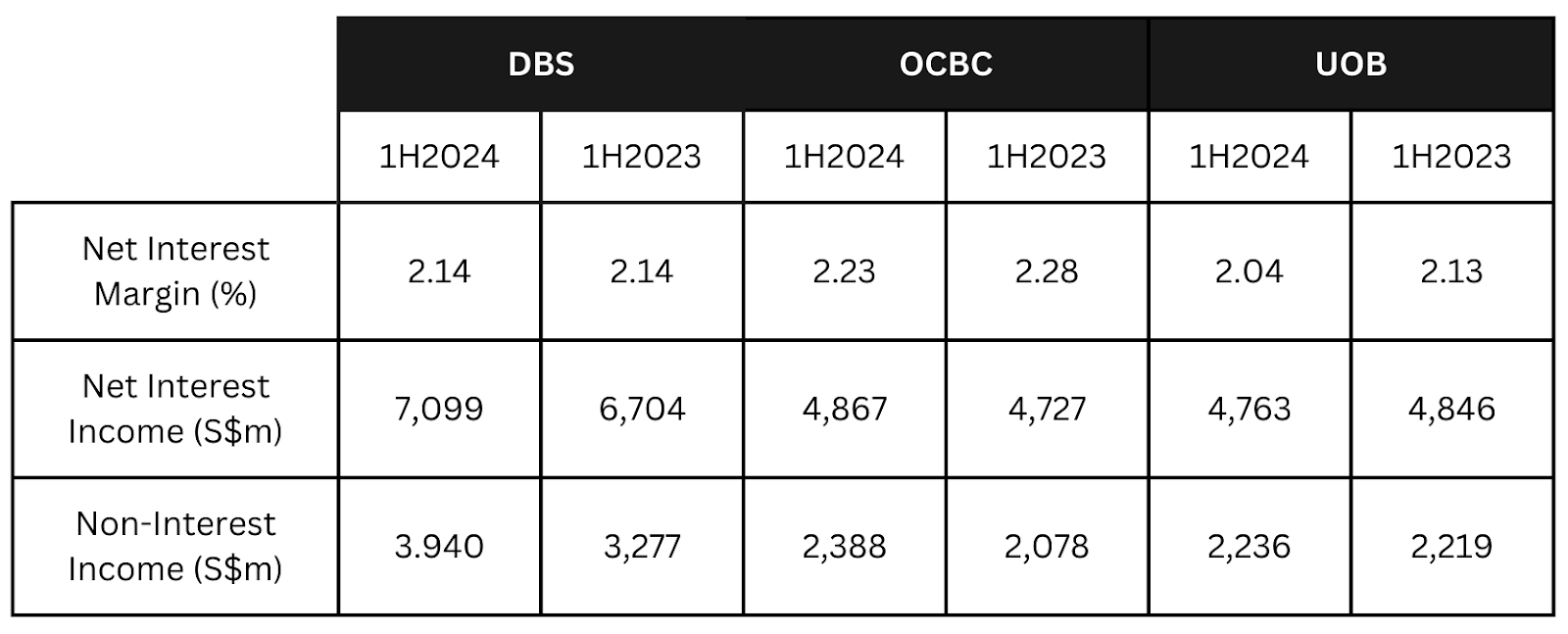

The table below which summarises the latest results from the three banks clearly shows that there is no definitive relationship between NIM and NII.

Source: DBS, OCBC, UOB 1H2024 results, compiled by the author

For 1H2024, UOB’s NII declined in tandem with its NIM but DBS was able to increase its NII with no change in its NIM.

Similarly, despite the drop in OCBC’s NIM, the bank was able to increase its NII.

Back to the analogy.

What if container B is now filled with 10-cent coins instead? Which container would have a higher amount of money now?

While it still depends on how much larger container B is, we can agree that it now needs to be very much bigger than container A to hold a higher amount of money.

Hence, if the decline in NIM is too steep, the loan growth may not be enough to mitigate the impact.

Beyond NII, the three banks have expanded their Non-II.

For 1H2024, DBS and OCBC grew their Non-II year-on-year by double digits.

Meanwhile, UOB’s Non-II growth was muted for the period above, but the CEO has guided a double-digit fee growth for the full year.

What does the above tell you?

While the future interest rate environment remains uncertain, Singapore banks have demonstrated a strong track record of dividend sustainability.

Except for 2020, when the Monetary Authority of Singapore called on the banks to cap their dividends, the trio have maintained or increased their dividends over the past decade.

Therefore, barring any unforeseen circumstances, the three Singapore banks are likely to continue to pay out steady, if not growing, dividends.

What about Singapore REITs? Will they benefit from the lower rate?

Rising interest rates may be a headwind for banks, but the REITs sector is poised to gain from lower interest rates.

If interest rates come down, REITs will benefit from lower borrowing costs, which can improve their profitability and ability to acquire accretive assets.

However, unlike Singapore banks, the REIT sector is more diverse.

Hence, the impact will vary depending on individual REITs’ debt structures, property types, and geographic exposure.

For instance, REITs with a higher proportion of floating-rate debt will likely experience a more significant and immediate positive impact from a rate cut.

For some REITs, the lower interest rates may still exceed the prevailing rates of their existing debt that require refinancing.

Hence, their average borrowing costs may continue to increase in the near term.

Furthermore, if the demand for properties within specific sectors and geographic regions is weak, the positive effects of lower rates may come to nought.

Above all, REITs with strong fundamentals, such as those that have weathered the recent downturns or possess strong sponsors, are better positioned to capitalise on lower interest rates and achieve stronger financial performance over the long term.

Get Smart: Invest in well-managed businesses

While interest rates can certainly influence the performance of banks and REITs, it is essential to remember that interest rates are just one factor among many.

Instead of fretting over interest rate movements, focus on investing in businesses with strong financial health, competitive advantages, and experienced leadership.

The goal is to invest in companies that are capable of generating sustainable returns over time, and not just react to short-term interest rate movements.

Dive into the future of technology with our newest FREE report, “The Rise of Titans.” Discover how the big 7 US tech stocks can be your ticket to huge long-term gains. Download your copy today and see how easy it is to supercharge your portfolio.

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclosure: Chan Kin Chuah owns shares of DBS, OCBC and UOB.