Once a favourite asset class among investors, real estate investment trusts (REITs) have fallen out of favour due to aggressive central banks’ interest rate hikes from 2022 to 2023.

These hikes have increased REITs’ borrowing costs, putting additional pressure on them alongside higher operating expenses caused by inflation.

Despite these challenges, Frasers Centrepoint Trust (SGX: J69U), Mapletree Pan Asia Commercial Trust (SGX: N2IU), and ParkwayLife REIT (SGX: C2PU) have all shown commendable performance.

Amid this negative sentiment, these well-managed REITs could be a compelling opportunity for investors seeking long-term income.

Frasers Centrepoint Trust (FCT): A Resilient Singapore Retail REIT

FCT is a leading owner of suburban retail malls in Singapore.

These malls are conveniently located near homes and within easy reach of public transportation, resulting in strong demand for their shop spaces.

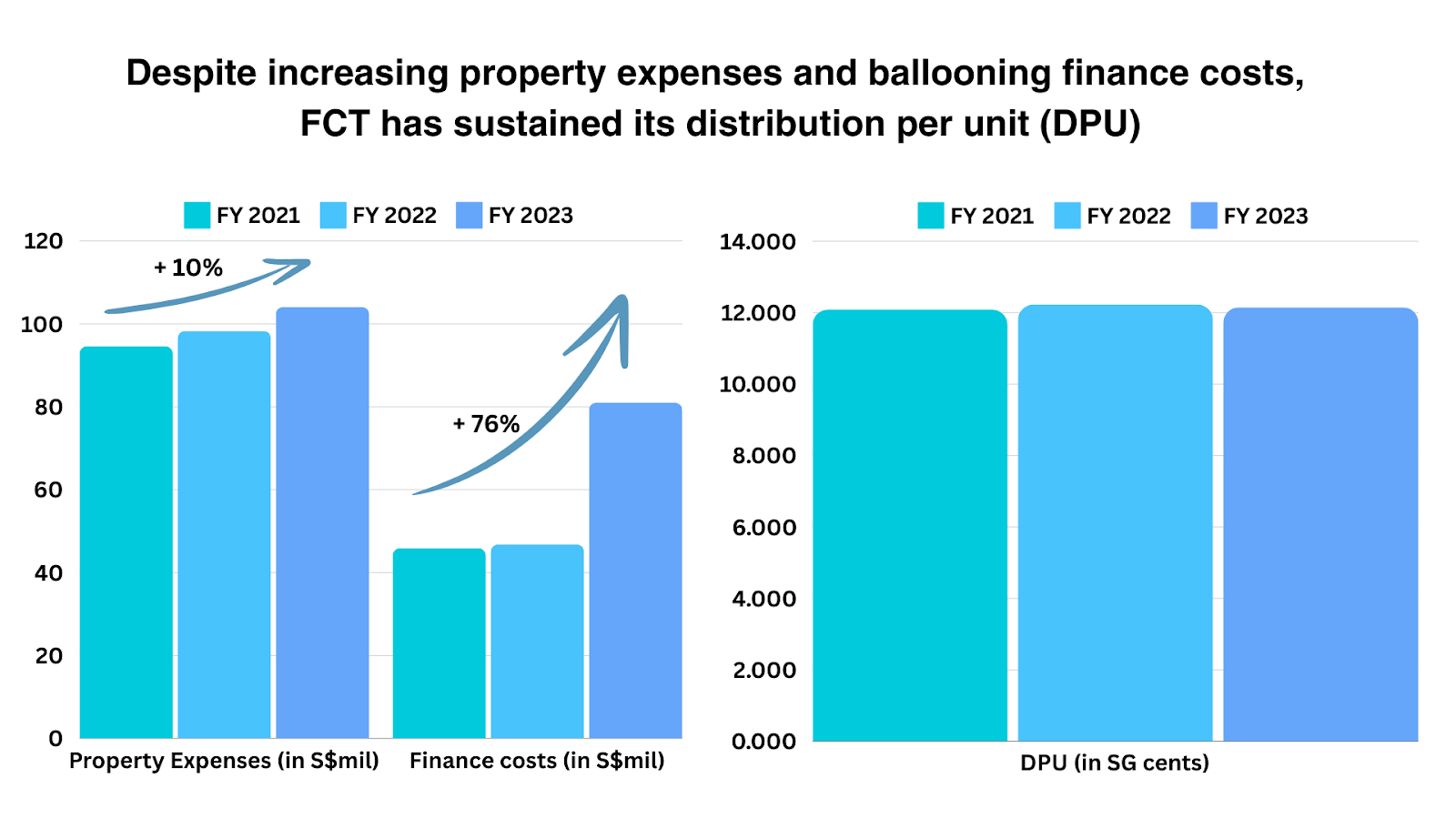

Source: FCT Annual Reports

As the data reveals, property expenses jumped by 10% from 2021 to 2023, and finance costs ballooned 76% over this period.

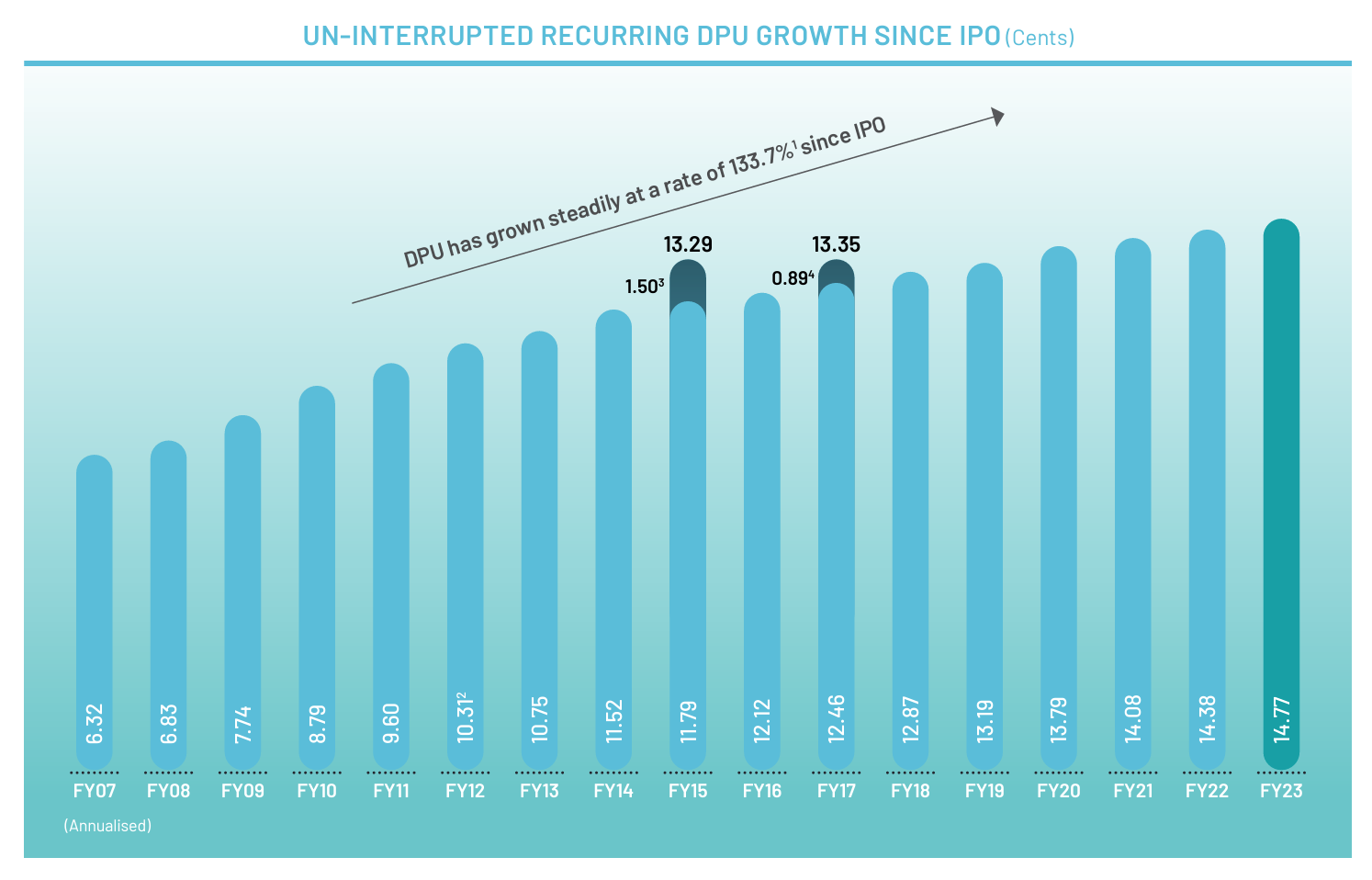

However, this increase was mitigated by its robust business operation, resulting in a minimal change in its distribution per unit (DPU).

In its latest 1H2024 earnings report, FCT boasted a high committed occupancy of 99.9% and average positive rental reversion of 7.5%. Meanwhile, shopper traffic and tenant sales also grew year-on-year (YOY) for the quarter.

With finance costs unlikely to skyrocket further, coupled with healthy demand for shop spaces, FCT has a good chance of maintaining its DPU.

Mapletree Pan Asia Commercial Trust (MPACT): Navigating Challenges and Emerging Stronger

MPACT was formed out of the 2022 merger of Mapletree Commercial Trust and Mapletree North Asia Commercial Trust.

The combination of these two REITs coincided with a period of aggressive interest rate hikes.

As a result, the newly formed REIT’s aggregate leverage ratio rose from 33.8% on 30 June 2022 to above 40% as of 30 September 2022.

Coupled with the higher cost of debt, finance costs for the fiscal year 2023/24 (FY 2023/24) surged by 39% YOY.

Furthermore, a stronger Singapore dollar against foreign currencies during this period contributed to a 7.3% year-on-year drop in DPU.

Despite these headwinds, there are positive signs that point to a brighter future for MPACT.

- Strong Occupancy and Rental Reversion: As of 31 March 2024, the portfolio maintains a healthy occupancy rate of 96.1%. Supported by strong demand for Singapore properties, average rental reversion for the FY 2023/24 was positive at 2.9%.

- Improving Operation for Festive Walk: MPACT’s Festive Walk property has been struggling with negative rental reversion. However, the Hong Kong property is showing signs of rental stabilisation. Notably, its net property income (NPI) has increased by about 40% from the previous year.

- Potentially Reduced Finance Costs: The announced divestment of Mapletree Anson (scheduled for completion in July 2024) is projected to reduce its aggregate leverage to 37.6% on a pro forma basis.

Having navigated a challenging operating environment over the past two years, MPACT appears well-positioned to improve its performance moving forward.

ParkwayLife REIT (PLife REIT): A Leader in Healthcare with a Growing Track Record

Last year marked the 16th consecutive year that PLife REIT has increased its core DPU since its listing.

Image credit: PLife REIT’s 2023 annual report

This impressive feat was achieved through a strong relationship with its sponsor IHH Healthcare Berhad (SGX: Q0F) and a sound management strategy.

For its Singapore portfolio, namely Mount Elizabeth Hospital Property, Gleneagles Hospital Property and Parkway East Hospital Property, PLife REIT has renewed its master lease with IHH in 2022.

This agreement secures a guaranteed rental step-up from 2022 to 2025, followed by the annual rental review adjustment formula which will apply for the remaining lease term till 2042.

With the Singapore portfolio contributing about 70% of its total NPI, the arrangement provides a sustained rental income stream in the long run.

That said, PLife was not immune to the increase in borrowing cost and foreign exchange fluctuations.

While the cost of debt is still low at 1.3%, it has more than doubled since 2021.

Meanwhile, the Japanese yen (JPY) has also depreciated significantly against the Singapore dollar over the past two years.

This will have an impact on the rental earned from its Japanese properties.

PLife’s proactive capital management has cushioned the impact. The REIT has no immediate debt refinancing needs till March 2025, with around 91% of its interest rate exposure hedged.

In addition, JPY net income hedges are put in place till the first quarter of 2029. These hedges have allowed PLife to increase its 1Q 2024 DPU by 4.0%, despite the YOY drop in its gross revenue and NPI for the quarter.

With the favourable rental structure for its Singapore portfolio, its first-mover advantage in the Japanese aged care market, and its prudent capital management, PLife is poised to sustain its increasing DPU.

Get Smart: Eyes on the future

While bonds offer a safety net in today’s economic climate, investors can consider adding well-managed REITs as a strategic long-term investment, as REITs have the potential to outperform bonds over time.

By investing in these reliable REITs now, you are positioning yourself to benefit from a stream of growing passive income through their rising distribution per unit (DPU).

We have just revealed the top 7 US tech stocks poised for remarkable growth. In today’s fast-paced market, betting on these giants could mean more money in your pocket. With a focus on solid fundamentals and innovative prowess, these selections should earn a place in your portfolio. Click here to grab your FREE report now and start investing in the future, today.

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclosure: Chan Kin Chuah owns shares of Frasers Centrepoint Trust, Mapletree Pan Asia Commercial Trust and ParkwayLife REIT.