There are many reasons to like DBS Group (SGX: D05).

First off, it’s Singapore’s largest bank with a market capitalisation of close to S$84 billion, making it a blue-chip stalwart that investors can rely on through thick and thin.

Secondly, the bank has also navigated many crises successfully over the years and has come through them stronger than ever.

Most attractive of all is the lender’s ability to pay out steady, consistent dividends over the years.

The bank was paying out half-yearly dividends up till 2018 and switched to paying out quarterly dividends from 2019 onwards.

DBS’ most recent quarterly dividend came up to S$0.36 per share for an annualised dividend of S$1.44, giving its shares a forward dividend yield of 4.4%.

Looking ahead, can investors expect the bank to raise its dividends?

A track record of increasing dividends

To answer this question, we will take a look at both DBS’ dividend history as well as its prospects.

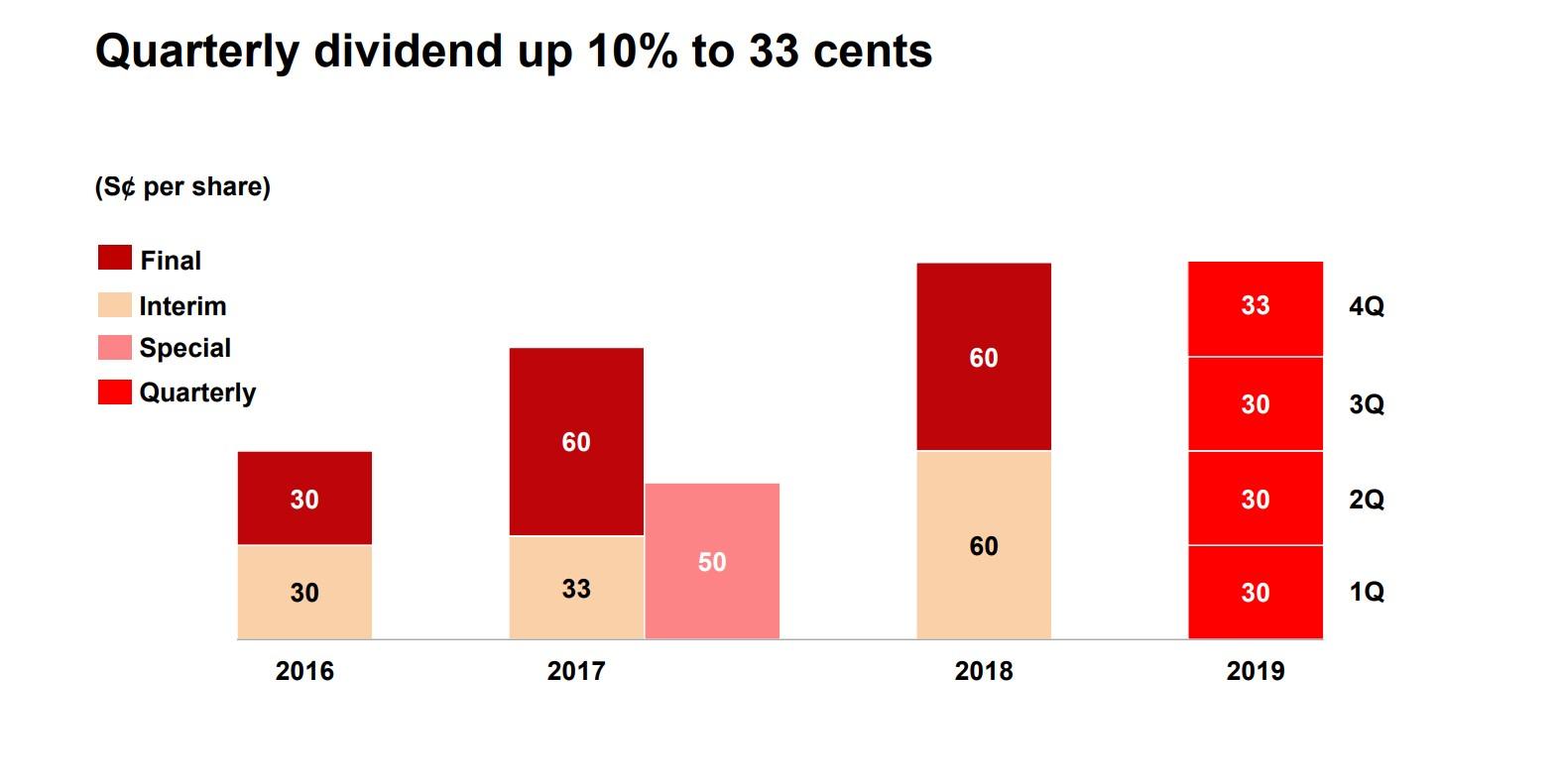

Source: DBS FY2019 Earnings Presentation

From the graph above, it can be seen that the bank’s core dividend had been increasing steadily, rising from S$0.60 in fiscal 2016 (FY2016) to S$1.23 in FY2019.

DBS even paid out a special dividend of S$0.50 to reward shareholders in FY2017.

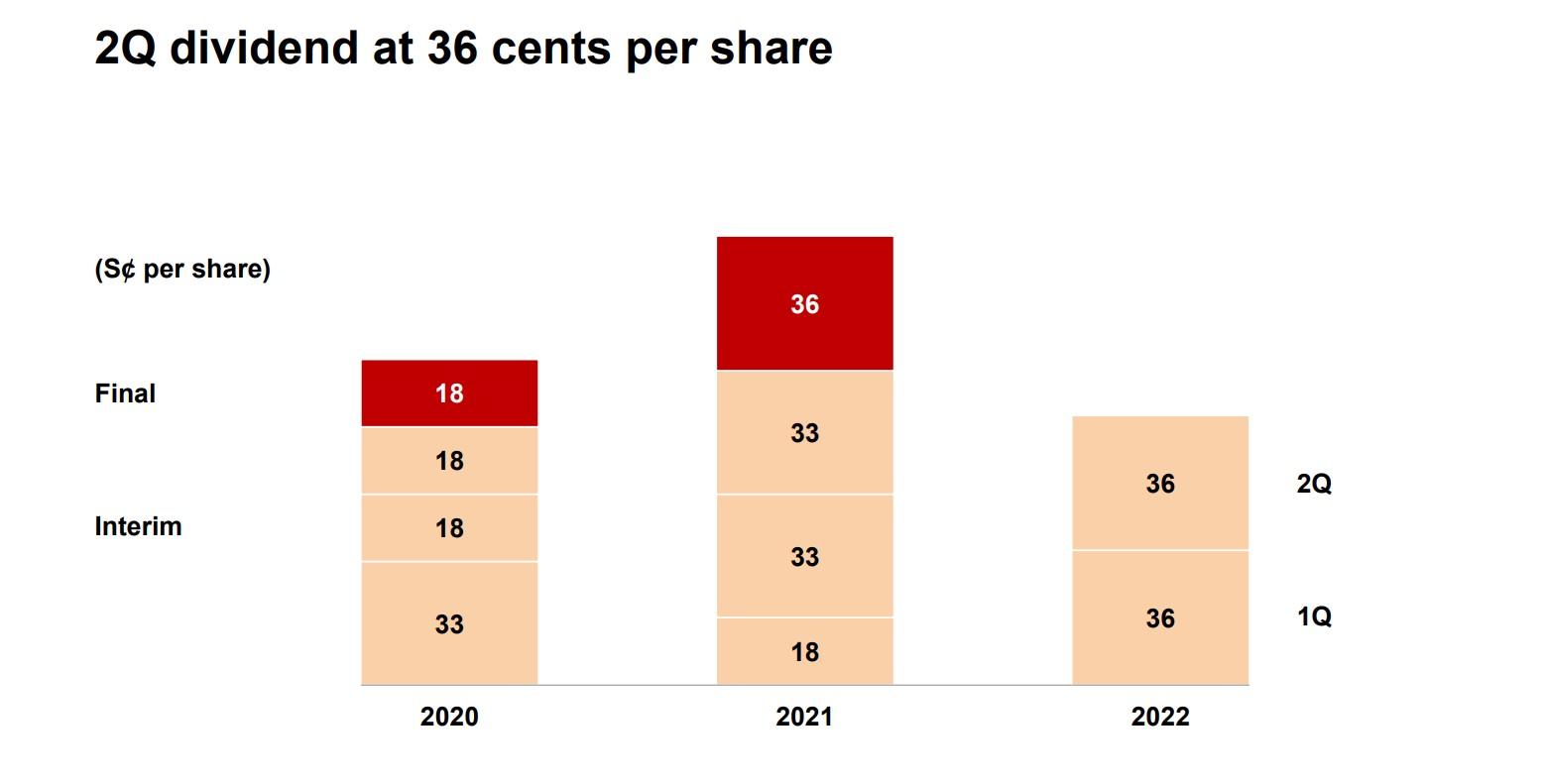

Source: DBS 2Q2022 Presentation Slides

During FY2020, DBS dropped its quarterly from S$0.33 to S$0.18.

The bank did this not because it wanted to, but because it was called on by the Monetary Authority of Singapore to pay out a maximum of 60% of its total dividend in the prior year.

As a result, DBS paid out S$0.18 per quarter in dividends for four straight quarters before restoring it to S$0.33 in the second quarter of 2021 (2Q2021).

In addition, the bank raised its quarterly dividend when it released its FY2021 earnings and reported a record net profit of S$6.8 billion.

The above illustrates the bank’s resilience when it comes to dividends as it only reduced it because of the central bank’s instruction.

Interest rate tailwinds

Now that we’ve looked at DBS’ dividend history, let’s discover if there are any tailwinds for the business to grow.

Banks’ main business relies on lending, which is highly sensitive to interest rates.

The good news is that the US Federal Reserve has hiked interest rates sharply in recent months, with three consecutive hikes of 0.75 percentage points each.

DBS reported a net interest margin (NIM) of 1.58% for 2022’s second quarter, with its first-half NIM coming in at 1.52%, up from the low of 1.43% in the second half of 2021.

In a sign of what’s to come, CEO Piyush Gupta said that July’s NIM was already above 1.8%, implying that the bank’s third-quarter NIM will probably be significantly higher than its second quarter.

For more context, DBS disclosed its interest rate sensitivity earlier this year.

Every percentage point rise in base interest rates will result in a net interest income (NII) uplift of S$1.9 billion.

We could see that happen.

From June to September, the US central bank raised its benchmark interest rate by a total of 2.25%.

Assuming the increases flow down to DBS’ NIM, there is the potential for NII to rise by S$4.2 billion, which is around half of FY2021’s total NII of S$8.44 billion.

To top it off, back in February this year, Mr Gupta had also communicated his willingness to pay out higher levels of dividends to shareholders should the lender benefit from higher rates.

Taking a leaf from US banks

If you’re still doubtful as to the effects of higher interest rates on banks’ NII, the latest earnings from several US banks have already demonstrated its impact.

Bank of America (NYSE: BAC) reported that its 2022’s third-quarter NII jumped 24% year on year to US$13.8 billion.

Meanwhile, JP Morgan Chase (NYSE: JPM) saw its NII surge by 34% year on year to US$17.6 billion while Wells Fargo (NYSE: WFC), a bank that Warren Buffet’s Berkshire Hathaway (NYSE: BRK.B) invests in, reported a 36% year on year climb in its NII.

These banks provide a taste of what’s to come for DBS when it reports its third-quarter earnings in early November.

Get Smart: A dividend increase seems highly likely

The evidence is clear.

DBS looks set to enjoy the tailwind of higher interest rates and its CEO has also communicated its intention to up its dividend.

Hence, income-seeking investors should rejoice as an imminent dividend increase seems highly likely.

In our special FREE report, Top 9 Dividend Stocks for 2022 – and 3 Tactical Shifts to Maximise Your Profits, we’re revealing 3 special categories of stocks that are poised to deliver maximum growth in 2022 and beyond.

Our safe-harbour stocks are a set of blue-chip companies that have been able to hold their own and deliver steady dividends. Growth accelerators stocks are enterprising businesses poised to continue their growth. And finally, the pandemic surprises are the unexpected winners of the pandemic.

Download for free to find out which are our safe-harbour stocks, growth accelerators, and pandemic winners! CLICK HERE to find out now!

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclaimer: Royston Yang owns shares of DBS Group.