The curtains are coming down for CapitaLand Limited (SGX: C31).

Last Friday, the real estate conglomerate released its final report card, bringing an end to its reign as a listed property development firm — at least, as we know it.

Earlier in March this year, CapitaLand revealed its plan to split the company into two: an investment management arm which will remain listed, and a property development arm that will be privatised.

The demerger received resounding approval from shareholders early last week.

But before the real estate firm ushers in a new beginning, there is the matter of its last-ever earnings report in its current form.

With that in mind, here are five things that investors should know.

1. Operational overview

CapitaLand delivered a final hurrah in the first half of 2021 with revenue rising 34.7% year on year to S$2.7 billion and operating profit (excluding exceptional items) soaring 66% year on year to S$433.6 million.

Over the same period, the real estate firm also generated S$625.4 million in operating cash flow, up from less than S$300 million a year ago.

Source: CapitaLand’s 1H 2021 earnings presentation

The gain in operating income led to higher profits.

Net profit, which includes portfolio gains and revaluations, rose to S$922.2 million, up almost 10 times from a year ago.

Profits received a big boost from portfolio gains of S$489 million of the quarter.

Source: CapitaLand’s 1H 2021 earnings presentation

CapitaLand also returned to profitability after posting a net loss of almost S$1.6 billion in 2020.

In sum, its operations are humming along nicely.

Meanwhile, in terms of its financial position, CapitaLand ended the quarter with S$7.8 billion in cash and cash equivalents and S$22.4 billion in debt together with around S$10.5 billion in debt securities (mainly notes and bonds).

2. Debt management

CapitaLand’s heavy debt load deserves more attention.

Source: CapitaLand’s 1H 2021 earnings presentation

As of 30 June 2021, CapitaLand’s debt had a maturity profile of 3.6 years.

The implied interest rate, calculated by dividing its finance cost (before capitalisation) against its overall debt, fell from 3% in 2020 to 2.8% for the first half of 2021.

For context, the company incurred financing costs of S$439 million for the first six months of the year.

Interest coverage ratio was 2.8 times, a vast improvement from the 0.7 times recorded in FY2020.

Note: the interest coverage ratio is based on its earnings before interest, taxes, depreciation and amortisation (EBITDA) divided by interest expense, and not EBIT (earnings before interest and tax).

Shareholders should also note that the company has a ready loan facility to draw down another S$7 billion.

3. Looking ahead: fee income

Looking ahead, the investment management arm will be renamed CapitaLand Investment Management or CLIM.

Unlike CapitaLand, CLIM is solely focused on growing its funds under management (FUM) and its fee income, which is recurring in nature.

In essence, if FUM increases, fee income should grow alongside.

Source: CapitaLand’s 1H 2021 earnings presentation

CapitaLand closed the first half at S$83 billion in FUM, a 7% increase from the FUM of S$77.6 billion recorded at the end of 2020.

The vast majority of the FUM is in China (S$28.1 billion) and Singapore (S$34.8 billion).

From the FUM, fee income came in at S$188.7 million for 2021’s first half (1H 2021), up 28.7% year on year from the fee income of S$146.6 million a year ago.

For completeness, on a pro-forma basis, CLIM is expected to hold S$13.8 billion in total debt and sport a 0.72 debt to equity ratio after the demerger.

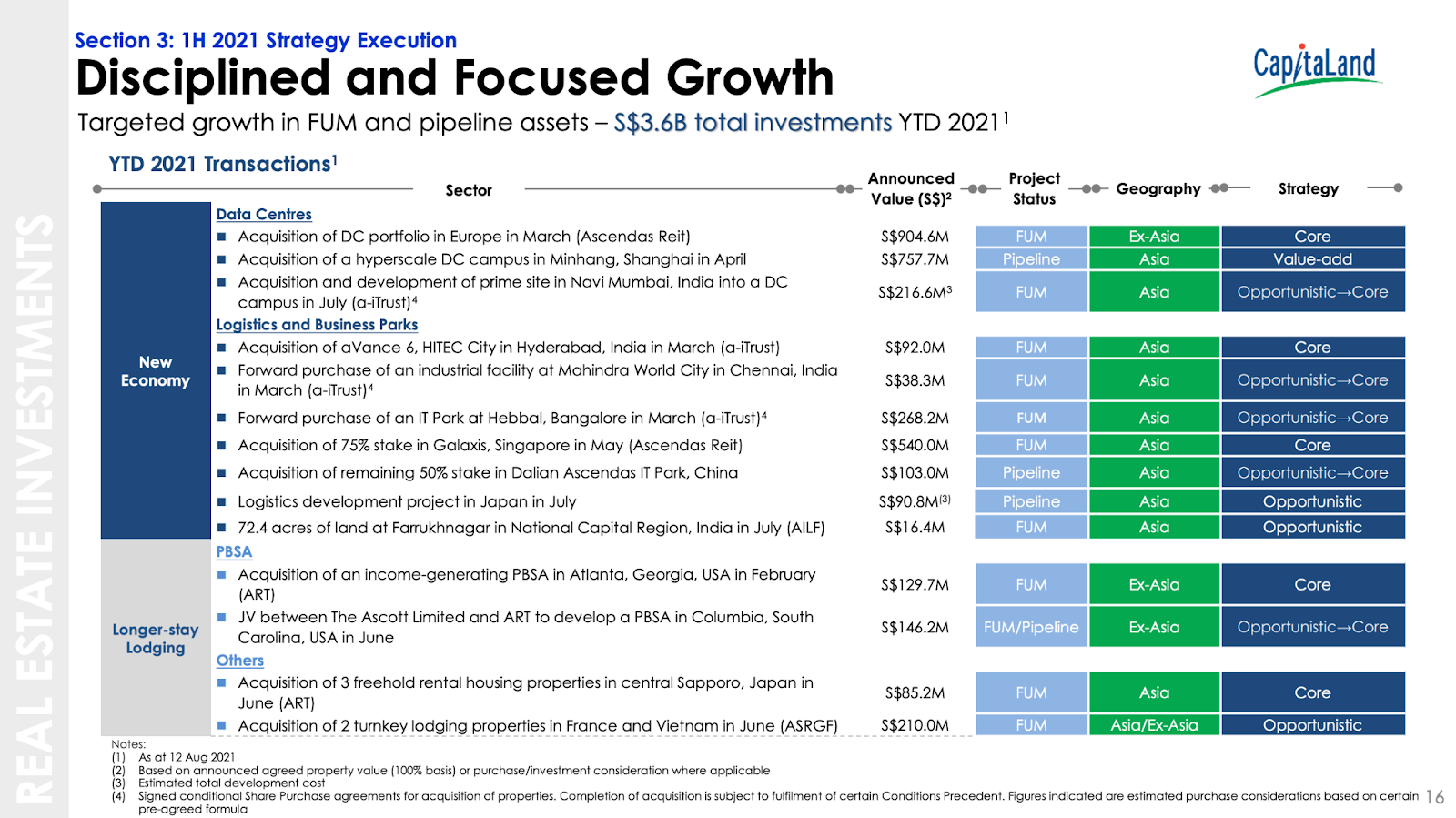

4. Looking ahead: investments and divestments

CapitaLand has a general target of recycling S$3 billion of its assets every year.

The real estate firm is running well ahead of goal this year, with S$11.2 billion in gross divestment value and S$3.3 billion in effective divestment value so far in 2021.

Source: CapitaLand’s 1H 2021 earnings presentation

In turn, these funds have been re-invested mainly into “new economy” assets such as data centres (around S$1.9 billion) and logistics and business parks (about S$1.1 billion).

Overall, CapitaLand has made S$3.6 billion in total investment for the year to date, as shown below.

Source: CapitaLand’s 1H 2021 earnings presentation

The remaining S$0.6 billion were allocated to purpose-built student accommodation (PBSA; S$275 million) and other lodging facilities (S$295 million).

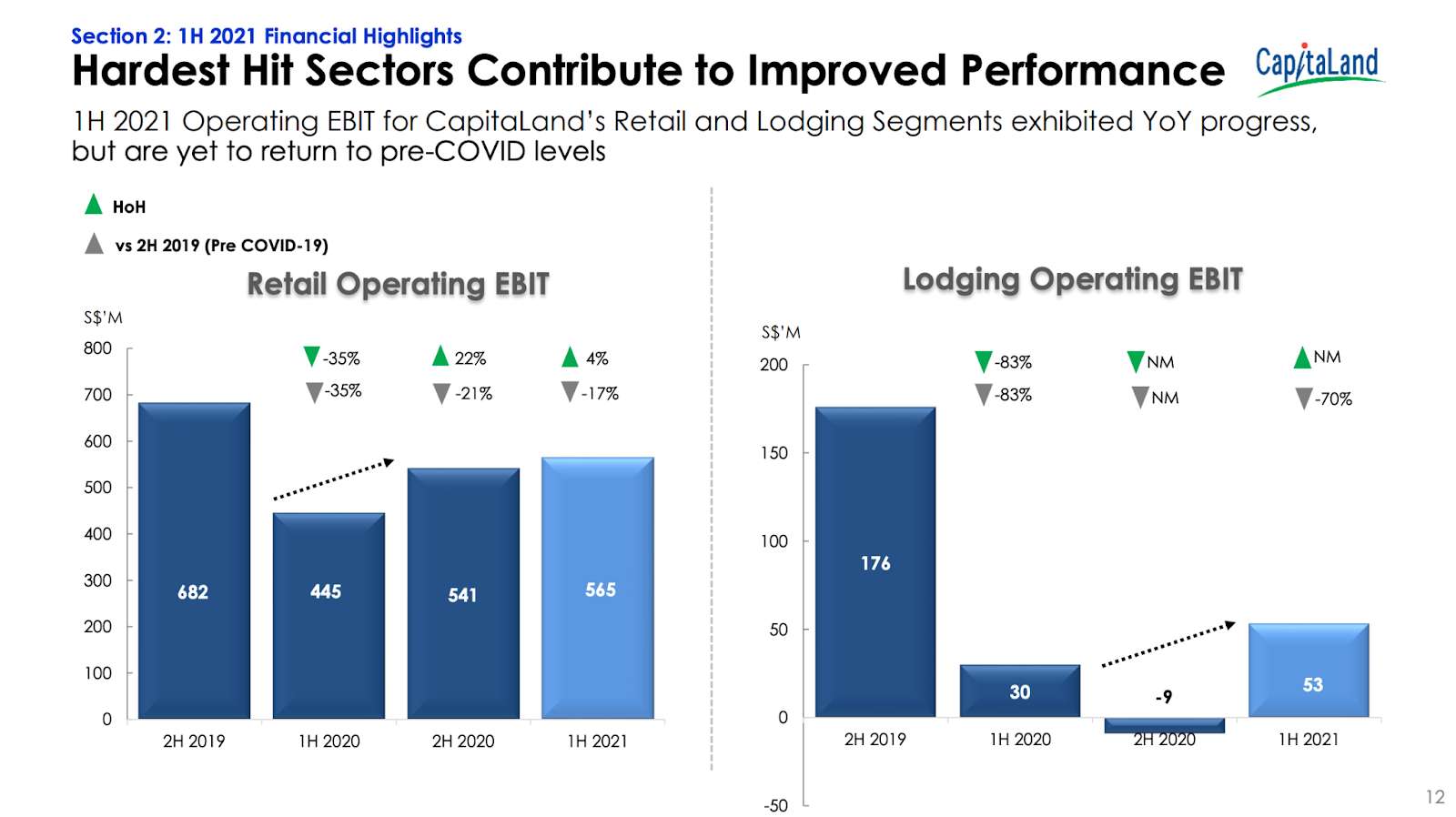

5. Looking ahead: green shoots of recovery

Speaking of lodging, green shoots of recovery have emerged for some of the hardest hit sectors within CapitaLand, namely its retail and lodging operations.

Source: CapitaLand’s 1H 2021 earnings presentation

As you can see above, the retail operating EBIT for 1H 2021 rose 27% year on year to S$565 million but remains 17% below the segment’s EBIT level set in 2H 2019.

Meanwhile, lodging operations produced a turnaround, turning in a S$53 million in EBIT for 1H 2021, compared to a loss in 2H 2020.

That said, the current EBIT level for lodging remains far below the EBIT recorded in 2019.

Accelerate your retirement plans with these 5 SGX stocks. Their dividends are climbing, and are well-positioned to weather through storms in the future. We think at least one of them deserves a spot in your portfolio. To find out their names, grab a copy of your FREE special report:“Dividend Stocks That Can Pay You For Life” today. Click here to download now.

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclosure: Chin Hui Leong does not own shares of CapitaLand.