REITs are back in vogue as global economic recovery takes hold.

Investors who are looking to boost their passive income stream are in luck.

Singapore, being an established REITs hub, has a tasty selection of high-quality REITs to choose from.

The question should centre around which REIT qualifies as a more attractive long-term income investment?

To answer that, we decided to take a look at two popular REITs.

The first is Frasers Centrepoint Trust (SGX: J69U), or FCT, a retail REIT that owns a portfolio of nine suburban malls and an office building in Singapore.

The other is Mapletree Commercial Trust (SGX: N2IU), or MCT, a retail cum commercial REIT that owns Singapore’s largest shopping mall, VivoCity, as well as four commercial properties Mapletree Business City (MBC), mTower, Mapletree Anson and Merril-Lynch Harbourfront (MLHF).

Both REITs have strong sponsors with FCT backed by property giant Frasers Property Limited (SGX: TQ5) and MCT by investment firm Mapletree Investments Pte Ltd.

So, let’s look at various aspects of each REIT to determine which is the better buy at this time.

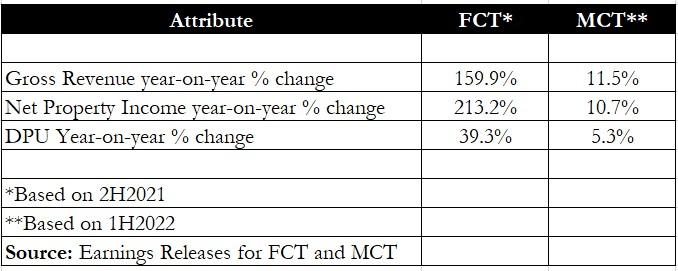

Revenue and net property income

First off, we compare the year on year increases in gross revenue, net property income (NPI) and distribution per unit (DPU).

Investors should note that FCT has a 30 September fiscal year-end while MCT has a 31 March fiscal year-end.

To ensure fairness in comparison, the second half of fiscal 2021 (2H2021) was used for FCT while the first half of fiscal 2022 (1H2022) was used for MCT.

The period under observation is similar for both, from 1 April 2021 to 30 September 2021.

FCT saw a huge year on year surge in revenue and NPI due to the full-year recognition from its purchase of five suburban malls from the AsiaRetail Funds portfolio.

MCT did reasonably well too, logging a healthy 11.5% year on year increase in gross revenue and a 10.7% year on year increase in NPI.

FCT’s DPU jumped by 39.3% year on year while MCT chalked up a smaller, but still respectable, 5.3% year on year DPU increase.

Winner: FCT

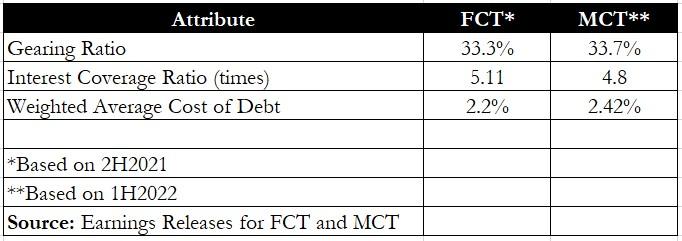

Gearing and debt servicing

Next, we looked at both REITs’ gearing levels, interest coverage ratio (ICR) and cost of debt.

Gearing for both REITs was below 35%, allowing them to have sufficient debt headroom for more acquisitions.

The ICR for FCT was slightly higher than that of MCT, while it also has a slightly lower cost of debt.

Winner: FCT

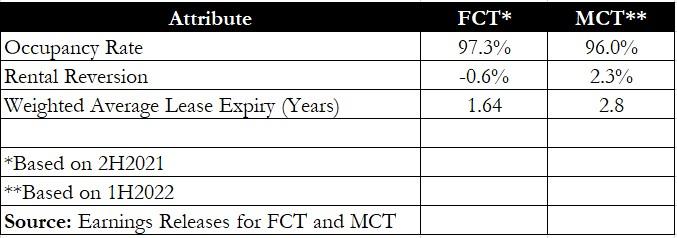

Operating metrics

The occupancy rate for both REITs remains high at above 95%, a good sign that most tenants are renewing their leases and staying on.

However, FCT reported a slightly negative rental reversion of -0.6% as this was based on the final year rent of the outgoing lease versus the first year of the incoming lease.

If the average rent is used for both incoming and outgoing leases, then rental reversion would be positive at 2.1%.

Even at 2.1%, FCT’s rental reversion still falls slightly short of MCT’s 2.3%.

Meanwhile, FCT also has a shorter weight average lease expiry (WALE) at 1.6 years as the REIT deals with retail leases that are generally shorter in length.

MCT’s overall portfolio WALE of 2.8 years consists of a mix of retail WALE of 2.2 years and office cum business park WALE of 3.3 years.

Winner: MCT

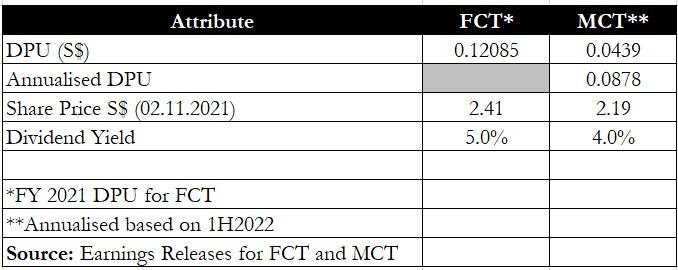

Dividend yield

Finally, we look at the dividend yield that unitholders will obtain if they purchase units of the REIT at their current prices.

We used FCT’s FY2021 DPU but annualised MCT’s half-year DPU for this exercise.

There is a clear difference here — FCT’s dividend yield is 5% versus MCT’s 4%, making FCT the more attractive REIT in terms of dividend yield.

Winner: FCT

Other aspects

Aside from the attributes stated above, it’s also instructive to look at each REIT’s acquisition track record and the nature of its assets.

For MCT, its latest acquisition was that of Mapletree Business City Phase 2 back in November 2019, a follow-up to its purchase of Phase 1 in August 2016.

Over at FCT, the REIT had recently completed its acquisition of the aforementioned five malls and has also divested three malls since September last year — Bedok Point, Anchorpoint and Yew Tee Point.

Between the two, FCT has been more active in its capital recycling strategy to refresh its portfolio.

Another point to note is that FCT’s malls are located in suburban areas and serve largely heartlanders who are shopping for essential goods and necessities.

This attribute makes these malls more resilient to economic downturns as foot traffic and tenant sales remain at healthy levels.

In contrast, VivoCity (under MCT) thrives more on tourism which has been badly impacted by border closures.

The mall takes up 34.1% of MCT’s revenue and around 32% of NPI for 1H2022.

Recovery may take a while for the REIT and it seems that, for now, FCT will be the better choice for those who seek a good dividend yield and a resilient property portfolio.

Here are 5 cash-rich companies so healthy, they can pay you dividends for life. The names of these SGX stocks are in our special FREE report. Download it here and start building your dream retirement portfolio today!

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclaimer: Royston Yang does not own shares in any of the companies mentioned.