Singapore is well known as a shoppers’ paradise.

Family outings at malls are a common weekend activity, and the island is dotted with malls of all shapes and sizes for the discerning consumer to choose from.

That is also why retail REITs tend to do well.

However, the COVID-19 pandemic has drastically altered the retail landscape.

Retail REITs suffered adverse effects from these tough measures as shopper traffic dried up and tenants faced financial pressure.

REIT managers had to dole out tenant relief measures to support their tenants, and many were forced to slash their distribution per unit (DPU).

We take a look at two popular retail REITs, CapitaLand Mall Trust (SGX: C38U), or CMT; and Frasers Centrepoint Trust (SGX: J69U), or FCT, to see which makes the better investment choice.

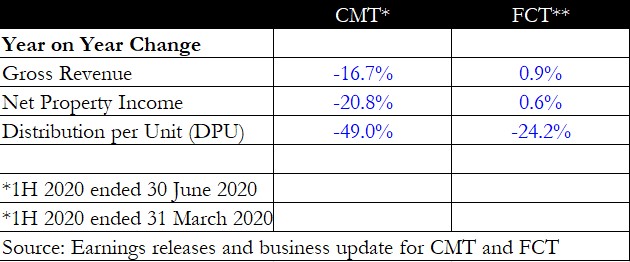

Financial performance

We start by comparing the financial performance of each REIT.

However, do note that CMT and FCT have different fiscal year-ends. For CMT, it is December 31, hence its reporting period for the first half is until 30 June 2020.

FCT has a September 30 year-end, which means its first-half earnings represent performance from 1 October 2019 till 31 March 2020.

For FCT’s third quarter ended 30 June 2020, the REIT has provided a business update without any numbers for revenue, net property income (NPI) or DPU.

Still, we managed to do a comparison of each of the REIT’s half-year performance.

FCT displays a better performance when compared to CMT but the period excludes the crucial circuit breaker period for the April to June quarter, hence we will be looking at other aspects to determine performance.

Winner: FCT (for now)

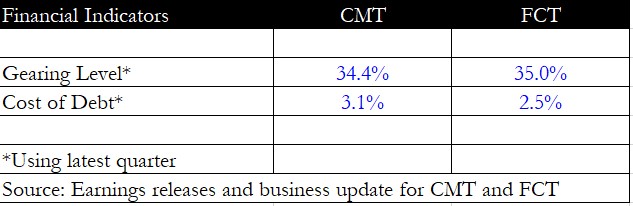

Financial indicators

For financial metrics, FCT’s gearing level is slightly higher than CMT, but its cost of debt is much lower at 2.5% versus 3.1%.

This means that FCT can squeeze out more savings on finance costs compared to CMT.

That said, FCT has recently announced a major acquisition to acquire the remaining 63.1% stake in AsiaRetail Fund Limited for S$1.06 billion.

As a result, the REIT’s gearing will rise to 39.3% but its average cost of debt will fall to 2.3%.

As both REITs’ gearing level is still below the 50% maximum threshold set by the Monetary Authority of Singapore, we feel the cost of debt metric is the more important one to look at, and FCT wins by a wide margin.

Winner: FCT

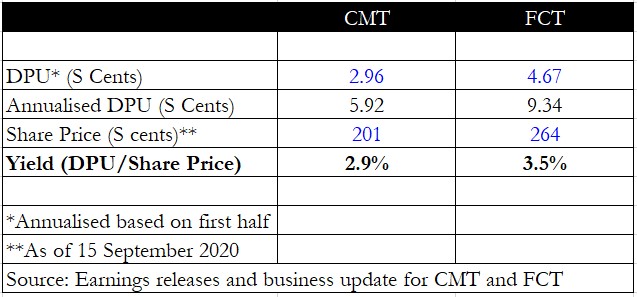

Dividend yield

Next, we compared the dividend yield for both REITs.

The DPU declared for the half-year was annualised to estimate the full-year DPU.

Investors should also note that this is not an exact estimation due to the effects from COVID-19, and also because FCT had not declared any DPU in its latest quarter ended June.

The results show that FCT sports a slightly higher dividend yield of 3.5% compared to CMT’s 2.9%.

Winner: FCT

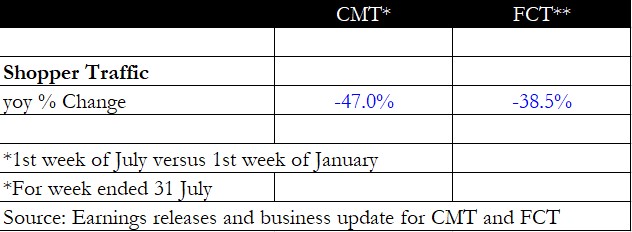

Shopper traffic

Finally, we looked at shopper traffic trends for both REITs as a way to gauge how well each REIT is coping with COVID-19.

Although the periods do not overlap exactly, FCT does display a slightly better recovery than CMT as the drop is 38.5% year on year compared to a steeper 47%.

Investors should note that this could be due to FCT’s portfolio being predominantly suburban malls, where shopper footfall has generally held up better due to locals patronising these malls.

CMT’s portfolio consists of several malls such as Raffles City, Clarke Quay and the Atrium @ Orchard that rely more heavily on tourist footfall, a crowd that has been absent even after the circuit breaker period ended.

Winner: FCT

Plans for the future

It seems that FCT has won on all counts, but do note that part of the reason is because of the lack of financial numbers for the REIT’s latest quarter.

Still, if we go by qualitative metrics, FCT’s malls are enjoying a much better recovery as a whole compared to CMT.

FCT’s latest acquisition also helps to diversify its portfolio further as the number of suburban retail malls within the REIT’s portfolio will increase from seven to 12.

This fact makes the REIT more resilient during the pandemic and it should also see a better recovery for tenant sales post-crisis.

CMT is currently going through a merger with CapitaLand Commercial Trust (SGX: C61U) that will introduce commercial properties into the combined REIT.

The merger will help to diversify the asset profile for CMT away from being purely retail, but there is also a concern as to whether commercial property occupancy and rentals can hold up as more people telecommute.

FCT is not without its risks, though.

The pandemic situation is still evolving and there could still be further financial stress for tenants, so investors need to keep abreast with the latest developments for the REIT.

With share prices battered to multi-year lows, many attractive investment opportunities have emerged. In a special FREE report, we show you 3 stocks that we think will be suitable for our portfolio. Simply click here to scoop up your FREE copy… before the next stock market rally.

Click here to like and follow us on Facebook, here for our Instagram group and here for our Telegram group.

Disclaimer: Royston Yang does not own shares in any of the companies mentioned.