Commodity prices have been on the rise since the Russia-Ukraine war broke out, coupled with rising inflation.

According to The Food and Agriculture Organisation of the United Nations, the food price index rose a record 12.6% from February to March this year alone.

As investors, it is hard not to feel worried.

Everything from animal feed and grains to food prices is increasing at an alarming pace.

Inflation is not equal for all companies out there, especially those dealing with food-related sources.

We take a look at three companies with specific advantages in their value chain that can help them to overcome inflation.

1. Wilmar International Limited (SGX: F34)

Wilmar International Limited, or Wilmar, is a leading agribusiness group with an integrated business model.

It grows, mills, processes, brands, and distributes a wide range of commodities and food products such as animal feed and biodiesel.

This blue-chip has a wide distribution network across 50 other countries and regions, with more than 500 manufacturing plants.

Wilmar enjoys logistical advantages that allow it to extract margins at every step of the value chain.

Nonetheless, the COVID-19 slowdown and weak crush margins in China from rising soybean prices have been felt by both its Feed and Industrial Product and Consumer Pack Oil segments.

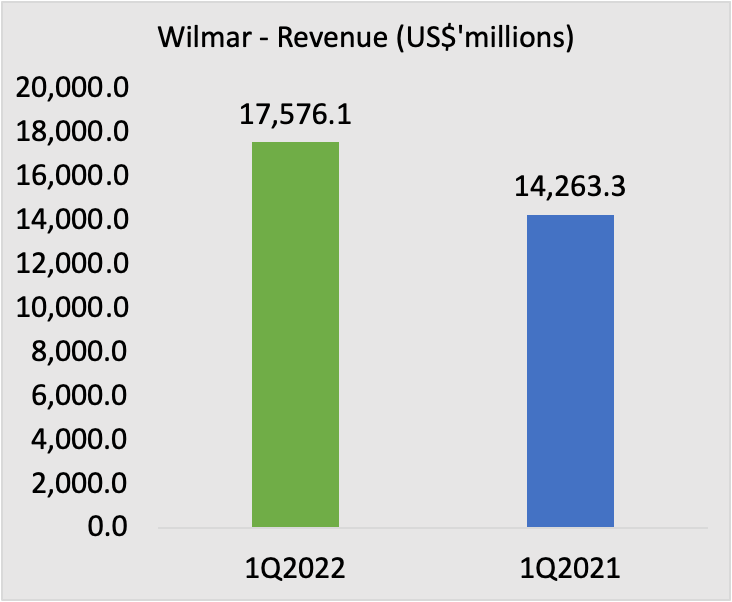

In its fiscal 2022 first quarter (1Q2022), Wilmar reported a 23.2% year on year jump in revenue to US$17.6 billion.

Core net profit rose by 18.8% year on year to US$503.4 million. This good performance was attributable to strong performances from its Plantation and Sugar milling segment, aided by firm palm oil prices.

|  |

Source: Wilmar’s 1Q2022 Financial Summary, Revenue and Core Net Profit

Wilmar’s expansion into more flour milling plants in 2021 has enabled the group to fulfil increased demand.

This expansion drove volume growth in flour products that resulted in a growth in sales volume for medium pack and bulk food products to 4.6 million metric tonnes, compared with 4.5 million metric tonnes a year ago.

Overall, inclusive of non-operating gains, the group’s total net profit for 1Q2022 rose 17.8% year on year to US$530.3 million.

2. Japfa Ltd (SGX: UD2)

Japfa Ltd, or Japfa, is a leading pan-asian industrial agri-food company. It produces protein staples from poultry, swine, aquaculture, beef to dairy.

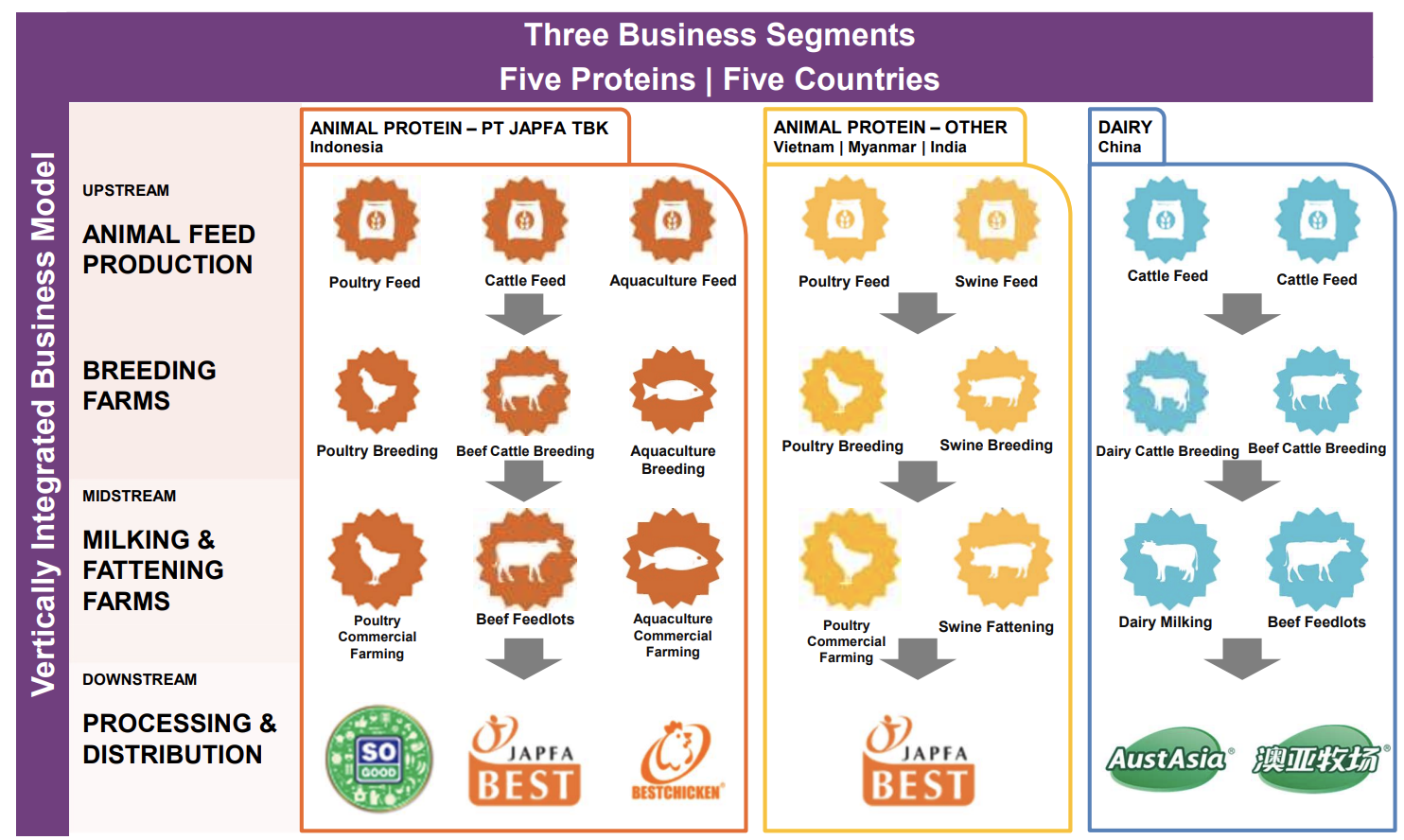

Its focus is on staple proteins such as poultry, to high growth markets in Asia. Japfa has two main business segments; Animal Protein, and Dairy.

Japfa has a complete integrated value chain from upstream; which deals with animal feed production and breeding farms, to downstream; which deals with processing and distribution.

Source: Japfa 1Q2022 investor presentation, business segments breakdown

Geographically, Japfa’s revenue comes from Indonesia, Vietnam, Myanmar, India, Bangladesh, and China.

Japfa is currently the second largest poultry company in Indonesia.

In its 2022 corporate presentation, Japfa’s poultry feed has an approximate 21% market share in Indonesia, according to research firm Frost and Sullivan.

In view of the chicken ban imposed by Malaysia on Singapore from 1 June 2022, Singapore had also started talks with Indonesia to include the country as an alternative chicken supplier.

On June 30, Indonesia was approved as a new source for the import of chilled, frozen and processed chickens into Singapore.

With this development Japfa will be able to benefit from the political tailwind.

Japfa reported 1Q2022 revenue of US$1.25 billion, representing a year on year increase of 13%, mainly driven by higher sales across all its operating segments.

However, as a result of high global raw material prices, inflationary pressures, the Asian swine flu, and COVID-19, net profit plunged 64.3% year on year to US$17.3 million for the quarter.

Japfa has generally been able to pass on higher raw material costs in its selling prices.

With the higher expected average selling prices for feed around the world, Japfa is likely to benefit from this trend.

3. Sheng Siong Group Ltd (SGX: OV8)

Sheng Siong Group Ltd is a well known local brand among Singaporeans.

It is one of the largest supermarket chain operators in Singapore with 65 outlets island-wide, and known for the provision of necessity-based shopping.

Many would have thought cost pressures from supply chain lockdowns and increased food prices would be a drag for Sheng Siong.

Due to the critical mass and economies of scale that Sheng Siong has, it has managed to keep its overall margins stable.

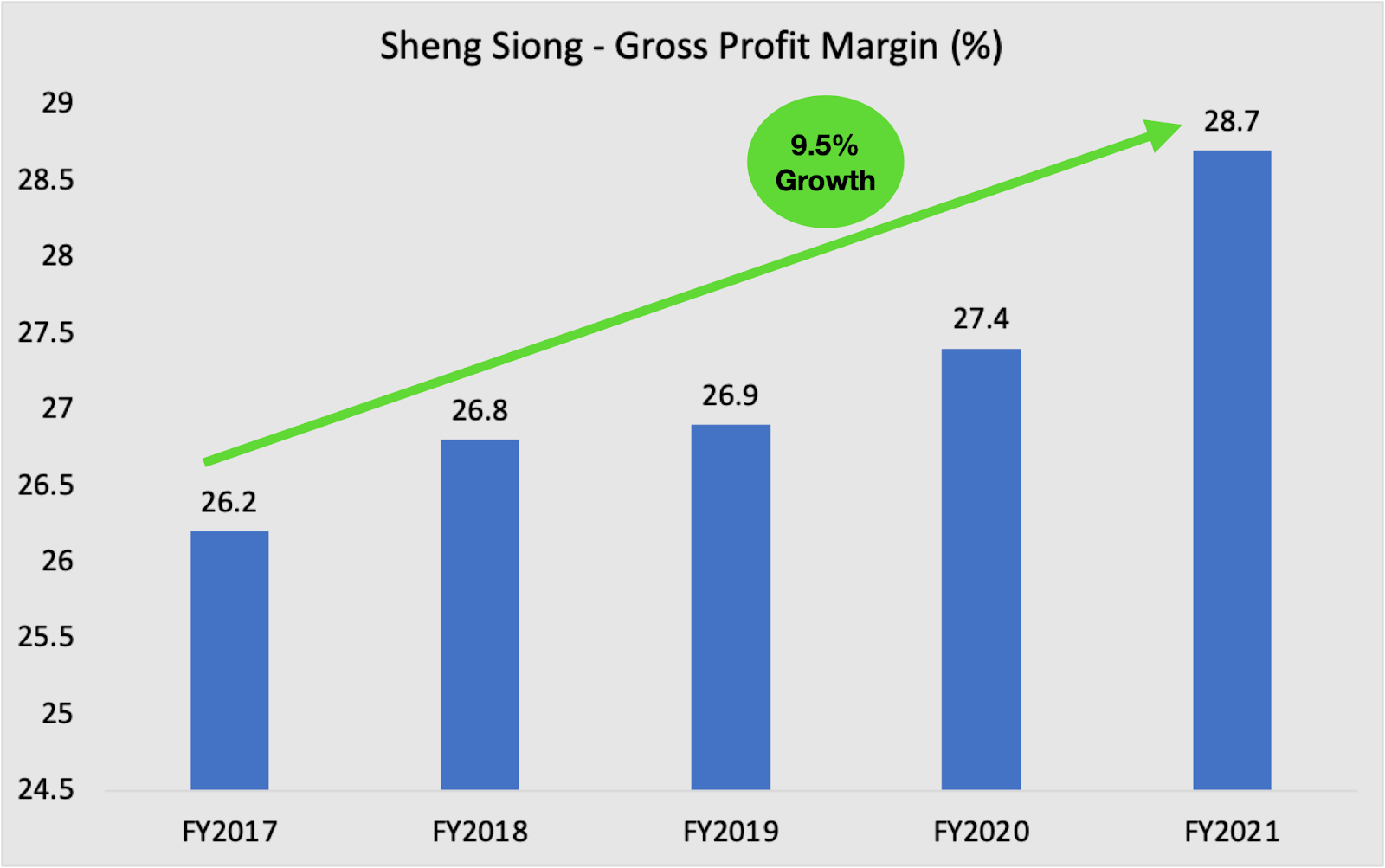

A closer look at its gross margins revealed that not only does Sheng Siong manage to keep a lid on the growing costs, it has also consistently generated higher gross margins over time.

Source: Sheng Siong investor relations; author’s compilation

Gross profit margins have grown by 9.5% from 26.2% to 28.7% between FY2017 to FY2021.

Sheng Siong’s long term growth is to open three to five stores per year over the next three to five years.

For FY2021, a total dividend of S$0.062 per share was paid out.

At a unit price of S$1.57, this translates to a dividend yield of 3.9%.

In our special FREE report, Top 9 Dividend Stocks for 2022 – and 3 Tactical Shifts to Maximise Your Profits, we’re revealing 3 special categories of stocks that are poised to deliver maximum growth in 2022 and beyond.

Our safe-harbour stocks are a set of blue-chip companies that have been able to hold their own and deliver steady dividends. Growth accelerators stocks are enterprising businesses poised to continue their growth. And finally, the pandemic surprises are the unexpected winners of the pandemic.

Download for free to find out which are our safe-harbour stocks, growth accelerators, and pandemic winners! CLICK HERE to find out now!

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclaimer: Kent Lee owns shares of Sheng Siong.

")