News broke on Wednesday that Iran has fired missiles at US troops stationed in Iraq, in retaliation for the death of a top Iranian general at the hands of the US military.

Could Iran’s latest move escalate into a full-blown war between itself and the US?

I have no idea.

My heart sinks at the thought of the human lives that could be painfully ended or maimed because of any potential large-scale armed conflict.

May a war not happen. The human costs are too tragic.

But what if tensions between Iran and the US erupt and a huge battle develops? What happens to the financial markets? In this uncertain time, it’s worth remembering that:

- The US experienced a recession in July 1990

- The US entered into a war in the Middle East in August 1990.

- The price of oil spiked in August 1990.

- Ray Dalio said in early 1992 that “unfortunately… the current economic climate of low inflation and historically slow growth means that bonds will actually prove to be the better long-term performers.”

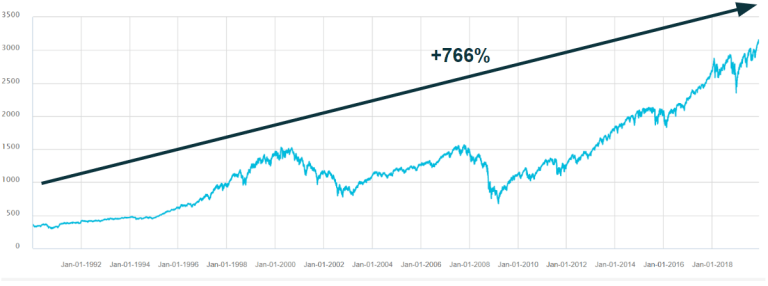

But from the start of 1990 to today, the US stock market is up nearly 800% in price alone (the chart below shows the price-change for the S&P 500 from the start of 1990 to early December 2019):

Source: S&P Global Market Intelligence

Every time I’m confronted with uncertainty in the markets, I turn to one of my favourite investing passages. It’s written by Warren Buffett in his Berkshire Hathaway 1994 shareholders’ letter:

“We will continue to ignore political and economic forecasts, which are an expensive distraction for many investors and businessmen.

Thirty years ago, no one could have foreseen the huge expansion of the Vietnam War, wage and price controls, two oil shocks, the resignation of a president, the dissolution of the Soviet Union, a one-day drop in the Dow of 508 points, or treasury bill yields fluctuating between 2.8% and 17.4%.

But, surprise – none of these blockbuster events made the slightest dent in Ben Graham’s investment principles. Nor did they render unsound the negotiated purchases of fine businesses at sensible prices.

Imagine the cost to us, then, if we had let a fear of unknowns cause us to defer or alter the deployment of capital. Indeed, we have usually made our best purchases when apprehensions about some macro event were at a peak. Fear is the foe of the faddist, but the friend of the fundamentalist.

A different set of major shocks is sure to occur in the next 30 years. We will neither try to predict these nor to profit from them. If we can identify businesses similar to those we have purchased in the past, external surprises will have little effect on our long-term results.”

This too, shall pass. But again, may war not happen.

Get more stock updates on our Facebook page. Click here to like and follow us on Facebook.

If you’d like to learn more investing concepts, and how to apply them to your investing needs, sign up for our free investing education newsletter, Get Smart! Click HERE to sign up now.

The Smart Investor is not licensed or otherwise regulated by the Monetary Authority of Singapore, and in particular, is not licensed or regulated to carry on business in providing any financial advisory service.

Accordingly, any information provided on this site is meant purely for informational and investor educational purposes and should not be relied upon as financial advice. No information is presented with the intention to induce any reader to buy, sell, or hold a particular investment product or class of investment products. Rather, the information is presented for the purpose and intentions of educating readers on matters relating to financial literacy and investor education. Accordingly, any statement of opinion on this site is wholly generic and not tailored to take into account the personal needs and unique circumstances of any reader. The Smart Investor does not recommend any particular course of action in relation to any investment product or class of investment products. Readers are encouraged to exercise their own judgment and have regard to their own personal needs and circumstances before making any investment decision, and not rely on any statement of opinion that may be found on this site.

Disclosure: Chong Ser Jing owns shares of Berkshire Hathaway.

Note: An earlier version of this article was published at The Good Investors, a personal blog run by our friends.