It’s a sign of the times.

A surge in interest rates caused by four consecutive rate hikes of 0.75 percentage points each from the US Federal Reserve has led to all three local banks reporting record results for their fiscal 2022’s third quarter (3Q2022).

United Overseas Bank Ltd (SGX: U11), or UOB, kicked off the banks’ earnings season by reporting a net profit of S$1.4 billion.

Singapore’s largest bank, DBS Group (SGX: D05), also reported a record net profit of S$2.24 billion for 3Q2022 while peer OCBC Ltd (SGX: O39) chalked up its highest-ever net profit of S$1.6 billion.

Investors are now faced with a happy dilemma.

With the trio of banks reporting stellar sets of earnings, which should you pick to include in your buy watchlist?

We break down the various components for all three banks to try to determine this.

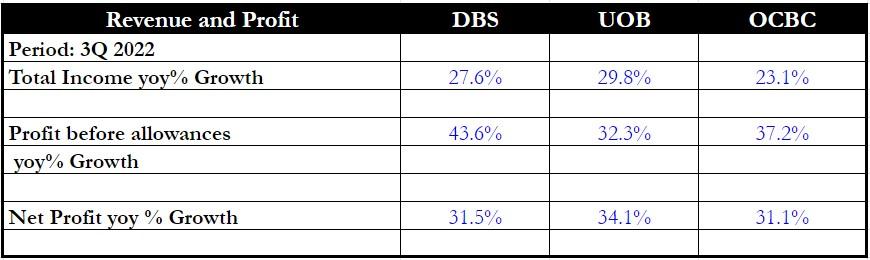

Income and net profit

Source: Banks’ earnings, author’s compilation

First, we look at the three banks’ financials.

All three saw their total income shoot up as higher interest rates led to a surge in net interest income (NII).

UOB is the winner when it comes to total income growth, chalking up a 29.8% year on year rise to S$3.2 billion, led by a surge in NII by 39% year on year to S$2.2 billion.

DBS came in a close second with its NII jumping 44% year on year to S$3 billion, but this good performance was offset by weaker fee income, which declined by 13% year on year to S$771 million.

After factoring in allowances, amortisation and results of associates, UOB came out tops with a 34.1% year on year rise in net profit to S$1.4 billion.

Winner: UOB

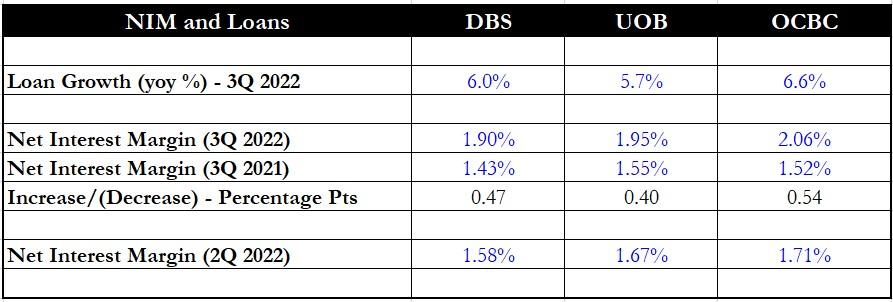

NIMs and loan book

Source: Banks’ earnings, author’s compilation

Next, we look at each bank’s NIMs and loan book.

As mentioned earlier, the sharp rise in interest rates benefitted all three banks, leading to a sharp rise in their NIM and, consequently, their NII.

Of the three banks, OCBC saw the biggest year on year increase in NIMs, rising by 0.54 percentage points to 2.06%.

The other two banks also saw large increases in NIM but DBS’ NIM ended 3Q2022 at 1.9% while UOB’s stood at 1.95%, below the 2% threshold.

Hence, OCBC is the clear winner here as it managed to ride on the interest rate tailwind to generate a much higher NIM than its two peers.

It’s interesting to note that back in 2Q2022, OCBC also had the highest NIM of the three banks.

Moving on to loan growth, OCBC also emerges as the winner with a 6.6% year on year rise in its loan book to S$299.8 billion.

All three banks reported healthy positive year on year growth in their loan books as the economic environment remains benign.

Winner: OCBC

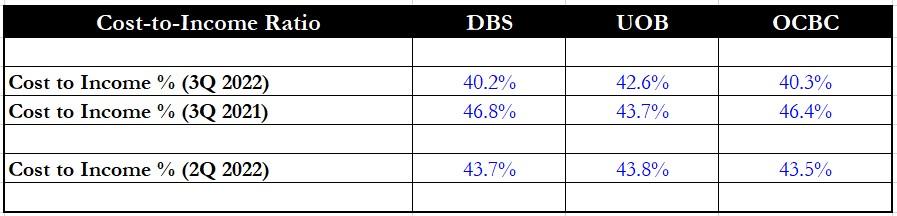

Cost-to-income ratio

Source: Banks’ earnings, author’s compilation

The next aspect we look at is the banks’ cost-to-income ratio, which measures the level of expenses in relation to each bank’s total income.

The lower this cost, the more efficiently a bank operates.

DBS and OCBC are pretty close on this metric as the former has a cost-to-income ratio of 40.2% while the latter’s stood at 40.3%.

If we look back at 3Q2021 and 2Q2022, DBS was lagging behind OCBC slightly while UOB was the clear winner in 3Q2021 with the lowest cost-to-income ratio.

Hence, the conclusion is that DBS has seen the largest improvement in its cost-to-income ratio among the three banks.

Winner: DBS

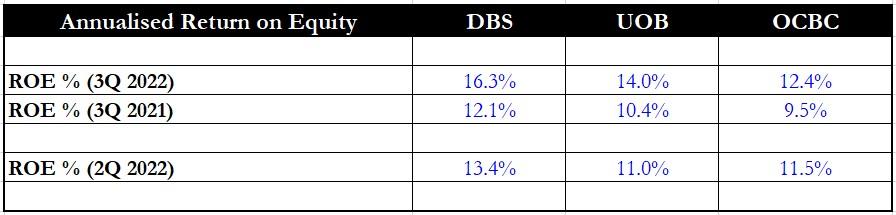

Return on equity

Source: Banks’ earnings, author’s compilation

Next, we look at the banks’ return on equity or ROE.

ROE is a measure of profitability and demonstrates how efficiently shareholders’ capital is used to generate a net profit.

For this financial metric, DBS stands above the rest with its ROE for 3Q2022 exceeding 16%.

From the table above, we can also note that historically, DBS has always had the highest ROE among the three banks.

As NII rises and leads to a boost in net profit, all three banks’ ROE should also rise correspondingly.

Winner: DBS

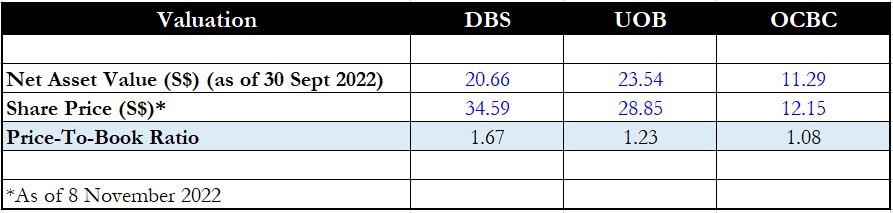

Valuation

Source: Banks’ earnings, author’s compilation

Finally, we look at each bank’s valuation as measured by its price-to-book (PB) ratio.

As in previous quarters, DBS once again emerges as the most expensive bank of the trio with a PB ratio of 1.67 times.

OCBC, on the other hand, is the cheapest and is trading just above its book value of S$11.29.

DBS is trading at the highest premium to its book value probably because it is also generating the highest ROE among the three banks.

Investors should also note that DBS pays a quarterly dividend compared with the other two banks that pay out half-yearly dividends.

For 3Q2022, DBS’ interim dividend declared stood at S$0.36 per share.

Winner: OCBC

Get Smart: A good mix of attributes

There is no clear winner for this round as each bank has won in at least one of the categories.

The good news is that you can always include all three banks as part of your buy watchlist if you cannot decide which is the best.

With rising interest rates as a tailwind, all three should likely continue to do well.

This could be the fastest way to jump from a “newbie” investor to a seasoned pro. Our beginner’s guide shows everything you need to know to buy your first stock and beyond. Click here to download it for free today.

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclaimer: Royston Yang owns shares of DBS Group.