Becoming a millionaire by age 40 sounds like an ambitious goal, because many think that it requires a fat paycheck right out of school or amazing stock-picking abilities.

However, true wealth can actually come from small, disciplined financial decisions made consistently over time.

Before hitting seven figures, break it down into bite-sized, smaller milestones, like the first S$10,000.

Achieving the first five-figure sum is the hardest part when you first start out, but it builds the foundation needed for long-term wealth.

Why the First S$10,000 Matters So Much

Accumulating your first S$10,000 requires everyday discipline, like skipping a few expensive weekend cafe brunches or holding back on phone upgrades just because a new model was dropped.

This boundary builds important muscle memory.

Upon achieving S$10,000, you transition from saving to investing.

Your capital can now be deployed into the market to provide you with another stream of passive income alongside your salary.

When this happens, you also fundamentally change how you view money.

You start asking “What stock or REIT should I own?” rather than looking at a retail storefront and thinking, “What can I buy?”

The Hidden Superpower: Time

The best asset you can own at 25 is not a finance degree from a prestigious university or amazing stock-picking abilities, but a long investment runway.

Starting early gives you decades for compounding to do the hard work while providing plenty of breathing room to recover from inevitable market bumps.

For example, you can put a regular monthly investment of S$200 into the Vanguard S&P 500 ETF (NYSEARCA: VOO), which historically has delivered an average annualised return of around 10.5%.

Look how the numbers shift:

- Start at 25: Your invested principal of S$72,000 grows to around S$503,280 by age 55.

- Start at 35: Your capital drops to S$48,000 and grows to just S$162,101 by 55.

- Double up at 35: Even doubling up your instalments to S$400 monthly only yields S$324,202 by 55 (with a principal of S$96,000).

Delaying your journey by a single decade deals a huge blow to your returns, forcing you to grind much harder later in life.

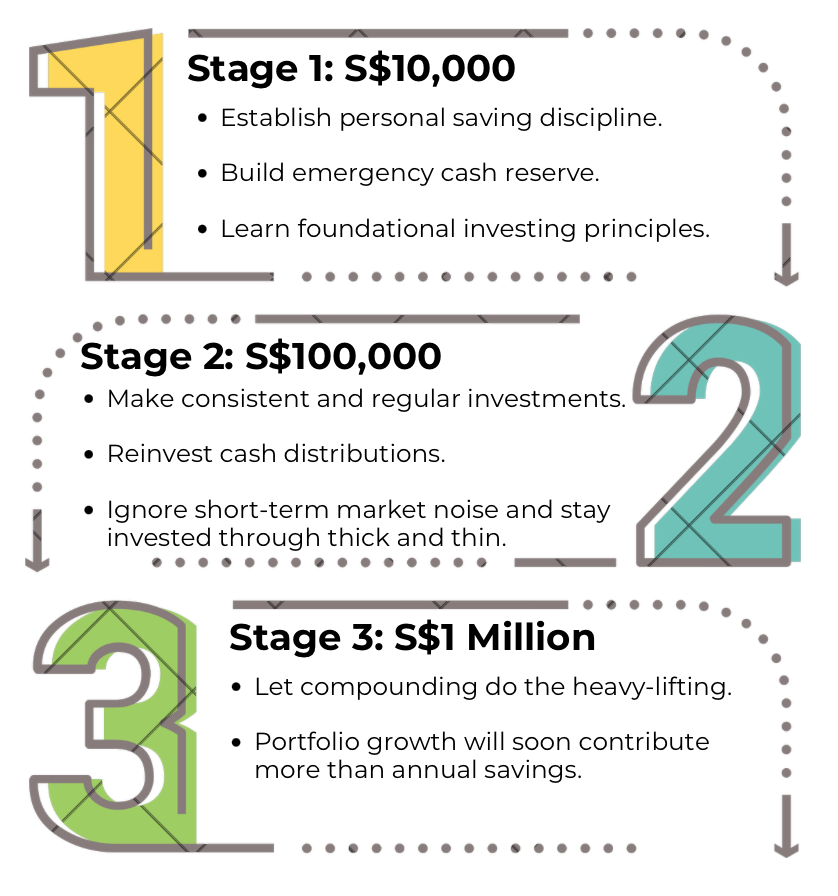

Building the Path from S$10k to S$1 Million

During the first stage, your core objective is to build personal saving discipline and an emergency fund.

Simultaneously, pick up core investing principles so you know how the market works before diving in.

Once your S$10,000 base is locked in, start making consistent and regular investments.

Utilise dollar-cost averaging (DCA) to manage your portfolio risk while buying into diversified, broad-market instruments like VOO.

Reinvest cash distributions right back into the market to accelerate growth.

Additionally, ignore short-term noise and stay invested through thick and thin.

The compounding process becomes highly significant once you cross the six-figure net worth, where your annual investment growth will eventually contribute far more to your wealth than your actual annual salary savings.

Three Habits That Matter More Than Stock Picks

#1: Paying yourself first

Allocate investment capital the day your paycheck hits rather than waiting till month-end to see what’s left.

Trust me when I say consistency beats trying to time the market.

#2: Increasing your investing rate

Rather than upgrading your lifestyle to match a pay raise, direct a larger portion of your promotion and year-end bonuses into your portfolio.

#3: Staying invested through market crashes

Market downturns are normal, so there’s no need to treat them like the end of the world.

Don’t panic-sell and lock in losses.

Instead, view dips as a discount sale to accumulate more shares.

What a “Millionaire by 40” Portfolio Might Look Like

Income-producing assets

Blue-chip players like DBS Group (SGX: D05) and CapitaLand Integrated Commercial Trust (SGX: CICT) provide reliable passive income through dividends.

Reinvest these payouts to accumulate more shares and speed up compounding.

Growth investments

Allocating a portion into broad-market equity ETFs – like VOO for global exposure and the SPDR STI ETF (SGX: ES3) for local coverage – provides instant market diversification.

Cash and flexibility

Keeping cash in Singapore T-Bills or high-yield savings accounts provides an emergency safety buffer and “dry powder” to buy during market dips.

Common Mistakes That Derail the Journey

While waiting on the sidelines for the “perfect” time to buy in, the market usually continues upward without you.

Speculative investments and get-rich-quick schemes mostly end in permanent capital destruction.

There are simply no shortcuts to building sustainable wealth because compounding is the ultimate investing tool.

Lastly, don’t treat early profits or dividends as spending cash.

Consuming payouts early kills that compounding snowball before it forms.

Get Smart: Your First S$10,000 Is More Powerful Than You Think

A massive seven-figure target can feel daunting, but breaking it down into smaller goals makes it completely manageable.

Forget the huge end number for now and focus entirely on your foundation – the first S$10,000.

Progress creates massive psychological momentum.

Once you hit that first milestone, it only gets easier from there.

Just stay consistent and patient, and your future self will definitely be rewarded.

What are the stock secrets to Singapore’s “quiet millionaires?” Chances are, you’ll find at least one of their favourites in this free report. Download it now and see how these stocks could power your portfolio!

Follow us on Facebook, Instagram and Telegram for the latest investing news and analyses!

Disclosure: Si-Fan T. owns shares in VOO, ES3, and DBS.