REITs have proven themselves as reliable dividend payers over the years.

Income-seeking investors have tapped into this asset class for consistent and dependable distributions since the very first REIT, CapitaMall Trust, was listed back in 2002.

Two decades on, Singapore is now well-known for being a REIT hub.

However, of late, the sector has come under pressure.

Share prices of popular REITs such as Mapletree Logistics Trust (SGX: M44U) and Frasers Centrepoint Trust (SGX: J69U) have hit their 52-week lows.

Several foreign REITs such as Cromwell European REIT (SGX: CWBU) are also hitting multi-year lows.

These declines are worrisome as they imply a loss of confidence in the REIT sector.

Should investors be worried?

Or could this be a golden opportunity to scoop up attractive bargains?

Reasons for the plunge

A key reason why REIT prices are plunging is because of a sharp increase in interest rates.

The US Federal Reserve has hiked its policy rate by 0.75 percentage points over three consecutive sessions, taking the benchmark rate to a range of between 3% to 3.25%.

As all REITs hold debt, an increase in interest rates will raise borrowing costs for them, thus crimping the amount of distributable income they can pay out.

The US central bank has made these moves in response to the highest inflation the country has seen in four decades.

The latest inflation reading in the US, at 8.2% for August, has done little to quell rumours that yet another large rate hike is on the cards.

If the Federal Reserve makes a similar move in early November, benchmark rates could hit 4%, a level unseen since the Great Financial Crisis in 2008.

For REITs, surging inflation will also increase operating expenses such as electricity, marketing and staff costs, resulting in less distributable income to dole out to unitholders.

The combination of the two – sky-high inflation and rising interest rates is causing significant concern among investors as to whether REITs can maintain their distribution per unit (DPU).

A third factor is also at play.

Investors who are looking for alternatives to park their money can now seek interest-free instruments such as Singapore Savings Bonds (SSBs) and fixed deposits.

The former is paying out a 10-year average return of 3.21% while the latter has seen rates hit as high as 2.6% to 2.7% for a 12-month and 24-month tenure.

Risk appetites are declining and this is evident as more people yank their money out of REITs and into “safe havens”.

DPU and asset values may decline

Some of these fears could be justified.

REITs will come under pressure and DPU may decline in the coming quarters.

In addition, REIT property values may also fall when the assets are up for revaluation.

Property values are usually computed by independent property agencies based on a capitalisation rate (cap rate).

The property’s net operating income (i.e. rental income minus expenses) is divided by this cap rate to obtain the property’s valuation.

With interest rates heading up, assuming a similar level of net operating income, the denominator will increase for this equation, thus resulting in lower property values.

As REIT gearing levels are predicated on its asset base, a decline in asset valuation will result in gearing levels increasing even without the REIT taking on additional loans.

Another factor to consider is exchange rates.

The Japanese Yen has weakened by close to 24% against the Singapore dollar (SGD) in the past year.

The British pound (£) has declined by 13% against the SGD over the same period.

Exchange movements have impacted REITs such as Daiwa House Logistics Trust (SGX: DHLU) and Elite Commercial REIT (SGX: MXNU).

With the need to convert their distributions to SGD even though their base rental income is in Yen or £, investors are seeing a possible DPU decline looming.

Mitigating factors

There are reasons to be optimistic, though.

REITs have several mitigating factors in place to buffer against these rising expenses.

Frasers Logistics & Commercial Trust (SGX: BUOU) has a very low gearing of just 29.2% as of 30 June 2022, thus mitigating against a rise in gearing due to declining property values.

Having a high proportion of fixed-rate debt and a well-spread-out debt maturity are also some measures that REITs possess to guard against sharply higher finance costs.

Furthermore, REITs with strong sponsors will also have a ready pipeline of assets to tap into for acquisitions to boost DPU and offset the effects of higher costs.

Get Smart: Watch and learn

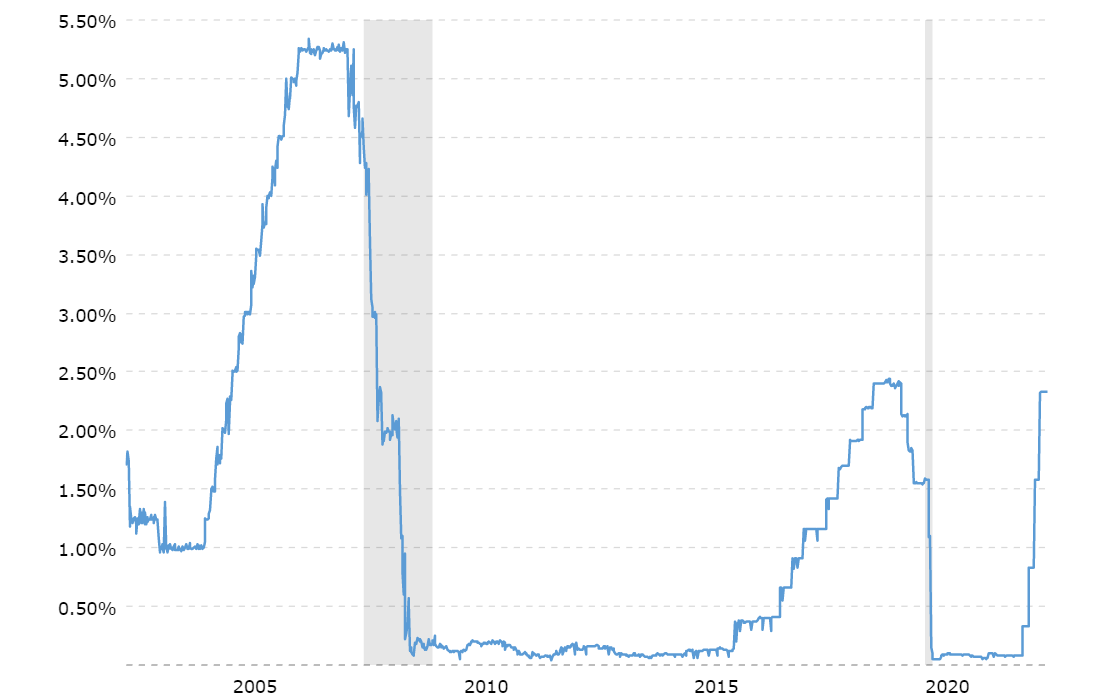

Source: Macrotrends

The world is seeing a new, high-interest-rate phase that has not been witnessed in nearly 14 years.

The chart above shows that rates have only gone past the 5% mark once in the last two decades.

It’s a whole new world for investors and also a different environment for REITs.

Investors should watch and learn and continue to monitor how REITs adjust to this new paradigm.

There’s cause for worry, but if you stick with the strong REITs, you can still enjoy a good night’s sleep.

Is it a good time to buy into Singapore REITs? If you’ve thought about it, then our latest REITs guide will be an essential read. This exclusive pdf report shows you why REITs are still excellent assets, what sectors to look out for and how to find good REITs today. The info inside can help you build a solid retirement portfolio. Click here to download it for FREE.

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclaimer: Royston Yang owns shares of Frasers Logistics & Commercial Trust.