OCBC Ltd (SGX: O39) made a move that surprised the investment community.

The bank has offered to purchase the remaining shares of Great Eastern Holdings (SGX: G07), or GEH, that it does not already own in a voluntary unconditional general offer.

This move came right after the lender announced a sparkling set of earnings for the first quarter of 2024 (1Q 2024) as higher interest rates buoyed its total income.

Will OCBC’s move benefit the bank’s earnings and help it to achieve better results? Let’s dig deeper to find out.

Details of the offer

OCBC intends to acquire the remaining 11.56% of GEH that it does not already own at an offer price of S$25.60 per share.

This offer price is a nearly 37% premium over GEH’s last traded price of S$18.70.

In total, OCBC will spend S$1.4 billion to buy up this remaining stake to delist the insurer from the Singapore Exchange.

The offer is also at a price-to-embedded value (EV) of 0.7 times and a price-to-earnings (P/E) multiple of 15.6 times, higher than the price to EV of 0.51 times and P/E of 11.4 times at GEH’s last traded price.

OCBC’s minority shareholders had brought up the issue of GEH’s persistent undervaluation and were also raising questions about the bank’s strategy.

Head of Investor Relations for OCBC, Collins Chin, highlighted that GEH remains a key pillar of OCBC’s insurance arm and this offer by the lender could be seen as a way to placate disgruntled minority shareholders.

A strong set of results for GEH

With this in mind, let’s take a peek at GEH’s financial results to determine if OCBC made a wise move.

In 2023, GEH saw its net profit climb 27% year on year to S$774.6 million.

The insurer declared a final dividend of S$0.40, taking its total 2023 dividend to S$0.75, up from S$0.65 a year ago.

For 1Q 2024, GEH saw total weighted new sales jump 34% year on year to S$524.2 million while new business embedded value rose 21% year on year to S$163.2 million.

The group’s net profit continued to rise, improving by 26% year on year to S$306.7 million.

A sprawling enterprise

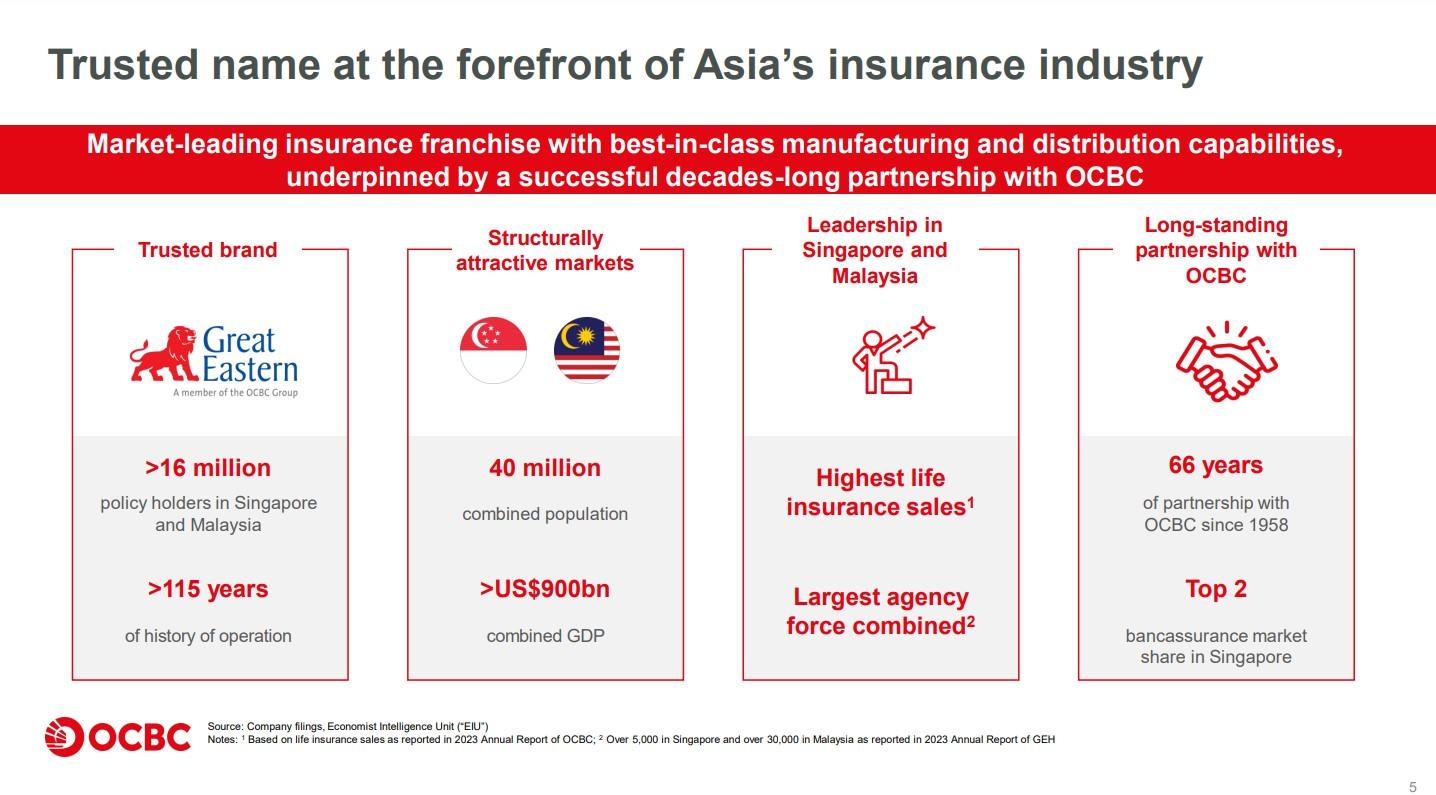

GEH is a big name in Asia’s insurance industry with more than 16 million policyholders across Singapore and Malaysia (see below).

Source: OCBC’s offer for Great Eastern – Presentation Slides

The insurer also has more than 115 years of operating history and is a storied name in the industry.

The markets that it targets (Singapore and Malaysia) have a total combined population of 40 million along with a gross domestic product of more than US$900 billion.

These attributes make GEH attractive as the insurer not only boasts a strong franchise but also enjoys structural tailwinds that will enable it to grow further.

Offer backed by solid reasons

OCBC also offered several reasons as to why it decided to buy up all the shares of GEH.

The first is to reinforce its strategic vision to become Asia’s leading wealth management player.

This move is in line with OCBC’s rebranded corporate strategy to strengthen its key pillars of banking, wealth management, and insurance.

With GEH being an established market leader for life insurance, OCBC shares a synergistic relationship with the insurer.

OCBC can tap GEH to offer a comprehensive suite of customised insurance solutions while GEH leverages OCBC’s extensive retail and commercial customer base.

Management also argues that this offer will enhance OCBC’s returns and help to optimise capital.

Assuming the offer goes through, it will be earnings accretive to OCBC as GEH has contributed an average of S$700 million in net profit annually to the bank over the past decade.

This level of profit equates to around 15% of OCBC’s total net profit for the period.

The offer will also raise OCBC’s 2023 return on equity (ROE) by 0.2 percentage points to hit 14% while its CET1 (Capital Adequacy) Ratio will fall to 15.3%.

Management also assures that OCBC’s capital position will remain strong following the offer even though the blue-chip bank will use solely internal cash to fund the offer.

Get Smart: A strong positive

The verdict is clear.

GEH is a powerhouse in the insurance industry and OCBC has laid out a strong rationale for purchasing and privatising the company.

The transaction will also add to OCBC’s earnings while boosting its ROE.

However, there is a chance that minority shareholders of GEH may clamour for a higher offer as the current tabled offer is at 0.7 times the insurer’s EV.

If so, OCBC could feel compelled to raise its offer price, thereby reducing some of the earnings and ROE accretion.

We’ve just released a new Special FREE Report: “How to Make Your Child a Millionaire.” It’s a simple, no-nonsense guide for parents who care for their child’s financial future. You’ll also find 3 stocks (one even had a 55.8% jump in dividends) you can consider today to kickstart your child’s “piggy bank.” Click HERE to download now.

Disclosure: Royston Yang does not own shares in any of the companies mentioned.