It’s always intriguing to see how much our money would have grown had we held on to strong businesses over a long period.

This exercise gives us an indication of a stock’s financial strength and consistency.

It can also tell us if a business can weather recessions and yet deliver.

Investors in Singapore Technologies Engineering Ltd (SGX: S63), or STE, may wonder if the blue-chip engineering giant has delivered a good return if held for more than a decade.

At the same time, we also assess if the group can continue to perform well based on its current prospects.

A dividend stalwart

STE went public 25 years ago in December 1997 and has been a component of the Straits Times Index (SGX: ^STI) ever since.

Temasek Holdings, a Singapore investment firm, holds a 51.69% stake in the engineering group as of 28 February this year.

Assuming you invested S$10,000 in STE back in July 2010, you would receive around 3,000 shares of the group.

The share price closed at S$4.10 recently, chalking up a 24% gain for the stock over 12 years.

This means that your original S$10,000 would have grown to S$12,400, giving you a S$2,400 capital gain.

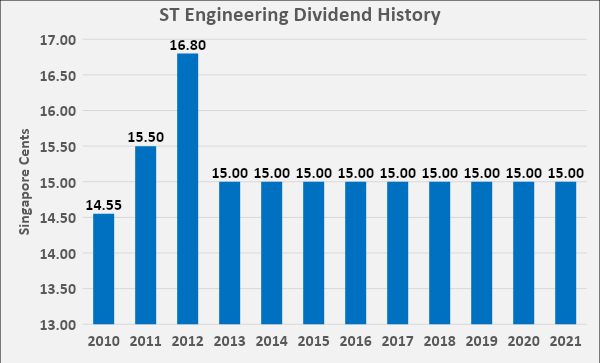

While this may not seem impressive, STE’s strength is in its consistent dividend payments over the years (see below).

Source: ST Engineering’s Annual Reports; Author’s Compilation

The group has paid out a consistent dividend over the last 12 years amounting to S$1.8185 per share.

Your 3,000 shares would have netted you a total of S$5,455.50 in dividends from 2010 to 2021.

Add this to the S$12,400, and your total will come up to S$17.855.50 for a 78.6% total return.

Over 12 years, this translates to a 4.9% compound annual growth rate, which beats the long-term inflation rate of around 2% to 3%.

From strength to strength

The question is, can STE deliver the same level of returns moving forward?

First off, let’s look at STE’s order book.

Its fiscal 2022’s first quarter (1Q2022) market update saw the group clinch a total of S$2.4 billion in new contracts across all three of its divisions.

As a result, the order book has ballooned to a three-year high of S$21.3 billion, higher than the pre-COVID level of S$15.3 billion.

Furthermore, STE had recently concluded the purchase of TransCore for US$2.7 billion to further its smart city ambitions.

TransCore is a market leader in electronic toll collection solutions (ETC) and a leading provider of intelligent transportation systems (ITS), and the purchase should help to boost STE’s top and bottom lines.

The cost of debt related to loans taken up to finance the TransCore purchase comes up to just 1.8%, ensuring that STE can earn a positive return on this investment.

Growing the digital business

STE is also aiming to drive growth in its digital business, which comprises cloud services, artificial intelligence (AI) analytics, and cybersecurity.

The group detailed its ambitions during its Investor Day in November last year.

These three sub-segments are poised to more than triple their combined revenue to more than S$500 million by 2026.

Upping its dividends

There’s more good news for investors.

STE’s board has approved an increase in the group’s annual dividend from S$0.15 per share to S$0.16, effective for FY2022.

What’s more, the dividend will now be paid quarterly at S$0.04 per quarter instead of half-yearly so that shareholders can receive a more frequent stream of passive income.

The increase in dividends shows management’s commitment to rewarding investors and signals its confidence in its future.

Get Smart: A reliable growth and dividend stock

Investors of STE would have collected a decent return from owning the stock for over 12 years.

However, there may still be room for the share price to run should the group’s revenue, order book and net profit continue to climb.

The blue-chip technology group will provide peace of mind and qualifies as a reliable dividend cum growth stock.

Looking for investment opportunities in 2022 and beyond? In our latest special FREE report “Top 9 Dividend Stocks for 2022”, we’re revealing 3 groups of stocks that are set to deliver mouth-watering dividends in the coming year.

Our safe-harbour stocks are a set of blue-chip companies that have been able to hold their own and deliver steady dividends. Growth accelerators stocks are enterprising businesses poised to continue their growth. And finally, the pandemic surprises are the unexpected winners of the pandemic.

Want to know more? Click HERE to download for free now!

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclaimer: Royston Yang does not own shares in any of the companies mentioned.