Earnings season is coming to a close, and it has offered good insights as to how companies fared last year.

Notably, our three local banks had also released their fiscal 2021 (FY2021) earnings.

DBS Group (SGX: D05), Singapore’s largest bank, was the first to report its FY2021 earnings.

Next came United Overseas Bank Ltd (SGX: U11), or UOB, with its impressive financial results.

The third and last lender to report was OCBC Ltd (SGX: O39), which released its FY2021 report card in late February.

With their financial and operating metrics fully disclosed, which bank should investors choose among the trio?

We place the three lenders side by side to determine which makes the most attractive investment idea.

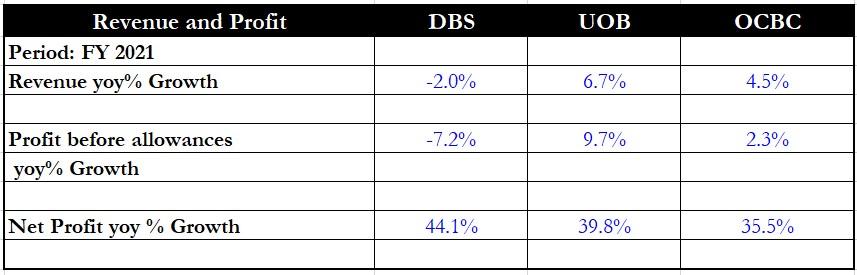

Financial performance

Source: DBS, UOB and OCBC’s earnings reports

We start with the banks’ financial performance.

DBS is the only one of the three banks that reported a slight year on year dip in total revenue.

The decline was mainly due to the fall in net interest margins (NIMs) that the bank experienced in FY2021.

Although DBS saw its net fee income rise 15% year on year, it was insufficient to cushion the fall in net interest income.

UOB is the standout performer here with year on year revenue growth of 6.7%.

UOB also performed the best among the three as operating profit before allowances rose 9.7% year on year.

Winner: UOB

Source: DBS, UOB and OCBC’s earnings reports

However, DBS announced a 44.1% year on year jump in net profit, higher than UOB’s 39.8% and OCBC’s 35.5%.

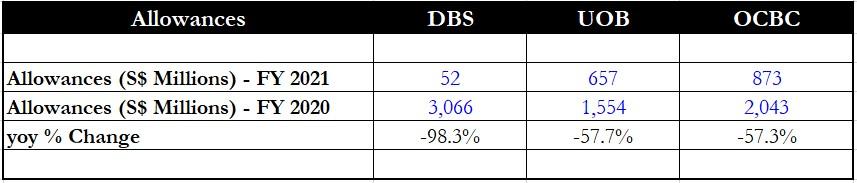

The reason can be traced to the level of allowances that each bank made in FY2021.

DBS saw its allowances plunge from S$3.1 billion a year ago to just S$52 million as the lender wrote back some provisions made in the past.

The other two banks also saw a decline in allowances as economic conditions improved, but the decline was around 57% year on year.

Winner: DBS

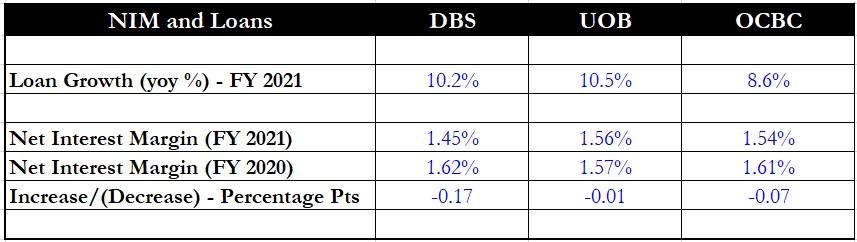

NIMs and loan growth

Source: DBS, UOB and OCBC’s earnings reports

Moving on NIMs and loan growth, both DBS and UOB reported healthy double-digit year on year loan growth.

OCBC came in third with high single-digit year on year loan growth, but it’s good news to see all three banks expanding their loan books in FY2021.

The picture for NIM was more varied, though.

DBS has reported the lowest NIM of the three for FY2021, and it also saw the biggest drop in NIMs from FY2020, at 0.17 percentage points.

UOB not only had the highest NIM among the three at 1.56% but also saw the smallest decline among the three.

Winner: UOB

Cost-to-income ratio

Source: DBS, UOB and OCBC’s earnings reports

Next, we move on to the cost-to-income ratio, which measures the expense level for each bank in relation to its total income.

UOB has the lowest cost-to-income ratio of the trio, at 44.1%, and its ratio had also come down from the 45.6% a year earlier.

However, investors should note that UOB may see higher expenses moving forward due to its upcoming purchase of Citigroup’s (NYSE: C) consumer banking business in four Asian countries.

Winner: UOB

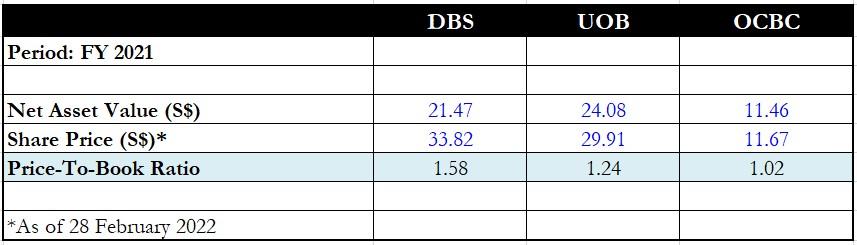

Valuation

Source: DBS, UOB and OCBC’s earnings reports

When it comes to valuation, DBS is, by far, the most expensive bank of the three as it is trading at a price to book (P/B) ratio of 1.58 times.

UOB comes in second with a P/B of 1.24 times while OCBC is the cheapest, trading at close to its net asset value.

Shares of DBS may have been bid up in anticipation of acquisitions that it had undertaken in FY2021.

Last year, DBS acquired a 13% stake in Shenzhen Rural Commercial Bank for around S$1.1 billion and this year, the group announced the purchase of Citigroup’s Taiwan division for S$2.2 billion.

DBS also collaborated with Singapore Exchange Limited (SGX: S68), Standard Chartered Bank and Temasek Holdings to launch Climate Impact X in May last year.

Climate Impact X is a global carbon exchange and marketplace for the trading of high-quality carbon credits, which are becoming increasingly important as highlighted during Singapore’s recent Budget 2022.

Winner: OCBC

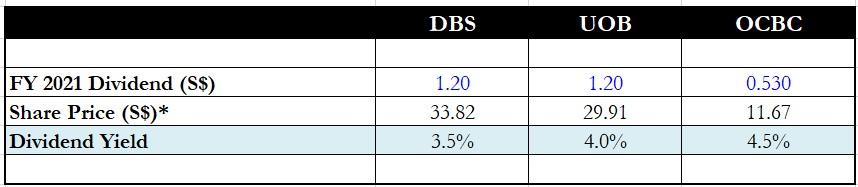

Dividend yield

Source: DBS, UOB and OCBC’s earnings reports

Income-seeking investors will be most interested in this last metric: each bank’s dividend yield.

OCBC has the highest dividend yield among the three banks, at 4.5%.

However, investors should note that DBS’ FY2021 dividend includes its first-quarter dividend of S$0.18 per share, which was lower than its following three quarters due to the Monetary Authority of Singapore’s dividend restrictions imposed in 2020.

Since then, DBS has raised its quarterly dividend to S$0.36 per share, implying an FY2022 full-year dividend of S$1.44.

At this level of dividends, the forward dividend yield should stand at 4.2%.

Winner: OCBC

Get Smart: A mix of growth and yield

UOB is the winner for this round as the lender provides a great mix of growth and yield.

It enjoyed healthy loan growth of around ~10% year on year while also keeping its NIM steady. Net profit also surged by close to 40% year on year.

UOB’s purchase of Citigroup’s consumer banking business should accelerate its goal of acquiring more customers in the four regions of Indonesia, Malaysia, Vietnam, and Thailand.

The bank’s shares also sport a trailing dividend yield of 4%, and there is a chance this dividend could increase should UOB continue to report growth in its top and bottom lines.

Is it a good time to buy into Singapore REITs? If you’ve thought about it, then our latest REITs guide will be an essential read. This exclusive pdf report shows you why REITs are still excellent assets, what sectors to look out for and how to find good REITs today. The info inside can help you build a solid retirement portfolio. Click here to download it for FREE.

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclaimer: Royston Yang owns shares of DBS Group and Singapore Exchange Limited.