After two turbulent years, the skies are finally clearing for Singapore Airlines Limited (SGX: C6L), or SIA.

In late March, the Singapore government had announced an easing of safe management measures, along with a slew of changes that further relaxed rules on travel, gatherings, and live performances.

This reopening should be music to the airline’s ears as it looks forward to better days ahead.

Importantly, Singapore is also shifting to a new Vaccinated Travel Framework (VTF) for all travellers.

The VTF simplifies the rules regarding travel, where countries are either classified in the “general travel” or “restricted” categories.

All fully-vaccinated travellers will be able to enter Singapore with just a pre-departure test from this month onwards.

They also will not need to quarantine and no longer need to take any COVID-19 tests here.

These changes should significantly increase the number of tourists entering Singapore, thereby boosting SIA’s prospects.

With a brighter outlook ahead, can Singapore’s flagship carrier see its dividend being restored?

Jump in passenger numbers

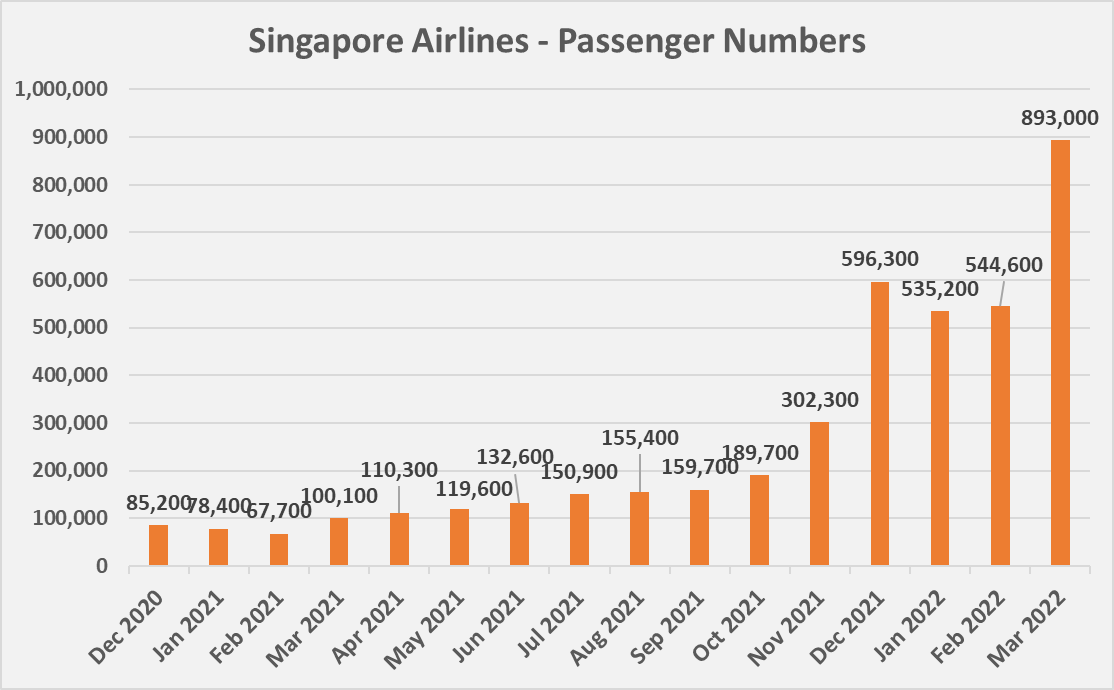

Since the vaccinated travel lane (VTL) scheme was launched in August last year, SIA has seen passenger numbers rise steadily.

Granted, passenger numbers had already been on an uptrend since early 2021 as several countries eased their border rules, but the VTL scheme resulted in an even stronger surge.

Source: Singapore Airlines Operating Statistics; Author’s Compilation

Passenger numbers rose from 85,200 in December 2020 to 132,600 in June 2021, a period of six months.

However, from September 2021 till March this year, this number went from 159,700 to 893,000, a more than five-fold increase.

And there are indications that this uptrend can continue with the introduction of the VTF.

Better financial numbers

There are also signs pointing towards better financial numbers for the group.

For its fiscal 2022’s (FY2022) third quarter ended 31 December 2021, SIA reported its first quarterly profit of S$85 million since the onset of the pandemic.

Group revenue also more than doubled year on year to S$2.3 billion for the quarter backed by the year-end holiday season and strong cargo demand.

The airline also generated an operating cash surplus of S$322 million for the first nine months of FY2022.

For context, in late-2020, SIA’s cash burn rate stood at S$4.2 billion a year, or around S$350,000 a month.

By May last year, this had been reduced to S$150,000 a month and by November, had further shrunk to just S$18 million per month.

These encouraging numbers demonstrate SIA’s commitment to reduce costs and help to make its business leaner, thus preparing it for the economic recovery.

Catalysts for growth

Several catalysts have also emerged for the airline that should enable it to do well over time.

First off, its cargo division is seeing robust demand, with loads comfortably exceeding pre-COVID levels for the past three quarters of FY2022.

The number of cargo destinations has also more than tripled since April 2020 from 26 to 97.

SIA also inked a crew and maintenance agreement with logistics company DHL Express to latch on to the fast-growing e-commerce segment.

Meanwhile, the carrier also signed a letter of intent to purchase seven A350F freighter aircraft with an option to buy five more.

When delivered in 2025, it will make SIA the first airline to operate this new-generation wide-bodied aircraft.

Not only will this move help in the group’s fleet renewal process, but it also demonstrates SIA’s commitment to ensuring its fleet remains one of the youngest in the industry.

Get Smart: Green shoots, but patience is needed

The last time SIA paid out a dividend was back in November 2019 when it declared an interim dividend of S$0.08 for the first half of FY2020.

By the end of FY2020, the pandemic had resulted in SIA reporting a full-year loss of S$212 million, leading it to suspend its final dividend to conserve cash.

While the signs are positive, I believe that several factors need to be in place before the airline can resume its dividend payments.

First, passenger numbers need to rise closer to pre-COVID levels so that the airline can enjoy a material boost in its financial numbers.

As a comparison, passenger numbers back in January 2020 stood at close to 3.4 million.

Next, SIA needs to report significantly higher operating cash flow and consistent net profit.

These will take time as tourism volumes ramp up, so investors need more patience as it is unlikely that the airline will start doling out dividends for FY2022.

Looking for investment opportunities in 2022 and beyond? In our latest special FREE report “Top 9 Dividend Stocks for 2022”, we’re revealing 3 groups of stocks that are set to deliver mouth-watering dividends in the coming year.

Our safe-harbour stocks are a set of blue-chip companies that have been able to hold their own and deliver steady dividends. Growth accelerators stocks are enterprising businesses poised to continue their growth. And finally, the pandemic surprises are the unexpected winners of the pandemic.

Want to know more? Click HERE to download for free now!

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclaimer: Royston Yang does not own shares in any of the companies mentioned.