Singapore is well-known for being a REIT hub.

With a plethora of choices, it can be tough to nail down a promising REIT that has both a high distribution yield and good growth prospects.

We took the liberty of comparing two popular REITs, Mapletree Logistics Trust (SGX: M44U), or MLT, and Mapletree Pan Asia Commercial Trust (SGX: N2IU), or MPACT, to see which is the more attractive option.

Both REITs have a common sponsor, Mapletree Investments Pte Ltd, a real estate development and investment group that owns and manages S$78.7 billion of properties as of 31 March 2022 in various sub-sectors.

Let’s review various aspects of MLT and MPACT to determine which is a better buy.

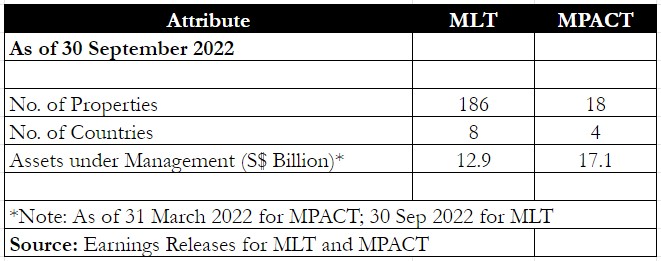

Portfolio composition

First, we review each REIT’s portfolio to determine how diversified it is.

A well-diversified portfolio is a boon as it helps to cushion the REIT against headwinds in any particular region or property.

From the table above, MLT owns more than 10 times the number of properties compared with MPACT, at 186 versus 18.

The logistics REIT is also present in a total of eight countries versus just five for MPACT.

However, MPACT is the slightly larger REIT with assets under management (AUM) of S$17.1 billion.

It’s also worth noting that MLT’s properties comprise logistics assets that should see continued strong demand as e-commerce booms in light of the pandemic.

MPACT’s properties are mainly commercial ones except for its VivoCity and Festival Walk retail properties.

Retail properties are more sensitive to economic conditions such as inflation rates that may dampen consumer demand.

Commercial properties may also face a fall in occupancy as hybrid work gains popularity in many parts of the world.

Winner: MLT

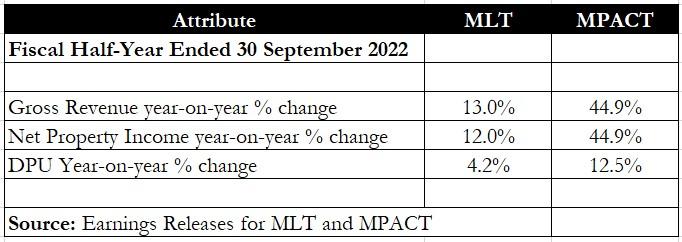

Financials and DPU

The next aspect is financial performance and each REIT’s distribution per unit (DPU).

MPACT’s numbers are significantly better than MLT’s as it reported a near-45% year on year jump in both gross revenue and net property income (NPI).

However, better performance should be viewed in light of MPACT’s recent merger.

Because of the addition of Mapletree North Asia Commercial Trust’s (MNACT) revenue and NPI to Mapletree Commercial Trust, MPACT thus reported sharply higher numbers.

DPU for MPACT rose 12.5% year on year due to the contributions from MNACT.

MLT did, however, eke out a decent 4.2% year on year rise in DPU.

Winner: MPACT

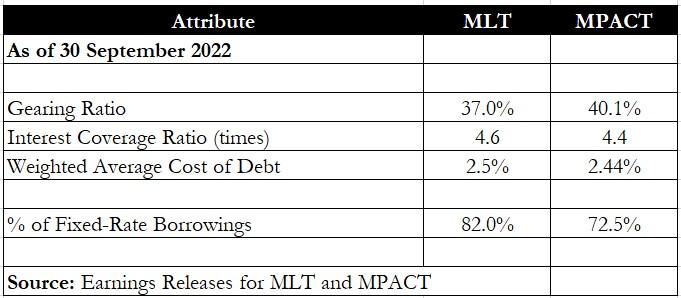

Debt metrics

Moving on to debt metrics, the table above shows that MLT sports a lower gearing ratio, at 37%, compared to MPACT’s 40.1%.

Lower aggregate leverage implies that a REIT has more debt headroom to take on yield-accretive acquisitions to boost its DPU.

Both REITs have a roughly similar cost of debt at around 2.5% but MLT has a slightly higher interest cover ratio at 4.6 times.

MLT also has one up over MPACT with 82% of its loans on fixed rates, higher than MPACT’s 72.5%.

Winner: MLT

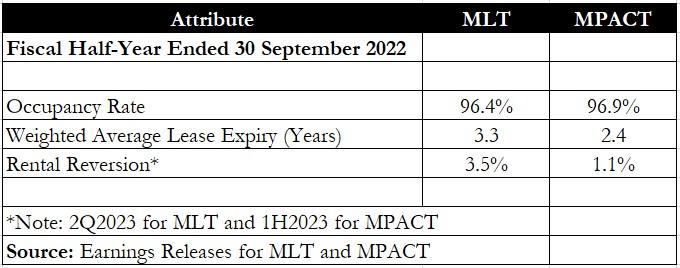

Operating metrics

Both MLT and MPACT sport a very high portfolio occupancy rate exceeding 96%.

However, MLT has a longer weighted average lease expiry (WALE) of 3.3 years as its leases are mostly industrial ones that are longer.

MPACT’s retail WALE stood at 2.1 years while its commercial segment’s WALE was 2.7 years.

Moreover, MLT also sported a higher rental reversion of 3.5% versus MPACT’s 1.1%.

MPACT’s lower rental reversion was mainly due to a negative 11.5% reversion for its key Hong Kong asset, Festival Walk.

Winner: MLT

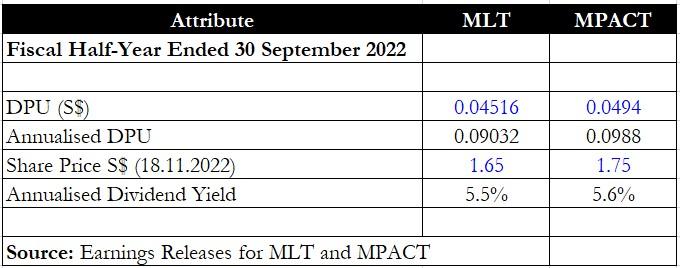

Distribution yield

Finally, we come to arguably the most important aspect of a REIT – its distribution yield.

Both MLT and MPACT are neck and neck, reporting an annualised distribution yield that is too close for comfort.

To differentiate the two, we turn to MLT’s successful acquisition track record.

The logistics REIT announced an acquisition and a redevelopment project for its fiscal 2023’s first half.

In the prior fiscal year, MLT also concluded a total of seven acquisitions.

MPACT is a newly-merged REIT that has yet to display its acquisition capability.

Hence, MLT clinches the title here as the REIT where investors can feel more confident in DPU rising over time.

Winner: MLT

Get Smart: Diversification is a boon

MLT is the winner this time as its diversified portfolio of properties enabled it to report a higher year on year DPU while buffering against headwinds in countries such as Hong Kong and China.

MPACT’s Festival Walk in Hong Kong was adversely affected by China’s COVID-zero policy, thereby affecting some of its operating numbers.

Investors should view MLT’s diversification as a boon but can also expect MPACT’s challenges to ease as China slowly relaxes its strict COVID-zero policy.

Not sure where to park your money in 2023? Give dividend stocks a try. You don’t need a lot of capital to start a stream of passive income. Our latest guide will show you how to invest and where to find the juicy dividends in SGX. Click here to download the report for FREE.

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclaimer: Royston Yang does not own shares in any of the companies mentioned.