With the wide variety of REITs available in the stock market, it can be tough to choose a suitable one.

The job is made even tougher when comparing two similar REITs that have the same sponsor.

A good example is Mapletree Logistics Trust (SGX: M44U), or MLT, and Mapletree Industrial Trust (SGX: ME8U), or MIT.

Both MLT and MIT are industrial REITs, albeit with different focuses, and both have a strong sponsor in Mapletree Investments Pte Ltd.

We decided to compare both REITs to determine which makes the better investment for income-seeking investors.

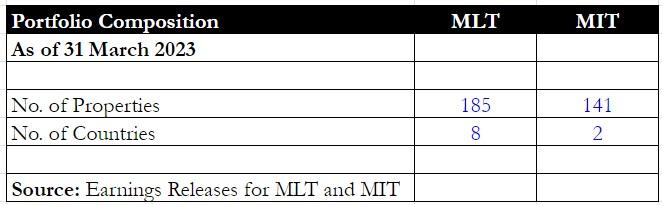

Portfolio composition

Both REITs have an impressive portfolio of properties with MLT’s coming in at 185 and MIT at 141.

MLT’s properties are logistics-related while MIT’s portfolio contains a healthy mix of industrial sub-types such as light industrial buildings, flatted factories, business parks, and hi-tech buildings.

Although MIT’s portfolio is spread out across six different segments, the properties are all concentrated in just two countries – Singapore and the US.

MLT, on the other hand, has the bulk of its properties in Singapore and China/Hong Kong with the rest spread out across six other countries such as Australia, South Korea, Malaysia, and Vietnam.

Hence, MLT’s portfolio is much more diversified in terms of geographic risks.

Winner: MLT

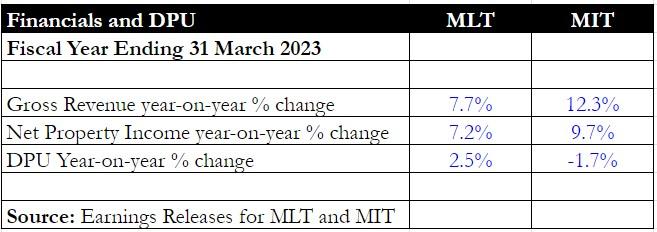

Financials and DPU

In terms of financials, MIT saw a higher rise in year-on-year gross revenue of 12.3% compared with MLT’s 7.7%.

Net property income, or NPI, also rose 9.7% year on year for MIT compared with 7.2% year on year for MLT.

MIT saw higher operating and borrowing costs that impacted its NPI for the fiscal year 2023 (FY2023).

The REIT also saw its number of units in issue inch up 2.4% year on year to 2.74 billion because of the distribution reinvestment plan.

In contrast, MLT’s issued units only crept up 0.7% year on year to 4.82 billion.

Hence, MLT managed to eke out a small 2.5% year-on-year increase in DPU but MIT saw its DPU slip by 1.7% year on year.

Winner: MLT

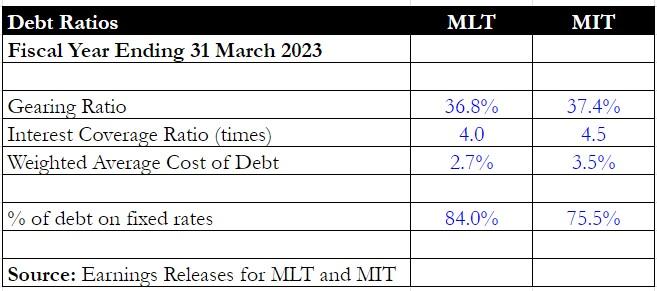

Debt metrics

Moving on to the REITs’ debt metrics, MLT has a slightly lower gearing ratio of 36.8% compared to MIT’s 37.4%.

However, the logistics REIT’s interest cover ratio (ICR) came in at four times, lower than MIT’s 4.5 times.

MLT’s cost of debt is also significantly lower than that of MIT, at 2.7% versus 3.5%, which may explain why the former’s NPI was not so much impacted by higher finance costs.

Moreover, MLT also has 84% of its debt tied to fixed rates, thereby mitigating a sharp increase in borrowing costs.

For MIT, this proportion is at just 75.5%.

Winner: MLT

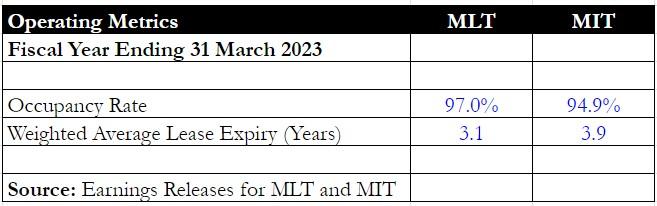

Operating metrics

Looking at operating metrics, MLT enjoys a higher occupancy rate of 97% when compared with MIT’s 94.9%.

However, as MIT has data centres within its portfolio, it enjoys a better WALE of 3.9 years compared with MLT’s 3.1 years.

Winner: MLT

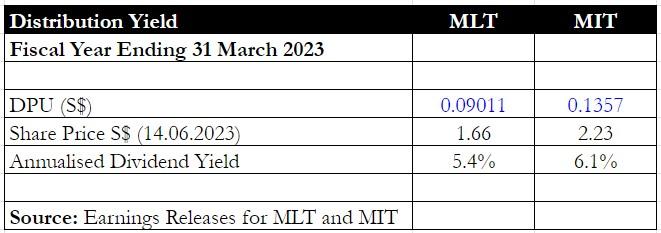

Distribution yield

Finally, we review both REITs’ distribution yields.

MIT has a much better distribution yield of 6.1% compared to MLT’s 5.4%.

This could boil down to the latter’s more robust debt and operating metrics that have seen MLT’s unit price stay more resilient.

Winner: MIT

Get Smart: MLT is the clear winner, but….

MLT is the clear winner here as it ticks off four out of the five categories.

However, income-driven investors may feel that distribution yield is the most important attribute for a REIT and thus place greater weight on MIT’s higher yield.

There are also other factors to watch for.

MIT had just completed its redevelopment of Mapletree Hi-Tech Park @ Kallang and the income from the committed leases will flow through in FY2024.

The industrial REIT had also recently concluded its first acquisition in two years by purchasing a Japanese data centre in Osaka.

MLT has also concluded a significant purchase of eight properties that should see its DPU rise by 2.2% but will lift its aggregate leverage to 39.9%.

Also, in terms of debt maturity, MLT has 19% of its total debt coming due in FY2024 and FY2025.

MIT, on the other hand, only has 10.5% of its debts coming due over the same period.

Hence, investors could see MLT’s cost of debt creep up more as it needs to refinance its loans using current high interest rates.

Investors will need to weigh these additional pieces of information to come to their final decision as to which REIT is more attractive.

Did you know there are 5 REIT sectors with a high potential for creating passive income? If you are building retirement wealth, this is crucial information. We have a new report that details all you need to know about them. Find out which sector to pay attention to, and see if you can fit them into your portfolio. Click HERE to download the guide here for free.

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclosure: Royston Yang owns shares of Mapletree Industrial Trust.