Industrial REITs have proven themselves to be resilient amid last year’s circuit breaker.

The ability of a REIT to stand firm amid strong headwinds depends largely on the tenants within their portfolio.

If you’re looking for a steady and dependable source of dividends, industrial REITs could be a good place to look.

As you narrow down your choices, deciding on one REIT over another requires some thought.

Especially when two REITs share many positive attributes such as a strong sponsor, high-quality assets, and a growing distribution per unit (DPU).

Take Keppel DC REIT (SGX: AJBU) and Mapletree Industrial Trust (SGX: ME8U), or MIT, for instance.

Keppel DC REIT is a data centre REIT that owns a portfolio of 19 data centres spread across eight countries.

MIT owns 87 industrial properties in Singapore and 28 properties in the US for a total of 115 properties worth around S$6.8 billion.

Between the two, which one would be a better buy? Let’s kick the tires on both REITs.

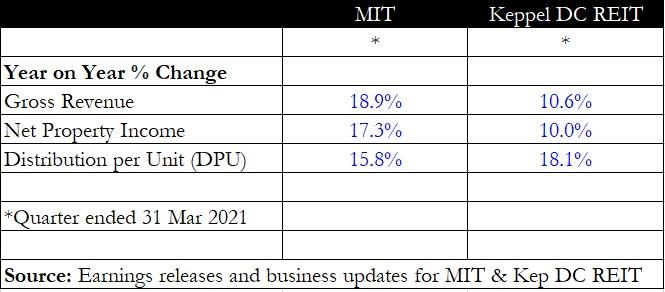

Revenue, NPI and DPU growth

Comparing the latest quarter’s results for both REITs, it’s clear that MIT has chalked up a stronger year on year performance.

Gross revenue increased by 18.9% year on year while net property income (NPI) increased by 17.3% year on year.

In contrast, Keppel DC REIT’s gross revenue and NPI has increased by 10.6% and 10% year on year, respectively.

However, when it comes to DPU, Keppel DC REIT is the winner with an 18.1% year on year jump compared to MIT’s 15.8% rise.

I would argue that DPU is the most important attribute that income-seeking investors are looking for.

Hence, Keppel DC REIT wins the first round as it registered a slightly higher year on year DPU increase.

Winner: Keppel DC REIT

Gearing and cost of debt

Next, we take a look at the gearing level for both REITs.

Lower aggregate leverage allows the REIT to take on more debt to carry out yield-accretive acquisitions.

Keppel DC REIT has the advantage here as its gearing stands at 37.2%, lower than MIT’s 40.3%.

To sweeten the deal, Keppel DC REIT also has a lower cost of debt at 1.5%, nearly half of what MIT is paying.

Having a lower cost of debt means the REIT will spend less cash on servicing the interest on its debt, enabling it to pay out more of its cash as DPU.

Finally, we also looked at the interest coverage ratio (ICR) for both REITs, which measures the operating profit divided by the REIT’s interest expense.

Keppel DC REIT has more than double the ICR of MIT, putting it in a stronger position to service its debt.

Winner: Keppel DC REIT

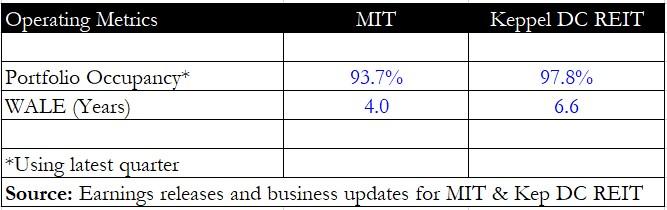

Operational aspects

Operating metrics include portfolio occupancy and the weighted average lease expiry (WALE) for both REITs.

A higher occupancy rate implies that more of the REIT’s gross floor area is being rented out, thus maximising rental income for unitholders.

On the other hand, WALE measures the average length of the leases extended by the REIT to its tenants.

A longer WALE is an advantage as it provides more certainty of rental income before the REIT manager is required to negotiate with tenants on lease renewal.

On both counts, Keppel DC REIT has the better numbers, with occupancy rate at 97.8% and WALE at 6.6 years.

Winner: Keppel DC REIT

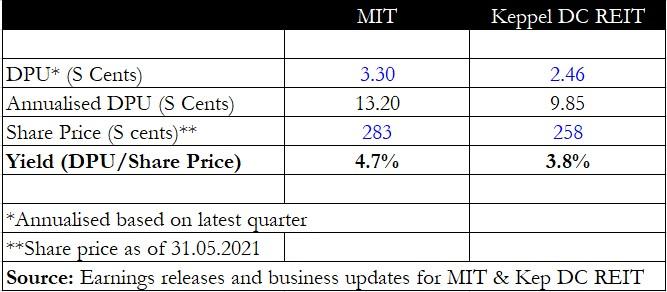

Dividend yield

Finally, we have a look at the distribution yield for each REIT.

Note that the DPU used is from the latest quarter and then annualised to obtain the full-year DPU.

Based on this calculation, MIT has the higher forward yield at 4.7% versus Keppel DC REIT at just 3.8%.

Moreover, this computation does not account for MIT’s recent acquisition of 29 data centres across 18 states in the US.

According to its presentation slides, DPU is expected to increase by 3.3% for the fiscal year 2021.

If we add this additional DPU boost to the projected DPU of S$0.132, we obtain an estimated DPU of S$0.1364.

MIT’s prospective dividend yield will thus inch up to 4.8%.

Winner: MIT

Get Smart: Other factors to consider too

From this initial analysis, it appears that Keppel DC REIT has “won” three out of four attributes, making it the better buy.

However, investors should also consider other factors apart from those listed above.

For one, MIT’s portfolio is significantly more diversified as it owns more than 100 properties, while Keppel DC REIT has just 19 data centres.

Furthermore, MIT’s portfolio is diversified across six property segments, of which data centres will take up 53.6% after the acquisition is completed.

Keppel DC REIT’s portfolio is concentrated on just one niche sector — data centres, making it vulnerable to adverse developments within this single asset class.

Investors need to balance out these qualitative factors as well when arriving at a final investment decision.

Looking for investment opportunities in 2022 and beyond? In our latest special FREE report “Top 9 Dividend Stocks for 2022”, we’re revealing 3 groups of stocks that are set to deliver mouth-watering dividends in the coming year.

Our safe-harbour stocks are a set of blue-chip companies that have been able to hold their own and deliver steady dividends. Growth accelerators stocks are enterprising businesses poised to continue their growth. And finally, the pandemic surprises are the unexpected winners of the pandemic.

Want to know more? Click HERE to download for free now!

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclaimer: Royston Yang owns shares of Keppel DC REIT.