We are right smack in the middle of the earnings season and the REIT sector is usually the first to announce its latest earnings and business updates.

It’s no secret that this asset class has been buffeted by the twin headwinds of high inflation and surging interest rates.

However, REITs with strong sponsors and a portfolio of high-quality assets are better positioned to weather this storm.

Two such REITs stand out – Mapletree Logistics Trust (SGX: M44U), or MLT, and Mapletree Industrial Trust (SGX: ME8U), or MIT.

Both are anchored by a strong sponsor in Mapletree Investments Pte Ltd.

Investors may be curious to know which REIT make the more attractive investment choice, so we put them side by side to compare various metrics.

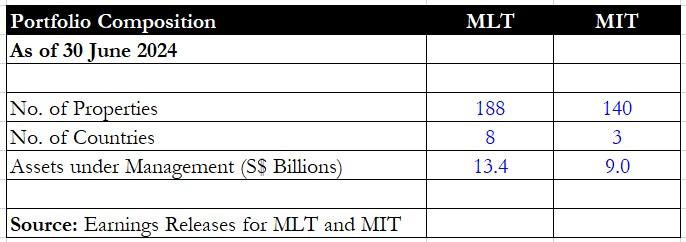

Portfolio composition

We start by looking at each REIT’s portfolio.

MLT and MIT both have more than 100 properties within their portfolios, which helps to diversify their rental income exposure.

MLT’s top tenant contributed just 4% to gross revenue while MIT’s largest tenant made up 5.9% of gross rental income.

However, in terms of geographic exposure, MLT’s properties are spread out across eight countries while MIT is focused on just three (Singapore, Japan, and the US).

MLT also has a larger asset under management (AUM) compared with MIT.

Winner: MLT

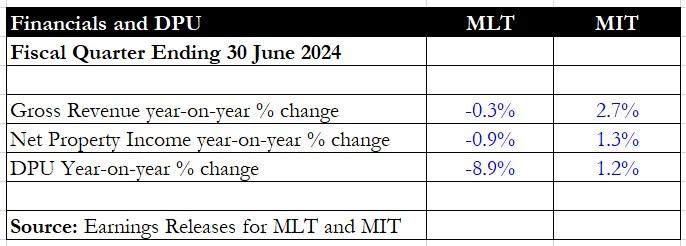

Financials and DPU

Moving on to each REIT’s financials, MIT reported a steadier performance for the first quarter of fiscal 2025 (1Q FY2025) ending 30 June 2024 compared with MLT.

Gross revenue for MIT rose year on year because of contributions from its newly-acquired Japan data centre along with new leases and renewals across various property clusters.

The industrial REIT saw its distribution per unit (DPU) inch up 1.2% year on year to S$0.0343 also because of a higher distribution declared by its joint venture, Mapletree Rosewood Data Centre Trust.

For MLT, its gross revenue was negatively impacted by the weakness of both the Chinese Yuan and Japanese Yen.

On a constant currency basis, MLT’s gross revenue and net property income would have increased by 2.1% and 1.3% year on year, respectively.

In addition, MLT was also adversely impacted by higher borrowing costs that rose 9.4% year on year.

In contrast, MIT saw its finance costs dip by 0.9% year on year for 1Q FY2025.

As a result, MLT’s DPU saw an 8.9% year-on-year tumble while MIT’s DPU managed to eke out a small 1.2% year-on-year gain.

Winner: MIT

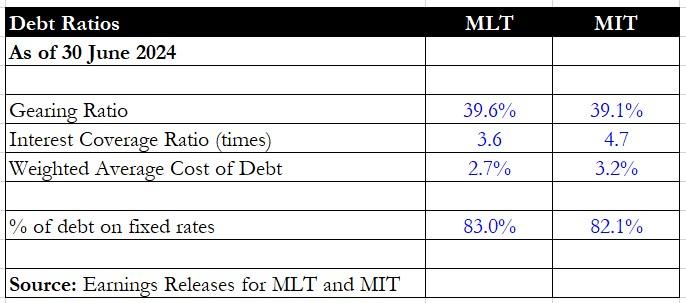

Debt metrics

Next, we look at each REIT’s debt metrics.

Both MIT and MLT had similar gearing ratios of 39%+.

MIT, however, sported a higher interest coverage ratio of 4.7 times compared with MLT’s 3.6 times.

On the flip side, MLT’s cost of debt, at 2.7%, was lower than MIT’s 3.2%.

Both REITs had around 82% to 83% of their debt pegged to fixed rates, thus helping to mitigate a sharp rise in finance costs.

We view a lower cost of debt as the more important metric here, so MLT wins in this case.

Investors should note that MLT’s manager warned that higher borrowing costs will continue to exert pressure on the REIT’s performance for FY2025.

Winner: MLT

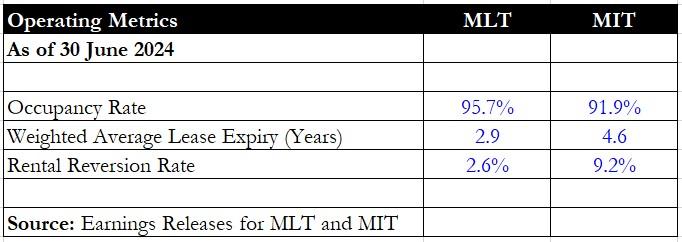

Operating metrics

Looking at operating metrics, MIT and MLT have widely differing statistics.

MLT boasts a higher overall portfolio occupancy rate compared with MIT, at 95.7% versus 91.9%.

However, MIT balances this out with a higher WALE (weighted average lease expiry) along with a stronger positive reversion rate of 9.2%.

MLT’s rental reversion rate saw a drag from China, where rental reversions hit -11.3% for 1Q FY2025, slightly worse than the previous quarter’s -10%.

Winner: MIT

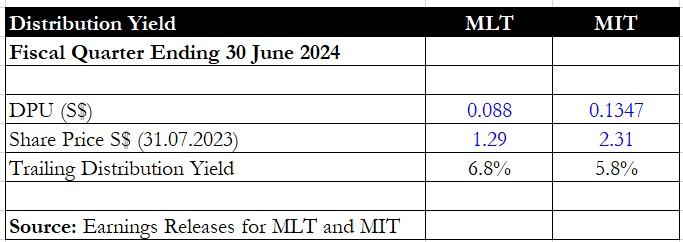

Distribution yield

Finally, investors should be interested in each REIT’s distribution yield.

MLT’s distribution yield of 6.8% is a full percentage point higher than MIT’s 5.8%.

However, investors should note that MLT’s manager has warned of continued currency headwinds and that China’s negative rental reversions should persist.

These factors will act as headwinds for the REIT and negatively impact both revenue and distributable income in the quarters ahead.

Winner: MLT

Get Smart: A tough decision

Let’s cut to the chase – it is a very tough decision to choose between both REITs.

Each has its strong attributes and you need to look at what you feel comfortable with as you go about choosing one for your portfolio.

We tend to go with MIT this round as the REIT does not have currency headwinds and China troubles that are dragging its performance.

Investors should also consider MLT’s active capital recycling programme in arriving at their final decision.

The logistics REIT announced three accretive acquisitions in 1Q FY2025 along with four divestments, all of which were done at a premium to the properties’ book values.

If undecided, you can always choose to own a little of each REIT for their respective strengths.

Which SGX companies will reach S$100 billion next? Our latest FREE report provides detailed financial analysis and growth prospects of 5 potential candidates. The results? Surprising. You’ll want to grab a copy now and see whether what everyone else says is true. Click here to download now.

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclosure: Royston Yang owns shares of Mapletree Industrial Trust.