Graduation marks the true day one of financial independence.

The feeling of receiving your first real paycheck is unmatched because you finally have spending power.

However, new responsibilities come with that excitement.

Suddenly, you need to navigate the Central Provident Fund (CPF), insurance, and adulting expenses.

Many would want to kickstart their investment journey too, but face a common problem: Where do I start?

Here’s a 3-year roadmap to help you work toward your first S$50,000.

Why the First S$50,000 Matters So Much

Starting from zero is a very slow process because your portfolio grows entirely on how much cash you save.

But hitting S$50,000 is a major financial tipping point.

It creates the initial momentum needed for long-term compounding to become visible, and also changes your relationship with money.

You stop looking at money as something to save in a bank, and see it as stepping stones to achieving financial freedom.

Year 1: Build Financial Stability and Investing Habits

Step one is to build a strong financial foundation.

Have three to six months of expenses parked in high-yield savings accounts or short-term Treasury-Bills (T-Bills).

This will be your financial shield so you never have to sell your investments if life gives you lemons.

Understandably, you’ll want to upgrade your lifestyle, but try to resist the urge to splurge on luxury habits.

Keeping your expenses grounded now sets you up for massive success later.

You don’t need a lot of money to start.

Consistently investing small amounts now is far better than dumping a lump sum ten years down the road.

Your defining metric at this stage is savings rate, the percentage of your monthly income kept after living expenses.

To keep things simple, look into Exchange Traded Funds (ETFs) like the SPDR Straits Times Index ETF (SGX: ES3) to get instant exposure to different segments of the economy.

Pair this with high-quality blue chips to provide a rock-solid foundation of reliable passive income.

Your main priority is to grow your portfolio size and cultivate healthy investing habits.

Financial goals should also be guided by realistic, long-term expected returns – say, 7% – rather than speculative overnight gains.

Year 2: Increase Contributions and Build Momentum

By your second year, you would have settled into your career and might even see a bump in salary and bonuses.

When your paycheck gets an upgrade, the portion allocated to your investments should adjust along with it.

Start expanding your portfolio to balance growth and income.

Consider local favourites like DBS Group Holdings (SGX: D05) and CapitaLand Integrated Commercial Trust (SGX: C38U).

They provide exposure to key industries and pump dividends directly into your account.

Avoid putting all your eggs in one basket.

Add international ETFs like the Vanguard S&P 500 ETF (NYSEARCA: VOO) to capture global growth.

But don’t just keep buying randomly.

Allocate specific percentages to each asset class.

Year 3: Let Compounding Start Working

Now, your portfolio is no longer a baby.

Here’s a tip: don’t spend the dividends you receive.

Use those payouts to buy back into the stock to kick off a snowball effect, which would then offer an even larger payout the next round.

To see this play out in numbers, track the dividend income growth.

This is also the perfect time to shift your mindset and remind yourself that short-term market noise doesn’t matter.

As long as you focus on high-quality assets, you are in good hands.

At the end of the three years, review your total portfolio value progress – the trend of your capital.

Check your savings rate, overall portfolio growth rate, and use those numbers to plan your next milestone.

The Power of Consistency Over Income Level

A common misconception is that you need a sky-high salary to build serious wealth.

That’s not true.

Trust me when I say that consistently investing small amounts monthly works better than chasing that perfect stock or waiting for a market dip.

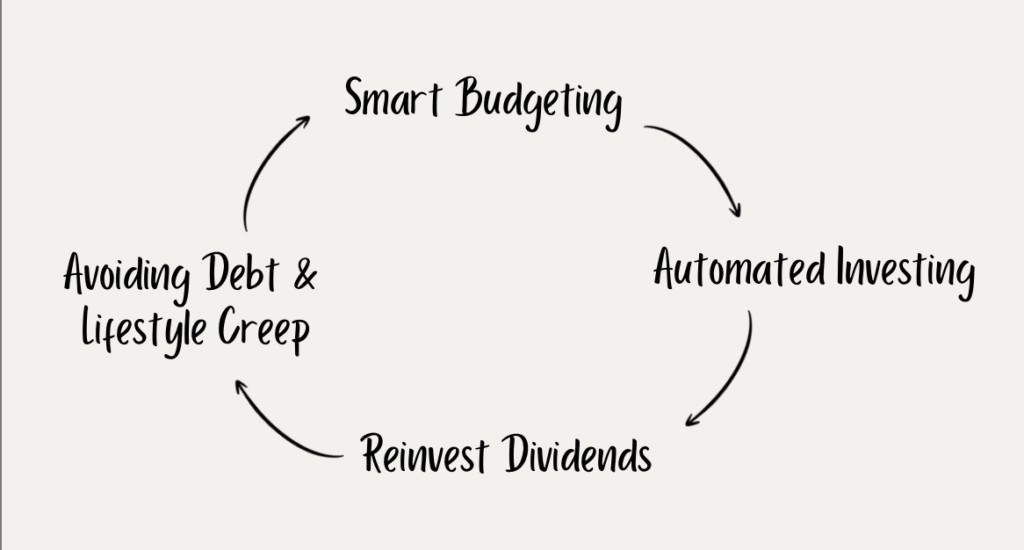

Sample Wealth-Building Framework

Here’s a wealth loop you can follow:

- Smart Budgeting: Allocate specific percentages of your salary to different spending categories. Investing should not be treated as an afterthought taken from whatever remaining cash.

- Automate Investing: Set up automatic, monthly recurring investments so you don’t have to log into your brokerage account to manually buy shares.

- Reinvest Dividends: Use payouts to buy more shares so that the compounding snowball never stops rolling.

- Avoid Debt and Lifestyle Creep: Celebrate your salary jumps, but also increase your investment allocation accordingly and avoid high-interest consumer debt.

Common Mistakes Young Investors Make

Sitting on the sidelines in hopes of a market crash is a losing game.

While waiting, you waste your biggest asset: time.

However, there are some things you shouldn’t waste time on, like those get-rich-quick schemes or viral meme coins you see online.

They are usually too good to be true.

Always pick quality over hype.

As mentioned earlier, salary bumps are a way to scale up your investments.

Treat yourself every now and then, but just keep your investment high up on the priority list.

Another golden rule: don’t buy things you can’t fully pay for in cash unless they are an absolute necessity.

Unnecessary consumer debt is a silent killer of wealth.

What Happens After the First S$50k?

Once you hit S$50,000, your dividend income begins to accelerate significantly.

The next tipping point occurs when organic market growth and dividend payouts outpace your monthly salary contributions.

And that’s when you tweak your allocations to maximise efficiency.

Get Smart: Max Out Your Time Horizon

You don’t need a massive salary to achieve S$50,000 as long as you remain consistent and disciplined.

Financial habits you forge in your first few working years will shape your wealth trajectory for years to come.

True investing success comes from making steady, unsexy progress, repeatedly, while time is still your greatest financial ally.

We’ve found 5 SGX-listed dividend stocks with strong track records in turbulent markets. If you want consistency in an uncertain world, start here.

Follow us on Facebook, Instagram and Telegram for the latest investing news and analyses!

Disclosure: Charlyn T. owns shares in DBS, ES3, and VOO.