It’s an exciting time for the Singapore stock market.

A new type of IPO, special purpose acquisition companies (SPACs), have just made their debut on the local bourse.

SPACs are essentially blank-cheque companies that are listed with the intention of sourcing for a suitable operating company to merge with.

Investing in a SPAC is akin to a bet on the future as these vehicles hunt around for a fast-growing company in cutting-edge sectors.

There are currently three listed SPACs, namely Vertex Technology Acquisition Corporation (SGX: VTA), or VTAC, Pegasus Asia (SGX: PGU), and Novo Tellus Alpha Acquisition (GSX: NTU), or NTAA.

As with anything new, investors may find the wealth of information on SPACs daunting.

We have lined up the three SPACs side by side to help you to make sense of the information to make a more informed investment decision.

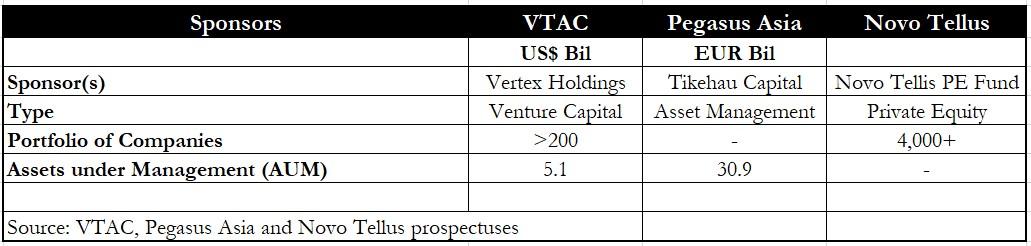

Sponsors

The sponsor for each SPAC is a crucial piece of information as a SPAC has no operating history or financials to speak of.

The table above provides a quick summary of each sponsor.

Investors should note that each SPAC has its strengths and merits and that they are not directly comparable.

VTAC is a venture capital outfit that has the support of investment firm Temasek Holdings. It has a portfolio of more than 200 companies that could be a de-SPAC target and manages an AUM of around US$5.1 billion.

Tikehau Capital is a European asset management firm with an AUM of EUR 30.9 billion, while Novo Tellus is a private equity fund manager that has an impressive portfolio of more than 4,000 investments.

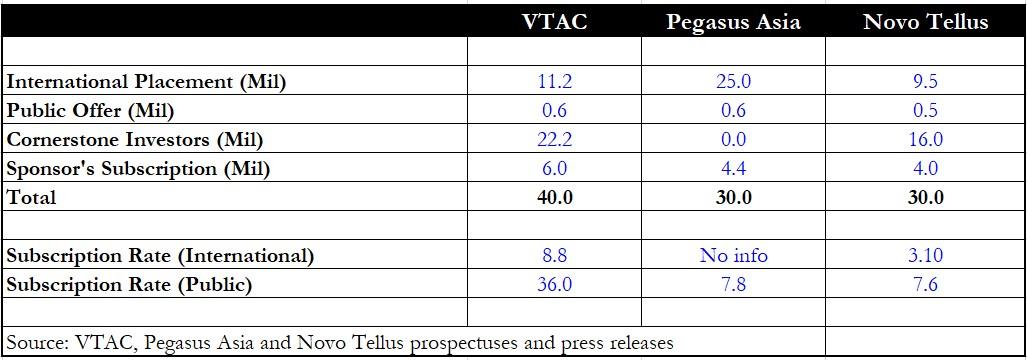

Offer details and subscription rate

The table above shows that for VTAC and NTAA, cornerstone investors took up a substantial chunk (>50%) of the total offer.

Pegasus Asia, however, did not have any cornerstone investors, but it offered the largest international placement of the three.

All three SPACs offered little by way of their public offers, with VTAC and Pegasus Asia offering 600,000 units each and VTAA offering just 500,000 units.

VTAC has the highest sponsor subscription rate, taking up 15% of the total offer size of 40 million units, with Pegasus Asia at 14.7% and VTAA at 13.3%.

In terms of subscription rates, VTAC saw the strongest demand with its public offer 36 times over-subscribed. Its international offer saw a subscription rate of 8.8 times.

In contrast, Pegasus Asia’s public offer was 7.8 times subscribed while NTAA’s offer saw a 7.6 times subscription rate.

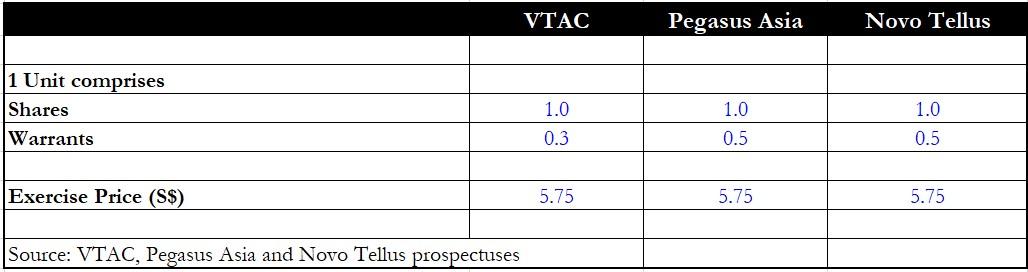

Shares and warrants details

SPACs have a unique feature in that each unit comes bundled with both a share and a detachable warrant.

Each warrant then allows you to subscribe for a share of the SPAC at the exercise price.

VTAC’s units come with one share and just 0.3 of a warrant, as opposed to Pegasus Asia and NTAA which offer one share and 0.5 of a warrant.

VTAC will offer an additional 0.2 of a warrant that will only be issued to holders of shares when the business combination is completed.

Investors should note that on the 45th day after the SPAC’s IPO, the shares and warrants will be detached and separately traded on the exchange.

All three SPACs have the same exercise price of S$5.75 for their warrants.

This means that holders of the warrants will only be in the money if the SPAC trades above S$5.75.

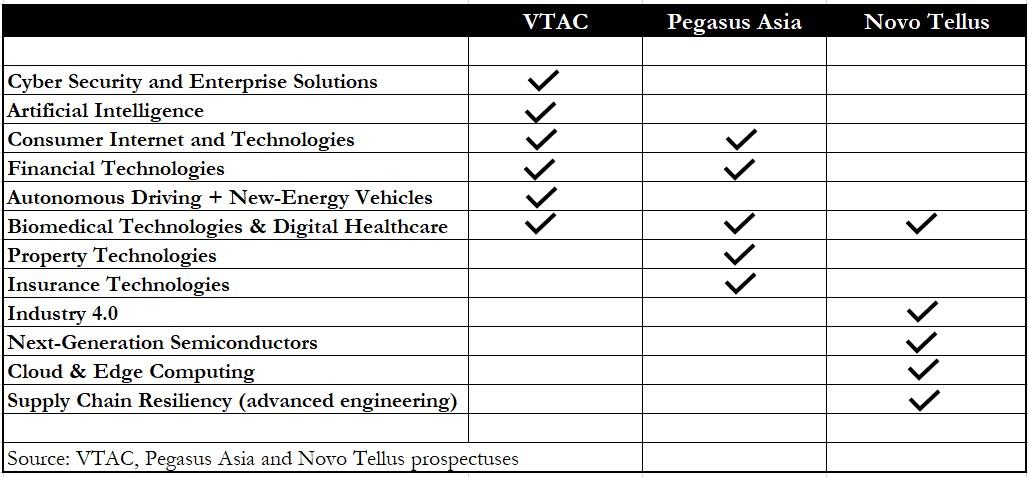

Target acquisition sectors

Next, we look at the industries that each SPAC is targeting for the business combination and subsequent de-SPAC.

There is a varied range of sectors that each SPAC is focused on, with some overlaps in terms of consumer internet, financial technology and medical technologies.

The differences highlight the strengths and preferences of each SPAC that each investor should take note of.

As for NTAA, its target is the technology and industrials sector in the Indo-Pacific region, and the SPAC’s investment themes are somewhat different from those of VTAC and Pegasus Asia.

It’s good news for investors as they have a buffet of choices when it comes to selecting a cutting-edge industry of their choice.

Unit price performance

Of the three SPACs, VTAC is thus far the only SPAC that is at its IPO price; the other two are trading below S$5 at the moment.

However, investors should note that it’s still early days for the SPACs and a lot hinges on both their ability to find a suitable de-SPAC target and the quality of the target business.

Get Smart: Suit your preferences

From the above, it’s clear that each SPAC has its strengths and merits.

Investors need to choose a SPAC that resonates with them in terms of the sponsor’s reputation and the investment themes and targets for that SPAC.

By the same token, a lot depends on the quality of the businesses injected as part of the de-SPAC, regardless of the SPAC.

For over 30 years, David Kuo has successfully built many winning portfolios. What’s his secret? We break it down for you in our latest FREE special report. Discover his strategies and stock insights for 2022. Click here to download now.

Disclaimer: Royston Yang does not own shares in any of the companies mentioned.