For many investors, REITs are seen as a stable and predictable income-generating asset class. But that has changed in the era of COVID-19.

Income-seeking investors have relied on REITs as a stable source of dividends for many years.

With the onset of the COVID-19 pandemic, many REITs have announced steep cuts to their distribution per unit (DPU).

Retail, commercial and hospitality REITs have been directly impacted by the lockdowns and social distancing measures implemented by countries around the world.

In particular, hospitality REITs have been the hardest hit sub-sector, as the hotels and serviced residences within their portfolios rely on tourist demand.

Today, we take a look at how badly hospitality REITs have been impacted, and try to figure out how the outlook is for them.

Steep declines in revenue and NPI

I took a look at four hospitality REITs — CDL Hospitality Trust (SGX: J85), Far East Hospitality Trust (SGX: Q5T), ARA US Hospitality Trust (SGX: XLZ) and Frasers Hospitality Trust (SGX: ACV).

For the quarter ended 31 March 2020, the four REITs reported double-digit declines in revenue ranging from 17% to 41%.

Declines in net property income (NPI) ranged from 21% to 52%.

Note that for ARA US Hospitality Trust, the numbers provided were against the manager’s forecast as the REIT had just been listed last year.

Revenue fell 24.5% against forecast, while NPI fell short by 68.2%.

The share prices of these four REITs have collapsed by 33% to 54% since the beginning of the year.

The worst is yet to come

Investors should note that performance for the quarter ended 31 March 2020 only included the lockdowns starting from March.

January and February have seen relatively normal trading conditions (apart from China).

As the pandemic has dragged on into April, numerous countries have started imposing lockdowns and border closures, while air travel came to a near standstill.

Hence, for the quarter ended 30 June 2020, these REITs should witness a significantly worse result as some hotels had to be shuttered, while others suffered a huge plunge in occupancy rates.

Investors need to brace themselves for steeper DPU cuts in the near-term, as the new measures announced recently allow for an extension of the permissible period for distribution of 90% of taxable income.

Adopting prudent measures

The four REITs in question have not stood idle, though.

The REIT managers have swung into action to try to mitigate the adverse impact arising from COVID-19.

CDL Hospitality Trust has announced that it will place asset enhancement initiatives (AEI) initiatives on hold, while also deferring non-essential expenditure.

Far East Hospitality Trust made a move to reduce management fees to the REIT manager. The base management fee was reduced from 0.3% to 0.28% with effect from 1 January 2020, while performance fee is now the lower of 4% of NPI or annual distributable income.

Frasers Hospitality Trust has retained 80% of its distributable income for the first half of the fiscal year 2020 to prepare for more pain ahead.

Get Smart: No glimmer of hope yet

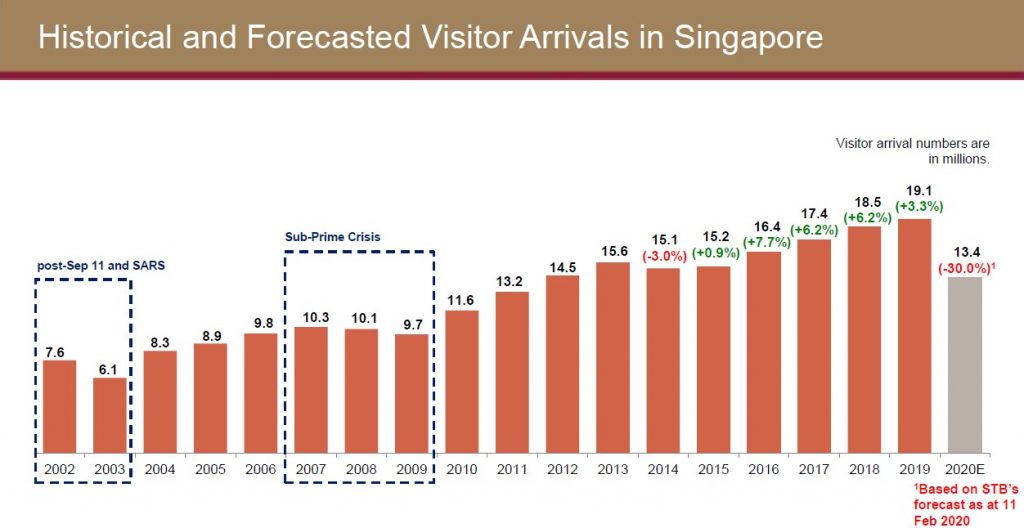

Source: Far East Hospitality Trust 2020 first-quarter presentation slides

Source: Far East Hospitality Trust 2020 first-quarter presentation slides

The above graph shows a projected steep decline in visitor arrivals based on the Singapore Tourism Board’s (STB) forecast as of 11 February.

At the time, the pandemic situation was not as severe, yet the forecast was for a 30% year on year decline to 13.4 million tourists.

With air travel curtailed and countries still struggling to effectively contain the virus, tourist arrivals could plunge even more sharply than what STB had forecasted three months ago.

To put things in perspective, the post-September 11 terrorist attacks and SARS epidemic also saw tourist numbers fall.

The outlook for hospitality REITs at this point is, therefore, still extremely murky.

While the REITs have undertaken actions to cut costs, investors should still expect more acute pain before things eventually start improving.

With share prices battered to multi-year lows, many attractive investment opportunities have emerged. In a special FREE report, we show you 3 stocks that we think will be suitable for our portfolio. Simply click here to scoop up your FREE copy… before the next stock market rally.

Disclaimer: Royston Yang does not own shares in any of the companies mentioned.