It has been more than 20 months since special purpose acquisition companies, or SPACs debuted on the Singapore bourse.

Back in January 2022, three SPAC candidates successfully listed on the Singapore Exchange, or SGX, namely Vertex Technology Acquisition Company (SGX: VT1), or VTAC, Pegasus Asia (SGX: PGS), and Novo Tellus Alpha Acquisition (SGX: NTA).

SPACs are blank-cheque companies listed to source for a suitable acquisition target to merge with.

Once a suitable business is identified, the SPAC will then undergo a process called “de-SPAC”, letting the new operating business take over.

VTAC was SGX’s very first SPAC to list, and the company has also become the first to announce a business combination with 17LIVE Inc.

Here are five things investors need to know about this transaction.

1. An up-and-coming live-streaming platform

17LIVE is a technology-driven live social entertainment platform.

According to independent research firm Frost and Sullivan, 17LIVE commanded the top pure-play streaming platform by revenue for both Japan and Taiwan.

The platform enjoyed a market share of 20.8% in Japan in 2022 and 26.9% in Taiwan in the same year.

17LIVE’s business model connects users with live streamers who generate content for which users pay using virtual gifts, which helps the streamer monetise his or her time.

The group content database encompasses a range of genres that include music, games, education, fashion, lifestyle, and cooking.

It also creates localised content and exclusive premium content and establishes partnerships and collaborations with local celebrities, politicians and athletes to produce exclusive content.

The business also holds online event marketing and competitions and ties these in with offline events to continuously engage its users.

2. A billion-dollar business

The purchase consideration for 17LIVE comes up to S$925.1 million, subject to certain financial targets being achieved.

S$803 million will be paid upfront with the issuance of 160,605,109 new shares in VTAC at an issue price of S$5 per share.

An additional 24,408,000 shares called the “earnout shares” will be issued to the vendors subject to the achievement of financial targets on the respective vesting dates of 30 April 2024 and 30 August 2024.

Assuming these shares are paid out, it will cost VTAC another S$122 million.

The earnout shares exist to incentivise the enlarged group (post-merger) to work towards achieving key performance targets for both revenue and profitability and to ensure the original shareholders of 17LIVE do not immediately dispose of their stakes.

When completed, the pro forma equity value of this business combination is projected to be around S$1.16 billion.

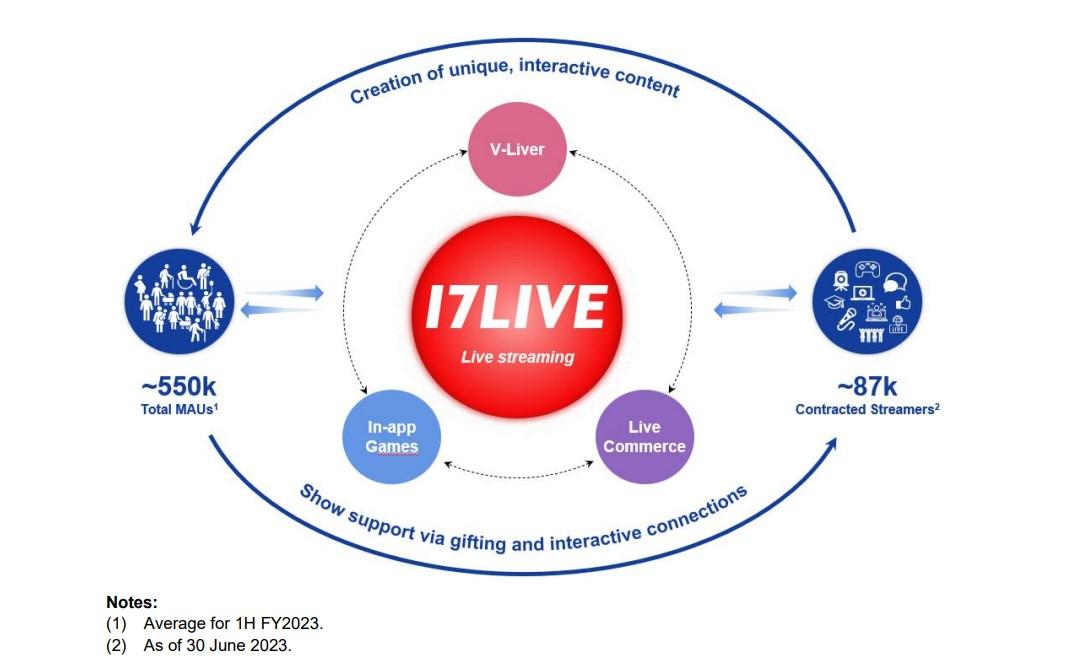

3. Impressive user statistics

17LIVE has shared several impressive user statistics.

Source: VTAC’s Business Combination Announcement

For the first half of 2023 (1H 2023), the business had an average monthly active user (MAU) of around 550,000.

Around one in six users are paying customers and each daily active user spends around 93 minutes viewing content on 17LIVE’s platform daily.

17LIVE has contracted with around 87,000 live streamers to generate content for its users.

V-Liver is a new streaming vertical introduced by 17LIVE in 2018 and is a type of live streamer which comprises computer-generated characters designed to resemble real people.

The virtual idol industry is projected to grow at around 44% per annum from 2022 to 2027 to end at US$3.9 billion, providing an attractive growth opportunity for the enlarged entity.

This segment has displayed strong growth momentum with approximately 75,000 average V-Liver MAU in the second quarter of 2023 (2Q 2023), more than doubling from a year ago.

Engagement also increased in tandem with an average of around 30,000 V-Liver spenders per month in 2Q 2023, up 2.7 times.

17LIVE has identified a total addressable market of US$7.8 billion for live streaming by 2027, growing at an annual rate of 20.1% over the next five years.

These numbers, along with a rise in digital natives and an increase in digital media platforms, should bode well for the group’s growth in the coming years.

4. Lumpy financial numbers

17LIVE’s financials, however, appeared lumpy over the past three years.

Operating revenue jumped 21% year on year for 2021 to US$497.8 million but then fell by 26.9% year on year in 2022 to US$363.7 million.

A net loss of US$51 million was incurred in 2022, and two out of three financial years saw net losses reported by the business.

17LIVE also had a net current liability of US$215.6 million as of 31 December 2022.

Furthermore, its cash flow from operations has also shrivelled from 2020 to 2022, going from US$67.4 million to just US$3.5 million.

5. An EGM to be held

A circular will be dispatched in early November with details of this transaction and is subject to SGX’s approval.

An extraordinary general meeting (EGM) will then be held in early December 2023 to vote on the business combination.

Once approvals are obtained and the resolution is passed at the EGM, VTAC will be renamed 17LIVE Group Limited.

By the time your child grows up, inflation will have gobbled up their savings. If you not only want to protect their money but also grow it, there are 3 SGX stocks you can consider buying. One has already proven to give a 55.8% dividend pay rise. Get all the details in our latest special FREE report. Just click here.

Disclosure: Royston Yang does not own shares in any of the companies mentioned.