The semiconductor industry looks poised to recover after grappling with a downturn for the past two years.

Excess inventory has pushed revenue and profits down this year but this is set to change.

The World Semiconductor Trade Statistics (WSTS) is projecting a 12.5% year-on-year (YOY) increase in the global semiconductor market in 2025.

Higher sales lead to higher profits — and for investors, the chance for higher dividends.

Here are three companies that might benefit from this recovery and increase their dividends in the next few years.

Micro-Mechanics (Holdings) Ltd (SGX: 5DD): A Generous Payout

Micro-Mechanics designs, manufactures and markets high-precision parts and tools used in process-critical applications for the semiconductor and other high-technology industries.

For the fiscal year (FY) 2024 ending 30 June, its revenue decreased by 13.6% YOY to S$57.9 million.

As a result, net profit fell by 17.7% YOY to S$8.0 million.

On a per-share basis, earnings per share declined by 17.8% YOY to S$0.0578.

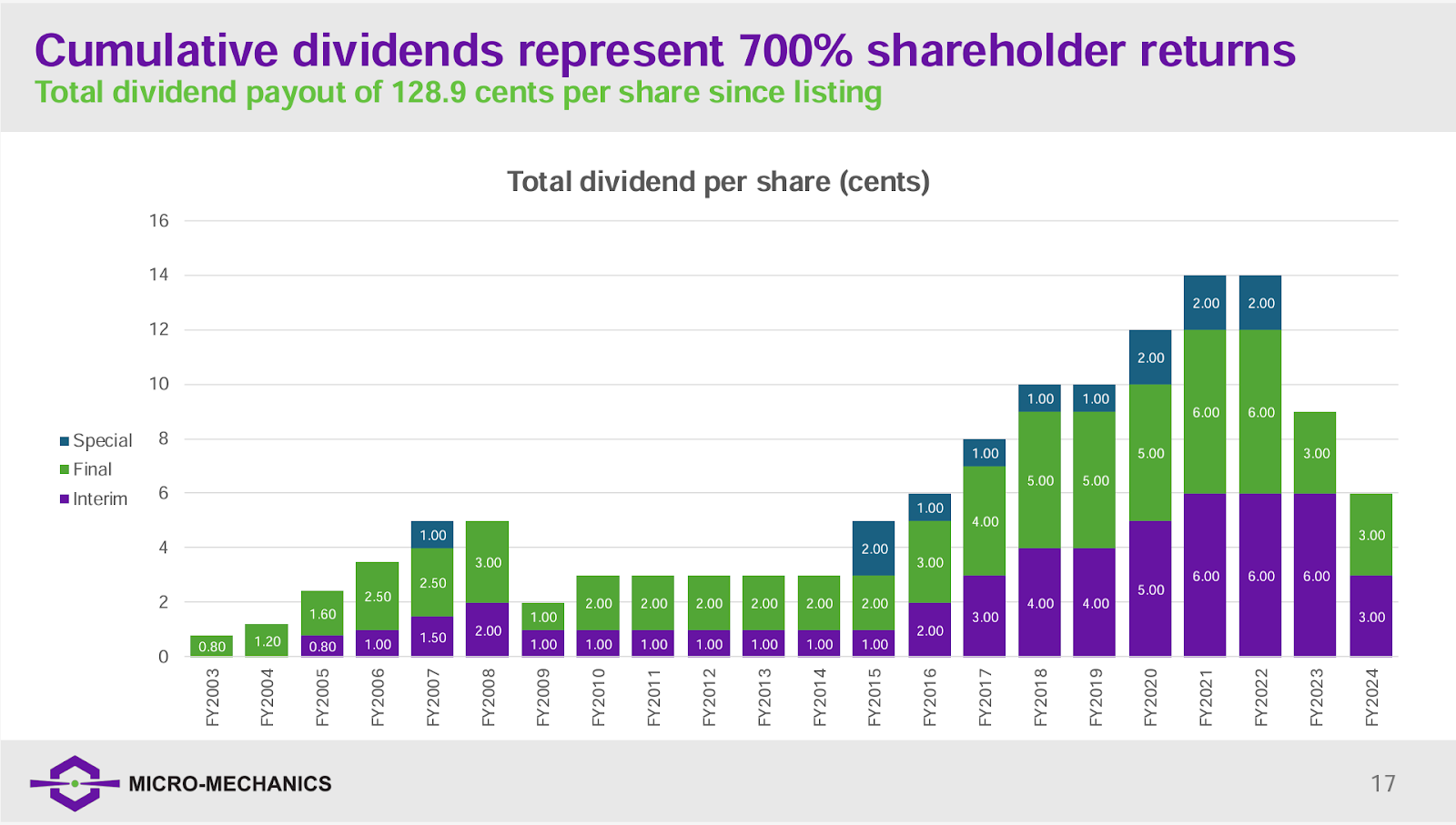

Despite the weaker performance, Micro-Mechanics continues to share its profits generously in the form of dividends, just like it did in the past.

Source: Micro-Mechanics FY2024 Presentation Slides

The company proposed a final dividend of S$0.03, bringing the total dividend for FY2024 to S$0.06, which translates to a payout ratio of 104%.

You might be wondering how Micro-Mechanics can pay out more than it earned.

The answer lies in its strong cash flow.

Although its net profit was just S$8 million, Micro-Mechanics generated S$12 million in free cash flow.

This healthy free cash flow not only allowed it to pay dividends but also increased its net cash position to S$16.4 million, which is S$2.3 million higher than the previous year.

Looking ahead, there are signs of recovery.

Micro-Mechanics has seen quarter-on-quarter improvement in its revenue, net profit and capacity utilisation.

If this momentum continues, FY2025 is likely to turn out to be a stronger year.

UMS Integration (Ltd) (SGX: 558): Expansion in Progress

UMS is a precision engineering group that specialises in manufacturing high-precision front-end semiconductor components.

The group’s core business includes the production of modular and integration systems.

For 2024’s first half (1H 2024), UMS reported a YOY drop in revenue of 29% to almost S$110 million, while net profit tumbled by 34% YOY to just over S$19 million.

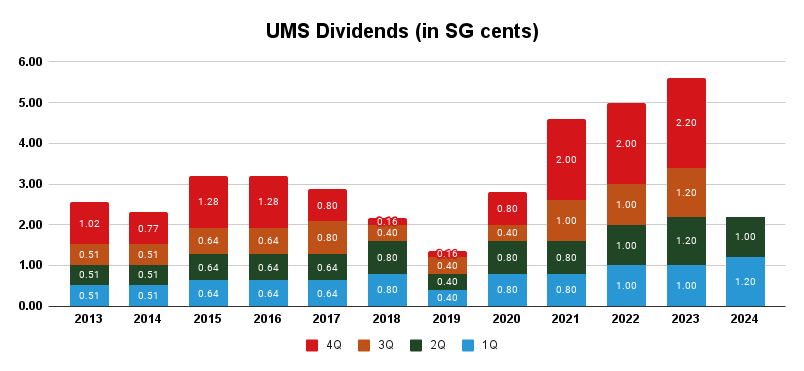

Like Micro-Mechanics, UMS is generous in sharing its profits with shareholders.

However, UMS retains a higher portion of its earnings for growth.

From 2019 to 2023, UMS has declared total annual dividends at the rate of approximately 34% to 73% of its net profit after tax.

Notably, UMS is one of the few locally listed companies to declare dividends on a quarterly basis, demonstrating its confidence in its business and commitment to boost shareholder value.

Source: Yahoo Finance, compiled by the author

To strengthen its growth prospects, UMS has widened its customer base and diversified its business portfolio.

In recent years, the company has reduced its reliance on the semiconductor segment, which made up almost all of its revenue in 2017.

By 2023, the semiconductor segment contribution declined to 87%, with its growing aerospace segment contributing 9%.

Moreover, UMS has secured a new major semiconductor customer and has commenced production at its new production facility at Penang Science Park North.

Looking ahead, UMS is optimistic about its outlook.

Not only did the company perform better in 2Q 2024 than 1Q 2024, it is well-positioned to benefit from the committed expansion plans of both its key customers in Malaysia and Singapore.

Additionally, its aerospace segment is poised to capitalise on the rebound in aviation and travel following the COVID-19 pandemic.

These factors suggest a promising overall outlook for UMS in the second half of 2024 and beyond.

Venture Corporation Limited (SGX: V03): Stronger 2H2024 Expected

Unlike the previous two companies, Venture is a significantly larger and more diversified business.

Semiconductor related products is one of its technology domains, but there are other notable domains in Venture’s portfolio include Life Science, Hyperscale Data Centres, and Luxury Lifestyle & Wellness.

Venture remains financially strong despite a 12.5% YOY decline in its revenue to S$1.4 billion, and an 11.7% drop in net profit to S$123.7 million in 1H 2024.

The company continues to generate robust operating cash flow which increased 4% YOY.

This healthy cash flow generation led to a higher net cash position of S$1.2 billion, representing a 33% increase compared to the previous year.

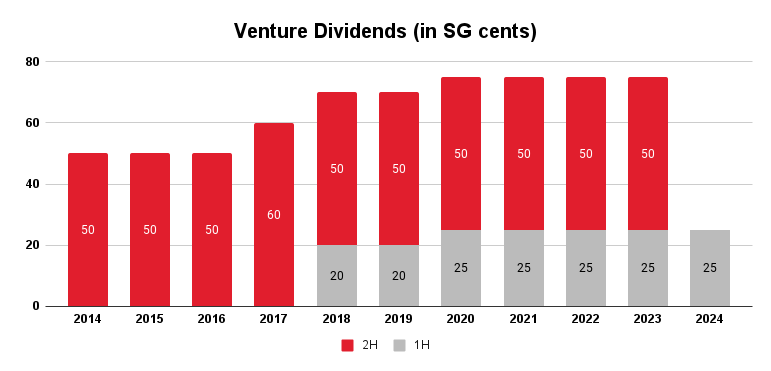

While Venture does not have a fixed dividend policy, it tries to pay equal, if not higher, dividends each year.

Since its listing in 1992, the company has paid dividends without interruption and has maintained or increased its dividends over the past decade.

Source: Yahoo Finance, compiled by the author

Similar to the other two companies, Venture is showing signs of recovery.

Both its revenue and net profit for 2Q 2024 are higher than 1Q 2024.

With the onboarding of new customers and new product introductions, Venture is optimistic about its prospect and expects a stronger performance in the second half of 2024 as compared to the first half.

Increasing dividends from business growth over the long-term

The improvement in the trio’s quarterly financial results suggest that the tide is turning for the semiconductor industry.

But the exact timing and extent of this rebound remains uncertain.

As a result, it’s difficult to predict whether the three companies will increase their dividends in the immediate future.

However, given their track record of sharing its profits with shareholders, an increase in dividend will always be on the cards if their businesses continue to grow over the long-term.

Eventually, the tide will turn.

Therefore, an effective strategy is to position your portfolio for the recovery of the semiconductor industry rather than attempting to pinpoint its exact timing.

Attention Growth Investors: Our latest report, “The Rise of Titans,” gives you a front-row seat on the 7 most influential US stocks today. If you’re passionate about tech and growth, you can’t go wrong with our research. Downloading this FREE report could be the most strategic move you make this year. Click here to get started now.

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclosure: Chan Kin Chuah owns shares in Micro-Mechanics, UMS Integration, and Venture Corporation.