Fear is a strong emotion, especially when it comes to investing.

Fear consumes us.

If left unchecked, it takes over and dictates the way we think.

Today, fear is paralysing, scaring us from buying stocks, even when we know we should.

Pause and think about the possible reasons why you may stop investing:

- Fear of an uncertain economy

- Fear that things will never get better

- Fear of share prices falling further

To ignore your fears is to pretend that they don’t exist.

Yet, to fear is to be human.

It’s the emotion lurking in your heart, uninvited, and must be confronted for you to get past it.

Confronting your fears

Fear doesn’t always have to be a negative emotion.

If we manage it well, fear can be a positive motivator too.

The fear of losing our ability to earn as we grow older spurs us to create multiple streams of income that will last us beyond our working years.

The fear of inflation eroding our purchasing power drives us to invest and seek higher rates of return compared to keeping our money in the bank.

The fear of not having enough for retirement pushes us to start planning earlier, giving us more time to compound our money.

Ultimately, fear is not a choice — we will feel it no matter how we try to deny it.

But how we manage our fears is our CHOICE.

How we move past the things that trouble us most, and deal with them head-on, is a decision we can make, regardless of the fear we feel.

Fear of an uncertain economy

It’s no secret that dark clouds are gathering on the horizon.

Whether it is runaway inflation, higher interest rates, or economic recession, all these troubles point in one direction — UNCERTAINTY.

Uncertainty over how long high inflation will persist.

Uncertainty over how long the US Federal Reserve will keep raising rates.

Uncertainty over the impact that a recession will have on businesses and subsequently, stock prices.

The thing is, worrying over what may or may not happen will not make you any more intelligent.

Worrying even causes you to miss out on the positive developments at companies.

For instance, Microsoft (NASDAQ: MSFT) just posted an 18% year-on-year growth in revenue for its fiscal year ending 30 June 2022 (FY2022), backed by growth in Microsoft Cloud services.

What’s more, the Redmond company delivered over US$65 billion in free cash flow and wields a balance sheet with almost US$55 billion in net cash.

In other words, the business is self-sufficient.

Microsoft does not rely on the kindness of bank loans to make ends meet. Nor does it need to worry over where interest rates are headed next.

The business is able to generate more cash than it needs and can sustain itself, come what may.

And that, for me, is far more useful and satisfying knowledge than the vague proclamations of economic troubles.

Bottom line: Worrying is a lot of wasted energy. Don’t let it consume your every waking hour. Use your time wisely.

Fear that things will never get better

The recent decline in the S&P 500 (INDEXSP: .INX) and NASDAQ (INDEXNASDAQ: .IXIC), down by over 23% and 34% from their respective peaks, appear to confirm investors’ fear over what will happen next.

In particular, the fear over how long such a decline will persist.

Large declines tend to draw comparisons with major downturns in the past such as the dot-com bubble bust in 2000.

In fact, bearish pundits will be all too happy to point out that the NASDAQ took over 14 years to recover its losses from the deep market crash in 2000.

Yet, such comparisons are misleading.

Firstly, it assumes that the unlucky investor will simply buy at the peak, and sit idly by for more than 14 years without investing further.

We can always choose to invest more over time, rendering the dotcom comparison moot.

Secondly, as the doomsayers are busy conjuring up worst-case scenarios, they often miss out on the performance of individual businesses.

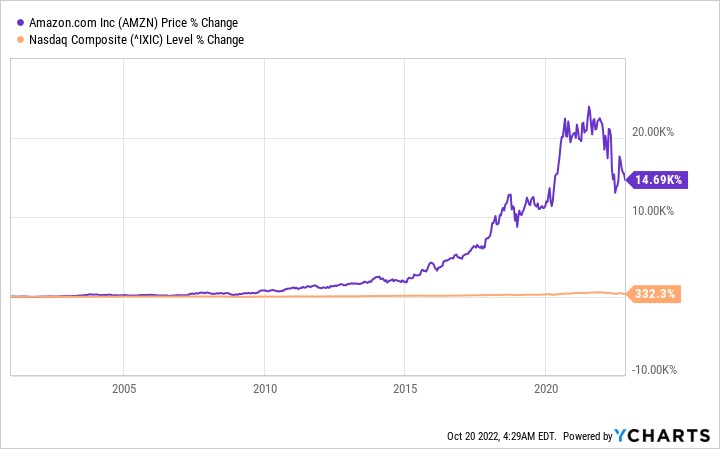

Take Amazon (NASDAQ: AMZN).

The dotcom bubble did leave a mark: the online retailer cut its workforce by 15% in 2001 in response to weaker consumer spending.

But if you had focused on the negative alone, you would have missed the forest for the trees.

Despite the short-term setback, it did not stop Amazon from growing its revenue from US$3.1 billion in 2001 to almost US$470 billion in 2021.

With a performance like that, it’s no wonder that shares of the tech giant have far outstriped the performance of the NASDAQ since 2001.

Even if you had the great misfortune of buying at the height of the dotcom bubble, you would still be way ahead.

Source: YCharts

Pessimists who are too busy dreaming up the worst-case scenarios will be left behind instead.

Bottom line: It’s easier to be a pessimist than it is to be an optimist today. Don’t fall into the trap of worst-case scenarios at the expense of the positive business developments happening around us.

Fear of falling stock prices

Finally, there’s the spectre of falling share prices.

If your stock portfolio today is filled with red ink, it’s like being handed a report card full of failing grades.

Yet, as hard as it is, we need to look beyond the short term in favour of what’s possible over the long term.

You see, in my book, there are two main components that can cause the share price to increase or decrease: the free cash flow per share (FCF per share) and the price to FCF (P/FCF) ratio.

Multiply these two factors, and you get the share price.

Here’s the thing …

In the short term, share price movements are dictated by changes in the P/FCF ratio, a reflection of the market’s sentiment.

Over the long term, it’s the business growth, represented by the FCF per share, that will be far more consequential compared to a change in the ratio.

Let me explain with an example.

When I bought shares of Apple (NASDAQ: AAPL) in June 2010 at a split-adjusted US$8.75 per share, the business had generated US$0.47 per share in FCF over its trailing 12 months.

The stock sported a P/FCF ratio of 18.7, as shown in the table below.

| FCF per share (TTM) | P/FCF | Share price | |

| June 2010 | US$0.47 | 18.7 | US$8.75 |

| October 2022 | US$6.62 | 21.2 | US$140.09 |

| Growth | 14.1x | 1.1x | 16x |

Fast forward to today, and shares have risen by 16.4 times to around US$144 per share.

If you compare the contribution of the FCF per share and the P/FCF ratio, the clear winner is Apple’s FCF per share that has ballooned from US$0.47 when I bought the shares to over US$6.60 today.

Therefore, the question investors have to answer is this:

Given the vast difference in contribution to Apple’s share price increase, what would you focus on: the FCF per share or the P/FCF?

The answer is obvious: the business, represented by Apple’s FCF per share.

Bottomline: Keep your eye on the ball. Over the long term, it’s the business growth that will determine your investment results.

Get Smart: Be curious, not judgemental

I’ll level with you.

All signs point to a recession on the horizon.

So, let’s not sugarcoat the situation.

Yes, it is possible that businesses will suffer in a recession, and post lower revenue and profits.

Yes, there is a possibility that share prices could fall further.

Yes, we do not know how long a recession, if any, will last.

And yet, by the same token, to be fearful of things that you cannot control is akin to spending time wallowing over things that may or may not happen.

What you chose to do today will define how well you do in the future, as an investor.

Would you choose to step up, acknowledge your fears, and address them head-on, or you can sit back, dream up worst-case scenarios and in the process, scare yourself from doing anything productive?

I’ll say one thing: the world does not need more pessimists today.

The next step is yours.

How do you decide if a growth stock is worth your money? There is no shortage of stock ideas today, but is a particular stock suitable for you? Find out more in our latest FREE report, How To Find The Best US Growth Stocks For Your Portfolio. Click HERE to download the report for free now!

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclosure: Chin Hui Leong owns shares of Amazon, Apple and Microsoft.