“There’s a pleasing sense of happiness for me”, sings the Carpenters from their famous song “Top of the World”.

That must be how bank investors are feeling after seeing the share prices of the trio of local banks hit new record highs.

DBS Group (SGX: D05) closed at S$42.40 last week while United Overseas Bank (SGX: U11), or UOB, and OCBC Ltd (SGX: O39) ended at S$35.69 and S$16.06, respectively.

The ebullient mood came about after all three banks released their latest third quarter of 2024 (3Q 2024) earnings reports.

But with all three banks hitting new all-time highs, which is the best one to pick for your portfolio?

We compare the trio of blue-chip names using different metrics to try to determine this.

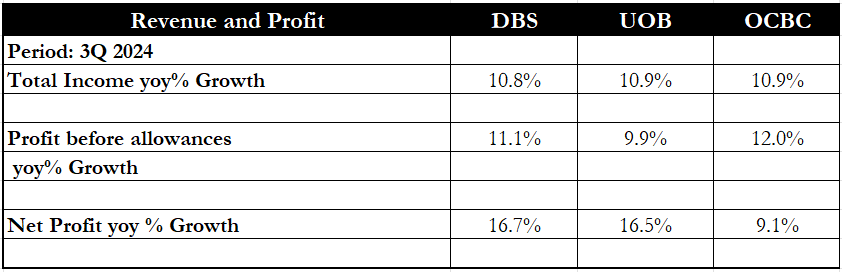

Revenue and net profit

Source: DBS, UOB and OCBC 3Q 2024 Earnings Release

First, we look at each bank’s financial performance.

It’s a tough comparison for this quarter as all banks did well, growing both their total income and net profit.

A high-interest-rate environment helped to boost net interest income while non-interest income also surged for all three lenders.

Fee income was boosted by an increase in wealth management fees and credit card spending.

Total income increased by nearly the same quantum for all the banks, but DBS emerged as the winner as its net profit jumped by the highest percentage among the trio.

Winner: DBS

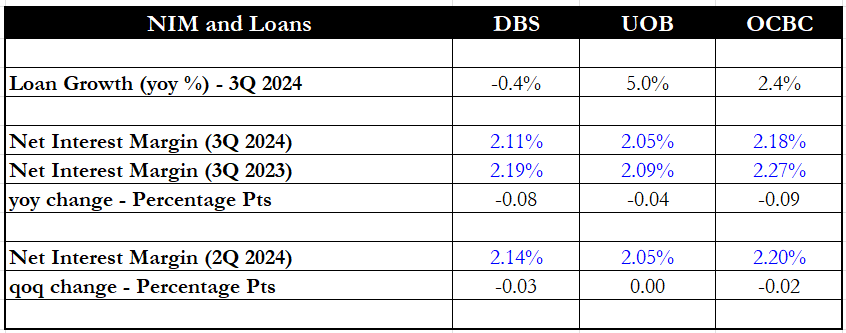

NIMs and loan growth

Source: DBS, UOB and OCBC 3Q 2024 Earnings Release

Next, we move on to each bank’s net interest margin (NIM) and peek into its loan book.

Loan growth was tepid for DBS as it was the only bank among the three to report a slight year-on-year drop in its loan book.

UOB posted the strongest loan growth of 5% year on year.

But when it came to NIM, OCBC boasted the highest NIM of the trio but also saw the largest year-on-year fall in its NIM, declining by 0.09 percentage points.

DBS also saw its NIM tumble by 0.08 percentage points from 2.19% to 2.11% over the same period.

Both DBS and OCBC also experienced quarter-on-quarter falls in NIM, by 0.03 and 0.02 percentage points, respectively.

Although UOB had the lowest NIM of the three, it saw the smallest year-on-year drop and also kept its NIM steady quarter-on-quarter.

Winner: UOB

Cost-to-income ratio (CIR)

Source: DBS, UOB and OCBC 3Q 2024 Earnings Release

The cost-to-income ratio, or CIR, comes next.

A lower CIR indicates that a bank is more efficient in expense control as its total expenses are a lower proportion of its total income.

OCBC had the lowest CIR of the three banks in 3Q 2024 and also saw the largest improvement in CIR as it fell by 0.6 percentage points year on year.

DBS’s CIR dipped by 0.02 percentage points year on year while UOB’s CIR increased by 0.5 percentage points over the same period.

Winner: OCBC

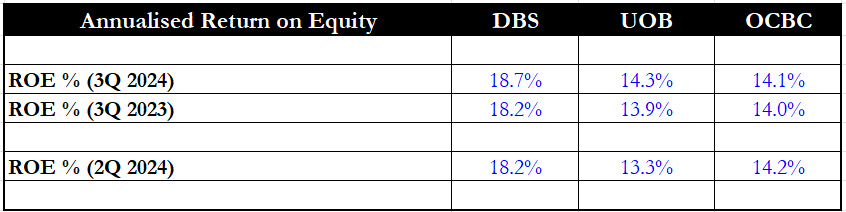

Return on equity (ROE)

Source: DBS, UOB and OCBC 3Q 2024 Earnings Release

Another important metric we looked at is each bank’s return on equity or ROE.

ROE measures the profitability of each lender with respect to its capital base, and a higher ROE means that a bank can squeeze out more profit per dollar of capital.

DBS wins this metric by far with an impressive ROE of 18.7% for 3Q 2024, improving on its 3Q 2023 ROE of 18.2%.

Credit should be given to UOB for increasing its ROE by a full percentage point quarter-on-quarter.

Winner: DBS

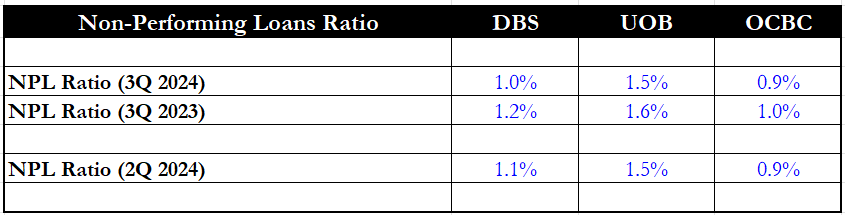

Non-performing loans ratio

Source: DBS, UOB and OCBC 3Q 2024 Earnings Release

The next metric looks at each bank’s non-performing loans ratio, or NPL ratio.

The NPL ratio measures the proportion of a bank’s loans that could go bad and is an indicator of the credit quality of the bank’s loan book.

Hence, a lower NPL ratio signifies that the bank’s loan book has better credit qualities.

OCBC takes the cake with an NPL ratio of 0.9%, and it has constantly kept its NPL ratio hovering at the 0.9% to 1% level.

DBS deserves special mention for lowering its NPL ratio by 0.2 percentage points year on year.

Winner: OCBC

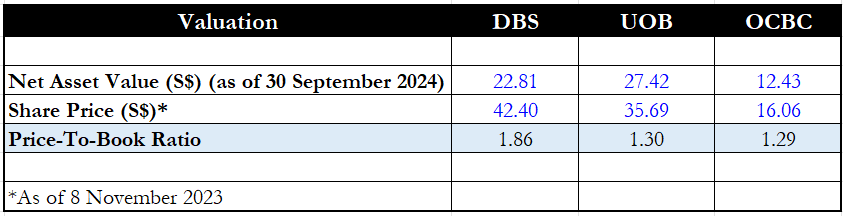

Valuation

Source: DBS, UOB and OCBC 3Q 2024 Earnings Release

Finally, we look at each bank’s valuation based on its price-to-book (P/B) ratio.

DBS is once again trading at the most expensive valuation at 1.86 times P/B after surging to its all-time high.

Both UOB and OCBC are evenly matched with a P/B ratio of around 1.3 times each.

OCBC is trading at a slightly lower valuation than UOB so it wins this round.

Winner: OCBC

Get Smart: The overall champion

There is something for everyone this round as all three banks have won at least one metric.

OCBC, however, is the overall winner as it has the lowest valuation, NPL ratio, and CIR.

OCBC also boasted strong year-on-year growth in its total income and net profit.

Investors need to review each bank holistically to make their decision.

For instance, DBS Group may seem more attractive as it is the only bank out of the three that announced a new S$3 billion share buyback programme where the bank will repurchase shares and cancel them.

By the time your child grows up, inflation will have gobbled up their savings. If you not only want to protect their money but also grow it, there are 3 SGX stocks you can consider buying. One has already proven to give a 55.8% dividend pay rise. Get all the details in our latest special FREE report. Just click here.

Disclosure: Royston Yang owns shares of DBS Group.