Many companies have enjoyed welcome relief as the pace of economic recovery picks up.

Blue-chip stocks such as Keppel Corporation Limited (SGX: BN4) and ComfortDelGro Corporation Ltd (SGX: C52) have both reported higher earnings and an increase in dividends.

Supermarket retailer Sheng Siong Group Ltd (SGX: OV8) has also reported a decent set of earnings as it ramps up its store growth.

However, pan-Asia retailer Dairy Farm International (SGX: D01), or DFI, has continued to face challenges.

Its share price hit an all-time low of S$2.42 recently and is down 47% in the last year.

Can the retailer manage a business recovery this year and see its share price pick up?

Weak financial performance

DFI reported a downbeat set of earnings for its fiscal 2021 (FY2021), underscoring the continued negative impact of the pandemic on its operations.

Sales fell by 12% year on year to US$9 billion with operating profit declining by almost 20% year on year to US$310.8 million.

Underlying net profit plunged by 62% year on year to US$105 million.

In line with the weaker performance, the group slashed its FY2021 dividend by 42% year on year to US$0.095, down from US$0.165 a year ago.

China weakness

Close to 70% of the reduction in net profit can be attributed to DFI’s stake in Yonghui Superstores (SHA: 601933).

If excluded, the group’s net profit would have declined by just 21.1% year on year to US$195 million.

Yonghui had contributed share of losses of US$90 million for FY2021 as it was impacted by reduced margins from rising competition and investments in its digital capabilities.

The rise in the number of COVID-19 cases since late-May 2021 had resulted in a space optimisation initiative for the group’s Mannings store network in Guangdong province in China.

This rationalisation has ensured that the brand is better able to grow and also leverage its 7-Eleven store infrastructure to push for higher sales.

Enhancing its loyalty programme

Despite the tough conditions, DFI has continued to build on its yuu Rewards programme.

The loyalty programme has garnered close to four million members, up from the three million last year.

yuu has expanded its ecosystem by roping in Chubb (NYSE: CB), Allianz SE (ETR: ALV) and Shell PLC (LON: SHEL) as new partners.

Because of yuu, daily e-commerce volume has more than doubled across the group in FY2021.

This programme has attracted high levels of engagement with over 130 billion points issued and 64 billion points redeemed since its launch.

yuu points have also led to a 50% increase in cross-banner shopping (read: across DFI’s different formats) since the start of FY2021.

Revisiting its strategic priorities

Management continues to report progress on its strategic initiatives, which are part of the group’s multi-year transformation plan.

7-Eleven South China continues to expand, with 200 new stores opened and 1,000 new products introduced during the year.

DFI’s Southeast Asian grocery retail division also reported strong underlying performance in FY2021, as its store sales per square metre increased by 25% relative to FY2019.

The group also relaunched the Giant brand in Singapore, opened its first new store in the island country in four years, and introduced its Low Prices That Last programme.

Building capabilities is another key pillar for DFI, with total training exceeding 300,000 hours in FY2021, more than double FY2019’s levels.

Johnny Wong was also brought in as the CEO of DFI Digital to accelerate the group’s digital transformation.

In line with driving its digital innovation agenda, not only has DFI tapped on its yuu rewards but has also experimented with alternative e-commerce offerings for customers.

CART, a new shopping experience that offers 20,000 products from Cold Storage, CS Fresh, Giant, and Guardian on one platform, was introduced in Singapore to boost e-commerce participation.

Finally, DFI has also launched over 1,300 new products under its house brand, Meadows, and now holds the number one position in multiple categories across the group.

Get Smart: Encouraging progress, but more time needed

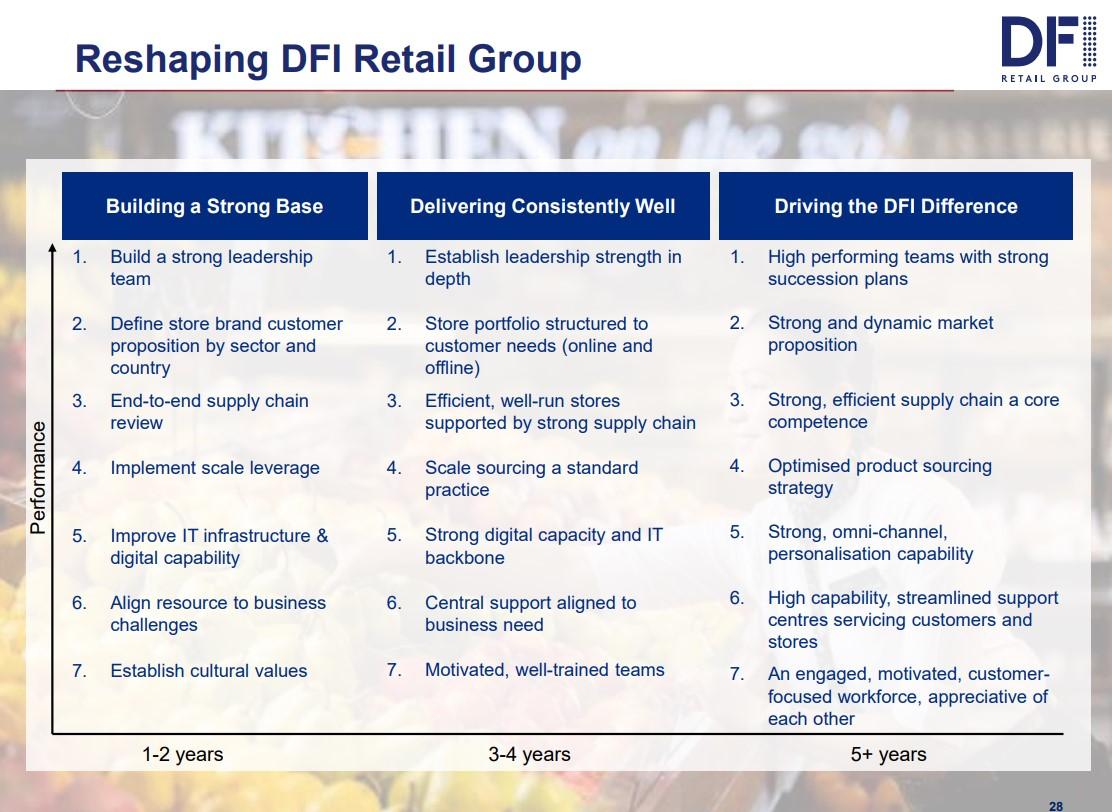

Source: DFI’s FY2021 Presentation Slides

DFI has made progress on the second phase of its transformation — delivering consistently well, and is now moving into its third phase — driving the DFI difference.

The summary of the three phases can be seen in the graphic above.

Despite its weaker results, the group has reported progress on many initiatives and is also seeing encouraging signs of recovery in its key markets.

However, more time is needed for DFI’s transformation to show tangible financial results, and investors may need more patience while management continues to execute.

What do real estate, Malaysia, Asia’s retail and healthcare have in common? They are a rich source of dividends! And in 2022, these 4 sectors look to be full of companies with healthy cash flows and dividends. If you want to own some of these stocks yourself, then grab a copy of our latest special report. Click here to download it for FREE.

Disclaimer: Royston Yang does not own shares in any of the companies mentioned.

Right Now")