Come January 2025, the CPF Special Account (SA) for individuals aged 55 and over will be closed.

Have you considered what to do with the excess savings in your CPF Ordinary Account (OA) once your Full Retirement Sum (FRS) or Basic Retirement Sum (BRS) has been met?

One option is to transfer them to your CPF Retirement Account (RA), up to the prevailing Enhanced Retirement Sum (ERS), which earns a minimum guaranteed 4% interest rate.

This move will earn you higher monthly payouts starting at age 65.

However, bear in mind that this transfer is irreversible.

Once transferred, your funds cannot be withdrawn for other purposes and will only be paid monthly when you turn 65.

Maintaining liquidity and investing for higher returns

Alternatively, you can keep your excess savings in your OA.

This option will provide you with liquidity and earn a decent interest rate of 2.5% per annum.

If you are looking for higher long-term returns, you can also consider investing a portion of your excess savings into stocks.

But wait, aren’t stocks risky?

Here’s the thing: while stock prices can fluctuate significantly in the short term, historical data show that investing in high-quality companies over the long term can be rewarding.

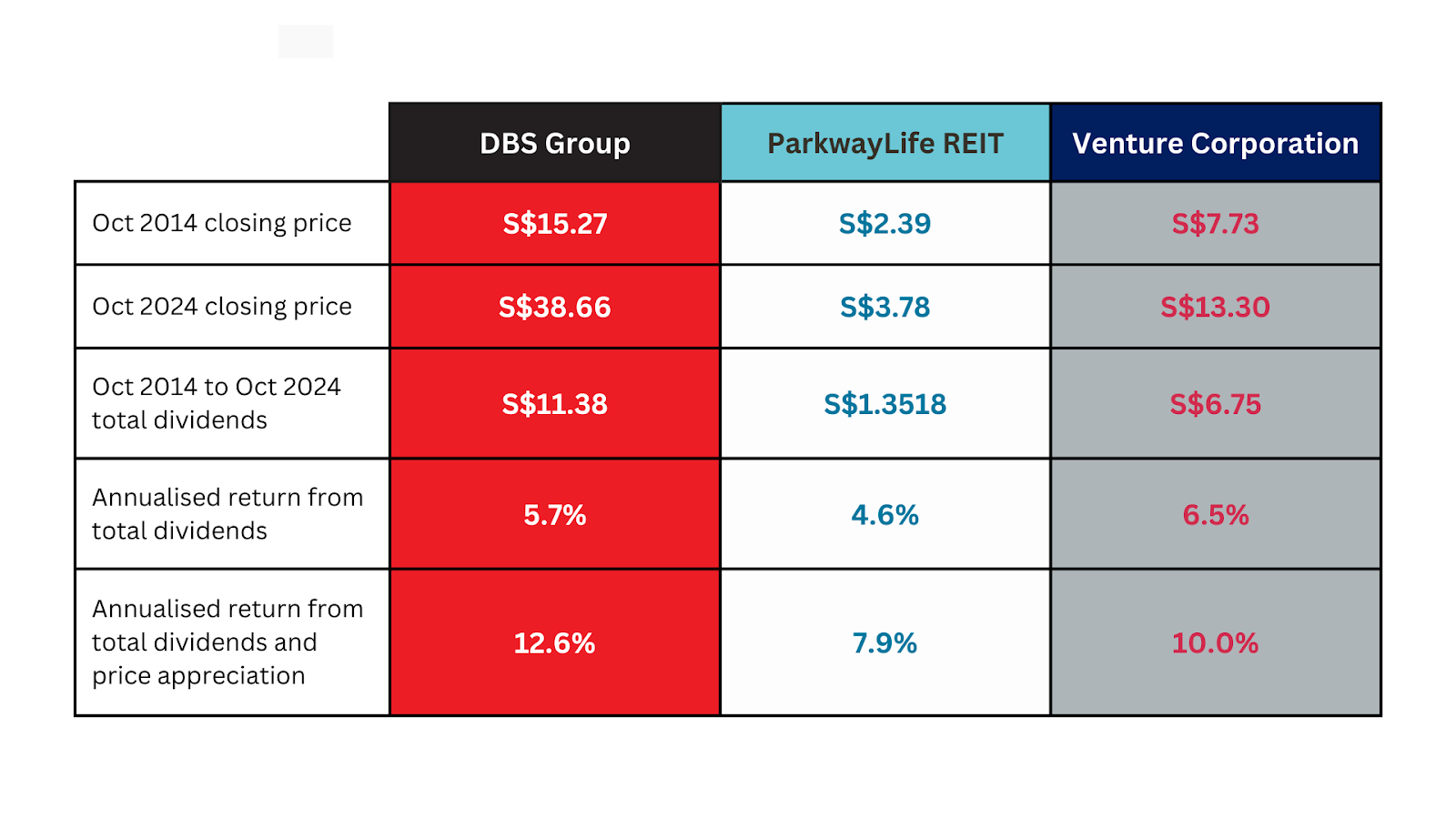

Let’s take a look at the performance of DBS Group (SGX: D05), ParkwayLife REIT (SGX: C2PU) and Venture Corporation Limited (SGX: V03) over the past decade.

As illustrated in the above table, the annualised returns from dividends collected over the 10-year period for all three companies would already exceed the RA’s interest rate.

If we include the share price appreciation, the total return is even more appealing.

For instance, S$10,000 transferred to RA would have grown to around S$15,000 after 10 years, but almost S$26,000 if invested in Venture.

Robust performance looks set to continue

The outperformance of these three stocks did not happen by chance.

Over the years, the three companies have grown both their revenues and net profits, leading to higher dividends and share prices.

Based on what we know today, these companies have a positive outlook.

For ParkwayLife REIT or PLife, despite facing headwinds in increased cost of borrowing and weakness in the Japanese Yen, the REIT has increased its year-to-date (YTD) distribution per unit (DPU) by 2.8% year-on-year (YOY) to S$0.113.

With a favourable lease structure with Parkway Hospitals Singapore till 2042, PLife is well positioned to continue the trend of increasing its DPU.

Moreover, PLife recently announced its first foray into a third key market – the acquisition of 11 nursing homes in France.

The acquisition is expected to be completed in this current quarter and is projected to be DPU accretive to unitholders on a pro forma basis.

Meanwhile, the appointment of new CEOs at DBS and Venture signals their preparation for the future.

There might be some concerns over leadership transitions, given the instrumental role of the previous leaders.

However, the successors are company veterans, and are well-positioned to ensure a seamless handover and continued growth.

For 3Q 2024, DBS reported another record quarter with net profit exceeding S$3 billion for the first time, a remarkable 15% growth over the previous year, given the bank’s size.

The bank achieved this result through strong growth in non-interest income and a stable net interest income, offsetting a slight margin decline with loan growth

DBS’s robust financial performance enabled it to maintain its quarterly dividend of S$0.54.

Additionally, it announced a new S$3 billion share buyback programme where shares will be purchased in the open market and then cancelled.

Venture, on the other hand, navigated a more challenging landscape, with its recovery hindered by the uneven demand from the various technological domains.

The company reported a slight sequential decline in its top and bottom lines in its latest announced third-quarter update.

Despite this setback, Venture continued to generate strong operating cash flow, boosting its net cash position by S$138 million to S$1.19 billion YTD.

This is impressive as it is on top of capital allocations for dividend payments and share buybacks for the year.

More importantly, it demonstrates the company’s strong financial health and commitment to its shareholders, even during business downturns.

Get Smart: There is no model answer

As the saying goes, “personal finance is more personal than finance.”

The decision to transfer your excess OA savings to RA or invest them depends on your unique circumstances and risk tolerance.

Transferring to RA offers a guaranteed return but limits liquidity. Investing in equities, on the other hand, promises higher returns but carries the risk of lower returns or even capital loss.

A mixed approach, combining both strategies, could be a prudent choice.

By allocating a portion of your savings to RA for stability and another portion to investments for growth potential, you can create a diversified portfolio that aligns with your long-term financial goals.

Attention Growth Investors: Our latest report, “The Rise of Titans,” gives you a front-row seat on the 7 most influential US stocks today. If you’re passionate about tech and growth, you can’t go wrong with our research. Downloading this FREE report could be the most strategic move you make this year. Click here to get started now.

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclosure: Chan Kin Chuah owns shares of DBS Group, ParkwayLife REIT, and Venture Corporation.