Why concentration?

A common recurring theme amongst a selected number of top investors in the world is that they generally tend to adopt a concentrated investing approach.

It is this concentrated approach to focus and invest in their best ideas that have led to outsized returns that have enabled them to beat the market.

“Diversification may preserve wealth, but concentration builds wealth. Wide diversification is only required when investors do not understand what they are doing.” says legendary investor Warren Buffett.

That said, on the other side of the table, we have investors that prefer to diversify and hold more stocks in their portfolio.

Therefore, the question of which style you should select, that of concentration versus diversification, has always been a pertinent consideration.

What conventional wisdom says

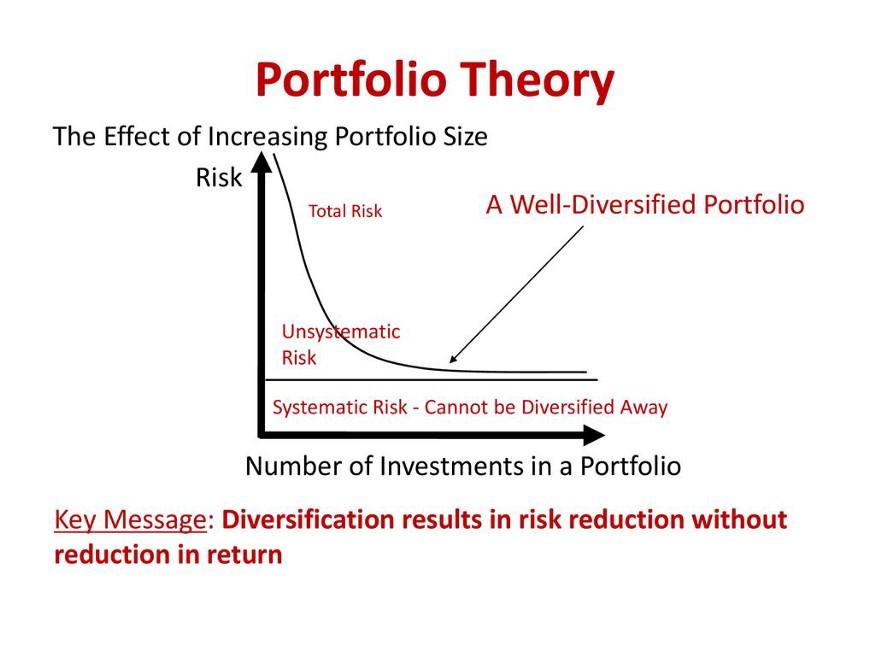

Modern Portfolio Theory argues that unsystematic risk (i.e. random risk, such as country, industry or company risk inherent in an asset) is the only risk that can be diversified away.

As we keep increasing the number of stocks within a portfolio, the majority of unsystematic risk ends up being diversified away, leaving behind largely systematic risk (i.e. market risk).

In simple terms: the more stocks you have, the more your portfolio tends to end up emulating the market (i.e. an index fund or an ETF) and you end up having average returns as risk reduces.

Why not concentrate your stock portfolio?

Concentration, especially if your stock portfolios have less than 10 stocks presents three key considerations, namely: (1) volatility, (2) returns, and (3) scalability.

The unexpected can happen

If you have a smaller portfolio (e.g. five to 10 stocks), the range of potential outcomes tends to be far wider than that of a larger portfolio (e.g. 20 to 25 stocks).

The price volatility (i.e. standard deviation) of a smaller stock portfolio tends to be higher as price movements are magnified by the stock concentration.

If prices move higher, it is a good thing to have and be happy about.

But if prices go lower for unexpected reasons that could be stock specific and beyond your control, such declines can significantly impact your overall portfolio return.

Cutting your winners

If you run a concentrated portfolio (e.g. a five-stock portfolio), you face a problem when your winners become multibaggers (i.e. a stock multiplying by many times your original investment cost).

By doing so, they become outsized and could well end up forming a significant percentage of your portfolio that is way beyond your comfort zone (think 40 to 60%).

When this happens, what most portfolio managers do is that they end up continuously trimming these winners to avoid over-concentration.

Sadly, this action works against them.

Winners are important because they tend to contribute to the overwhelming majority of your returns.

When you trim your winners and reallocate capital to the next lower performing idea, you end up constantly reallocating capital from the winners to the poorer-performing winners.

The continuous long-term drag from cutting your long-term winners will eventually impact longer-term investing performance negatively.

“You want to bet on the winning horse, not the next best winning pony.”

Not scalable

The investment strategy that you choose has to be scalable as the size of your funds grow.

If one adopts a concentrated approach, there is an implicit theoretical limit on how big the fund can grow, because one wants to avoid becoming one of the major shareholders of a company.

As the portfolio continues growing, the universe of companies starts to shrink and the size (i.e. market capitalisation) of the companies also starts to increase.

In general, bigger companies tend to have smaller moves and smaller companies tend to have bigger moves, so the portfolio ends up having to either (1) cap its fund size and/or return capital or (2) invest in larger companies.

For the latter option, the gravitation toward larger companies will lead your portfolio more and more towards benchmark-like returns.

Why diversification?

Diversification allows you to let our winners run high, and not having to trim them, and water your weeds instead.

Diversification allows you to have peace of mind on any given day, knowing that no one stock accounts for such a large portion of the portfolio that you will not be able to sleep soundly.

You would rather let your winners concentrate within your portfolio, which is very similar to the way many venture capital companies (“VCs”) invest in startups.

They have a diversified approach with many investments.

But the majority of VC’s performance is driven by the few winners that turn into unicorns.

In our case , it is the winners, the compounders and multi-baggers that chalk up a return of 3x, 5x or 10x and more.

We certainly don’t know what the market will bring, or how the stock prices will be today, tomorrow or next month.

But one thing that is very likely is that if growth continues, with rising revenues, profits and cash flows, the businesses that we invested in should do well over the long-term.

And that’s all you should care about, rather than be bothered by market noise.

Get Smart: Choose what works for you

Your portfolio allocation should ultimately reflect your conviction.

The size of an investment should be proportional to your assessment of the probability of success and failure.

Invest in a way that best suits you, your own investing style and mindset, and you will do just fine over the long-term.

If you want more stock ideas, start looking out for these 5 unique traits in the stock market. Companies with these traits can possibly pay you dividends for life. Discover what these traits are in your FREE special report “Dividend Stocks That Can Pay You For Life”. Click here to download now.

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclaimer: Eugene Ng does not own shares in any of the companies mentioned.