The REIT sector has been through the twin headwinds of high interest rates and surging inflation.

However, there are pockets of strength amid the challenges.

Mapletree Investments Pte Ltd is viewed as a strong sponsor that has three REITs under its belt.

Two of these are Mapletree Industrial Trust (SGX: ME8U), or MIT, and Mapletree Logistics Trust (SGX: M44U), or MLT.

We compare these two REITs to see which makes the better investment choice.

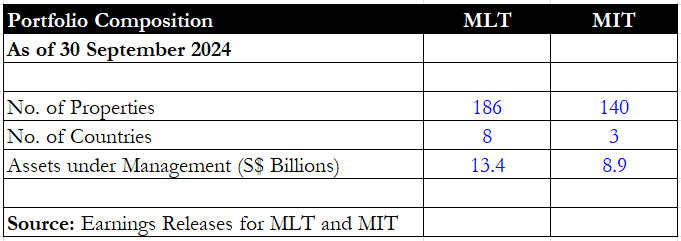

Portfolio composition

First, we look at the composition of each REIT’s portfolio.

Both MIT and MLT have more than 100 properties each within their portfolio, making their rental income diversified and resilient.

However, MLT is present in more countries (eight) such as Malaysia, India, China/Hong Kong, Japan and Australia.

By contrast, MIT is only present in three key countries – Singapore, the US, and Japan.

MLT also has a larger asset under management (AUM) base compared with MIT.

Winner: MLT

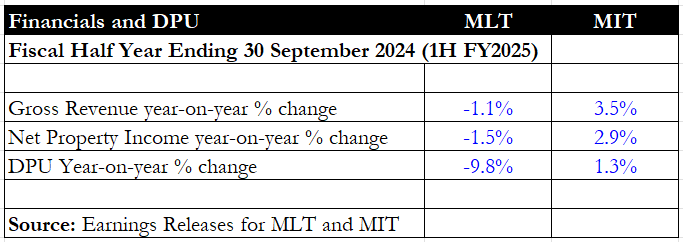

Financials and DPU

Next, we move on to each REIT’s financial and distribution per unit (DPU) performance.

Note that the numbers above relate to the earnings report for the first half of fiscal 2025 (1H FY2025) ending 30 September 2024.

MIT saw a 3.5% year-on-year increase in gross revenue coming from additional contributions from its Osaka data centre which was acquired in September last year.

Furthermore, rental renewals also contributed to the higher revenue.

As for MLT, lower contributions from China along with the depreciation of regional currencies against the Singapore Dollar caused gross revenue to dip by 1.1% year on year to S$365 million.

MIT managed to report a higher year-on-year DPU despite the presence of higher borrowing costs.

MLT, on the other hand, saw borrowing costs increase by 8.8% year on year to S$78.3 million.

This increase in borrowing costs, along with an enlarged unit base, caused MLT’s DPU to tumble by 9.8% year on year to S$0.04095.

Winner: MIT

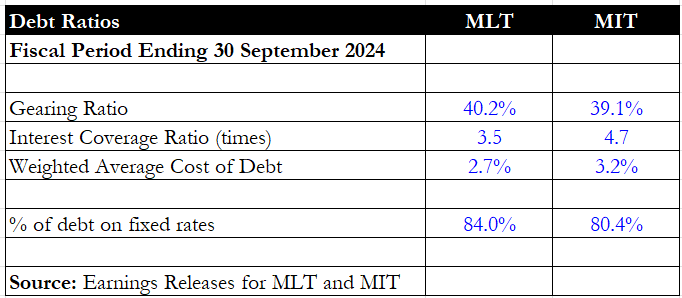

Debt metrics

Looking at each REIT’s debt metrics, it’s clear that both MIT and MLT have roughly the same gearing ratio.

MIT, however, enjoyed a higher interest coverage ratio of 4.7 times versus MLT’s 3.5 times.

MLT also enjoyed a lower cost of debt at 2.7% versus MIT’s 3.2%.

However, investors should note that despite the higher cost of debt on MIT’s part, its borrowing costs for 1H FY2025 inched up just 1% year on year.

MLT also has a slightly higher proportion of its debt on fixed rates at 84% versus 80.4% for MIT.

Winner: MLT

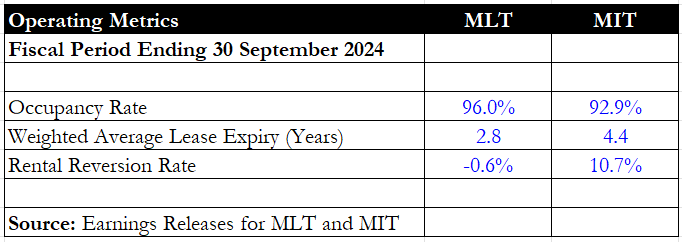

Operating metrics

Operating metrics are up next, and both MIT and MLT boast very high portfolio occupancy rates above 90%.

MLT’s occupancy was higher than MIT at 96% versus 92.9%, giving the logistics REIT an advantage here.

However, MIT had a longer weighted average lease expiry period of 4.4 years, thereby ensuring more rental income certainty.

MLT also reported a negative rental reversion rate as China remained a drag on the portfolio. If China was excluded, MLT’s rental reversion rate would have been positive at 3.6%.

Even at 3.6%, MIT’s rental reversion rate of 10.7% would have been almost triple that of MLT, making the industrial REIT the clear winner for this category.

Winner: MIT

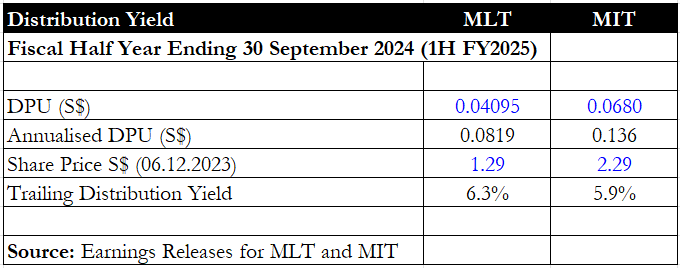

Distribution yield

Finally, we come to arguably the most important metric for both REITs – the distribution yield.

MLT has a slightly higher distribution yield compared with MIT, at 6.3% versus 5.9%.

However, income investors also need to assess the sustainability of this yield and not focus on the absolute yield alone.

MIT managed to eke out a small year-on-year increase in its DPU while MLT’s DPU is under pressure because of weak regional currencies and China.

Winner: MIT

Get Smart: Ongoing capital recycling

The winner for this round is MIT as its sister REIT, MLT, is mired in troubles that are depressing its DPU and causing portfolio rental reversions to turn negative.

Despite the challenges, MLT has engaged in accretive acquisitions and capital recycling to mitigate the fall in distributable income.

Three acquisitions were completed year-to-date in Malaysia and Vietnam.

MLT also announced the divestment of eight properties with older specifications and limited redevelopment potential.

These properties are in Malaysia, China, and Singapore.

MIT is not sitting idly, either.

The industrial REIT acquired a 98.47% stake in a multi-storey, mixed-use freehold property in Tokyo, Japan, for around S$127.8 million.

This property is located in a strategic location with potential redevelopment into a new data centre.

Want more dividends in 2024? Our latest FREE report spotlights five Singapore REITs with distribution yields of 5.5% or more, a rare find in today’s market. These are reliable, proven performers. Just one stock inside could boost your portfolio’s returns in the next few months. Download your report today and start reaping the benefits.

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclosure: Royston Yang owns shares of Mapletree Industrial Trust.