With the year almost wrapping up, it’s a good time to take a look at the REIT sector.

Sentiment has been poor towards this asset class because of still-high interest rates and elevated levels of inflation.

However, REITs with strong sponsors have done well in mitigating these headwinds.

CapitaLand Investment Limited (SGX: 9CI) is recognised as a solid sponsor that has expertise in managing properties within its REITs.

We compare two REITs under its umbrella – CapitaLand Integrated Commercial Trust (SGX: C38U), or CICT, and CapitaLand Ascendas REIT (SGX: A17U), or CLAR, to see which makes the better investment.

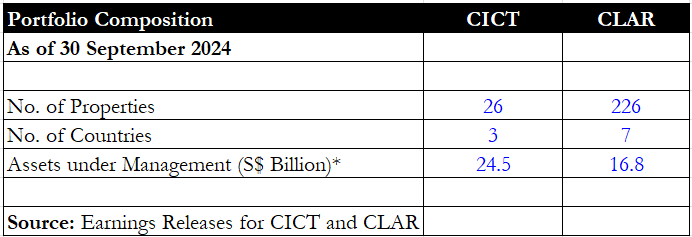

Portfolio composition

To start, we take a look at each REIT’s portfolio composition from their latest third quarter of 2024 (3Q 2024) business updates.

From the numbers above, it’s clear that CLAR has around nine times more properties in its portfolio compared with CICT.

Not just that, but CLAR is also present in more than double the number of countries than CICT’s portfolio.

Although CICT has a larger assets under management (AUM) of S$24.5 billion compared to S$16.8 billion, CLAR’s diversification is still much more impressive.

Winner: CLAR

Financials and DPU

Next, we look at each REIT’s financials and distribution per unit (DPU).

As these REITs only pay out distributions on a half-yearly basis, we used the numbers as of 30 June 2024.

CICT shows superior expense management as its net property income (NPI) rose more than its gross revenue.

The retail and commercial REIT also eked out a small year-on-year rise in its DPU to S$0.0543.

In contrast, CLAR saw its DPU fall by 2.5% year on year because of higher finance costs and a larger base of issued units.

Winner: CICT

Debt metrics

The next attribute we look at are the debt metrics for each REIT.

As REITs are now mired in a higher interest rate environment, these metrics become all the more important in determining which REIT manager is superior.

Both REITs have roughly the same level of gearing and both are below the 40% level.

Their weighted average cost of debt is also hovering around the same level of 3.6% to 3.7%.

However, CLAR has the upper hand with a higher interest coverage ratio of 3.7 times along with a greater proportion of its debt (80.2%) pegged to fixed rates.

Winner: CLAR

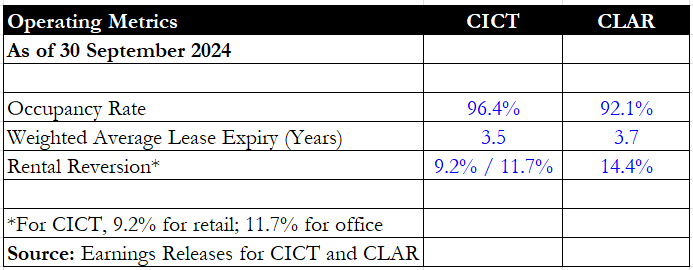

Operating metrics

Operating metrics come next and CICT sports a much higher portfolio occupancy rate of 96.4% compared with CLAR’s 92.1%.

This higher rate attests to the strong demand for CICT’s retail and commercial properties.

In terms of weighted average lease expiry (WALE), both REITs have roughly the same.

CLAR enjoys a much stronger rental reversion rate of 14.4% compared with CICT, but investors should note that the two REITs represent different asset sub-types.

CICT has retail and commercial properties within its portfolio while CLAR’s portfolio comprises industrial properties.

We feel that the occupancy rate in this case is the better judge of which REIT is the winner for this category, as both have exhibited strong positive rental reversions.

Winner: CICT

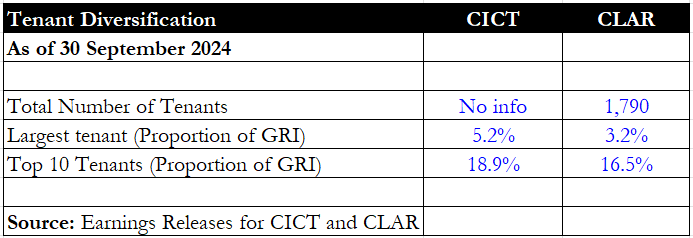

Tenant mix

Next, we look at tenant diversification which is an important aspect of how resilient a REIT is when a downturn arrives.

If a REIT is too reliant on a few large tenants, this makes it riskier should any of these tenants get into financial trouble.

CICT’s largest tenant makes up 5.2% of its gross rental income (GRI) while CLAR’s is only 3.2%.

For the top 10 tenants, CICT also loses out to CLAR as it has 18.9% of GRI compared with just 16.5% for CLAR.

Winner: CLAR

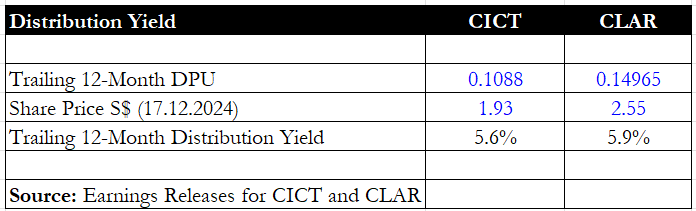

Distribution yield

Finally, we come to the most important aspect of a REIT – its distribution yield.

This attribute is what many income investors look for when deciding on which REIT to purchase.

CLAR has a slightly higher distribution yield of 5.9% compared with CICT’s 5.6%.

However, it’s important to note that DPU sustainability is more important than the headline yield.

REIT investors should carefully study the trajectory of each REIT’s DPU to determine if it can be sustained or even improved in future years.

In other words, distribution yield should not be looked at in isolation.

Winner: CLAR

Get Smart: Improving their respective portfolios

It’s a tough decision to make when comparing these two quality REITs.

On one hand, CICT has grown its DPU but its portfolio is more concentrated and has a lower distribution yield.

On the other hand, CLAR boasts a higher distribution yield but has a lower portfolio occupancy and saw its DPU fall year on year.

Investors need to find out which attributes they prefer when it comes to choosing between the two.

Alternatively, you can also choose to own a bit of both.

The good news is that both CICT and CLAR are working to improve their portfolios.

CICT’s value creation strategy includes asset enhancement initiatives (AEIs) for its IMM Building in Singapore and Gallileo in Germany.

The REIT also recently concluded its purchase of a 50% stake in ION Orchard Mall.

Over at CLAR, the industrial REIT just completed two AEIs in 3Q 2024 for two Singaporean properties.

It also has six ongoing projects worth S$572.6 million to redevelop and refurbish six properties in Singapore (5) and the US (1).

In our latest report, we dive into five standout Singapore REITs offering distribution yields exceeding 5.5%. Why settle for less? Get more dividends hitting your bank account with our REITs guide. Click here to download for free now.

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclosure: Royston Yang does not own shares in any of the companies mentioned.