Growth investors may be pleased to know that growth stocks have performed well this year.

The bellwether technology stock index, the NASDAQ Composite Index, has surged nearly 35% since October last year and has risen by 30.7% year-to-date.

This impressive performance could be due, in part, to the poor performance of growth stocks in 2022 when the NASDAQ Composite Index lost a third of its value.

In hindsight, it seems investors were probably too pessimistic back then and only saw bad news ahead.

Despite the rebound, you may be surprised to know that there are still cheap growth stocks to be found.

These stocks are cheap from both a valuation perspective and considering the prospects of the business.

Here are four US growth stocks that could see more share price upside as they remain cheap by historical standards.

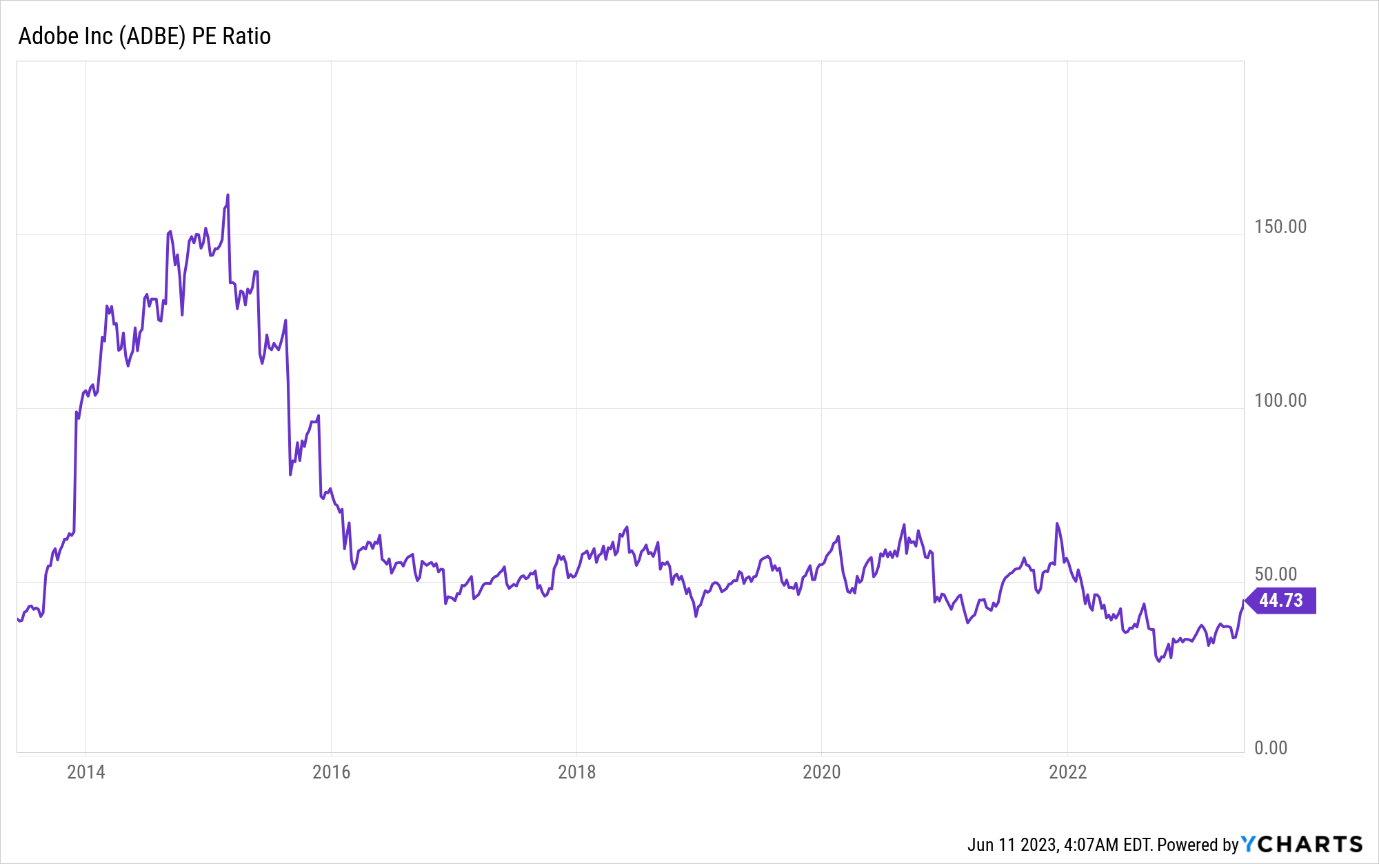

Adobe (NASDAQ: ADBE)

Source: Y-Charts

The software company, which sells a variety of cloud software that enables users to manipulate and personalise their images and videos, is trading at a compelling valuation of around 45 times the price to earnings.

This is despite the shares of Adobe surging by 42.2% year to date.

The company had reported record revenue for its fiscal 2023’s first quarter (1Q FY2023) of US$4.7 billion, up 9% year on year.

Adobe also generated a positive free cash flow of US$1.6 billion for the quarter and ended 1Q FY2023 with remaining performance obligations (RPO) of US$15.2 billion.

Adobe CEO Shantanu Narayen has also raised the company’s full-year guidance for digital media’s new annual recurring revenue and earnings per share.

Recently, the software giant has also integrated its Adobe Firefly generative artificial intelligence (AI) capabilities into Adobe Express, its all-in-one app that includes the company’s suite of popular products such as Photoshop, Illustrator, and Acrobat.

This move will boost the capabilities of its cloud software and endear more customers to it, helping to increase stickiness.

Netflix (NASDAQ: NFLX)

Netflix is a streaming TV giant with around 233 million paid subscribers in more than 190 countries to its movies and TV shows.

Source: Y-Charts

Like Adobe, Netflix’s share price has shot up by 47.7% year to date but valuation-wise, the streaming TV company still looks cheap at 45.2 times earnings (see chart above).

For its recent fiscal 2023’s first quarter (1Q 2023), revenue continued to climb, edging up 3.7% year on year to US$8.2 billion.

Net profit, however, slipped slightly from US$1.6 billion a year ago to US$1.3 billion.

However, the company generated more than US$2.1 billion of free cash flow, more than the previous four quarters combined.

Netflix has also continued chalking up membership growth, with its latest 1Q 2023 membership rising by 4.9% year on year to 232.5 million.

Late last month, the company widened its crackdown on password sharing in the US and more than 100 countries, alerting members that their accounts cannot be shared with others outside their households.

As a result, Netflix has seen more than 200,000 new sign-ups, according to data streaming analysis website Antenna.

PayPal (NASDAQ: PYPL)

PayPal is a financial technology company operating an online payments platform that supports secure and convenient money transfers between customers, merchants, and banks.

The stock has lost around 11% year to date and now trades at its lowest price-to-earnings valuation of 26.9 times in the last 10 years (see graph below).

Source: Y-Charts

The company’s business is faring well, though.

For 1Q 2023, net revenue rose 9% year on year to US$7 billion, with operating profit jumping 41% year on year to US$1 billion.

The payments company also generated a positive free cash flow of US$1 billion.

Total payment volume grew 10% year on year to US$354.5 billion.

PayPal has raised its guidance for the full year and now expects its earnings to grow by 20% year on year.

It also expects to generate around US$5 billion in free cash flow and will spend around US$4 billion to buy back shares.

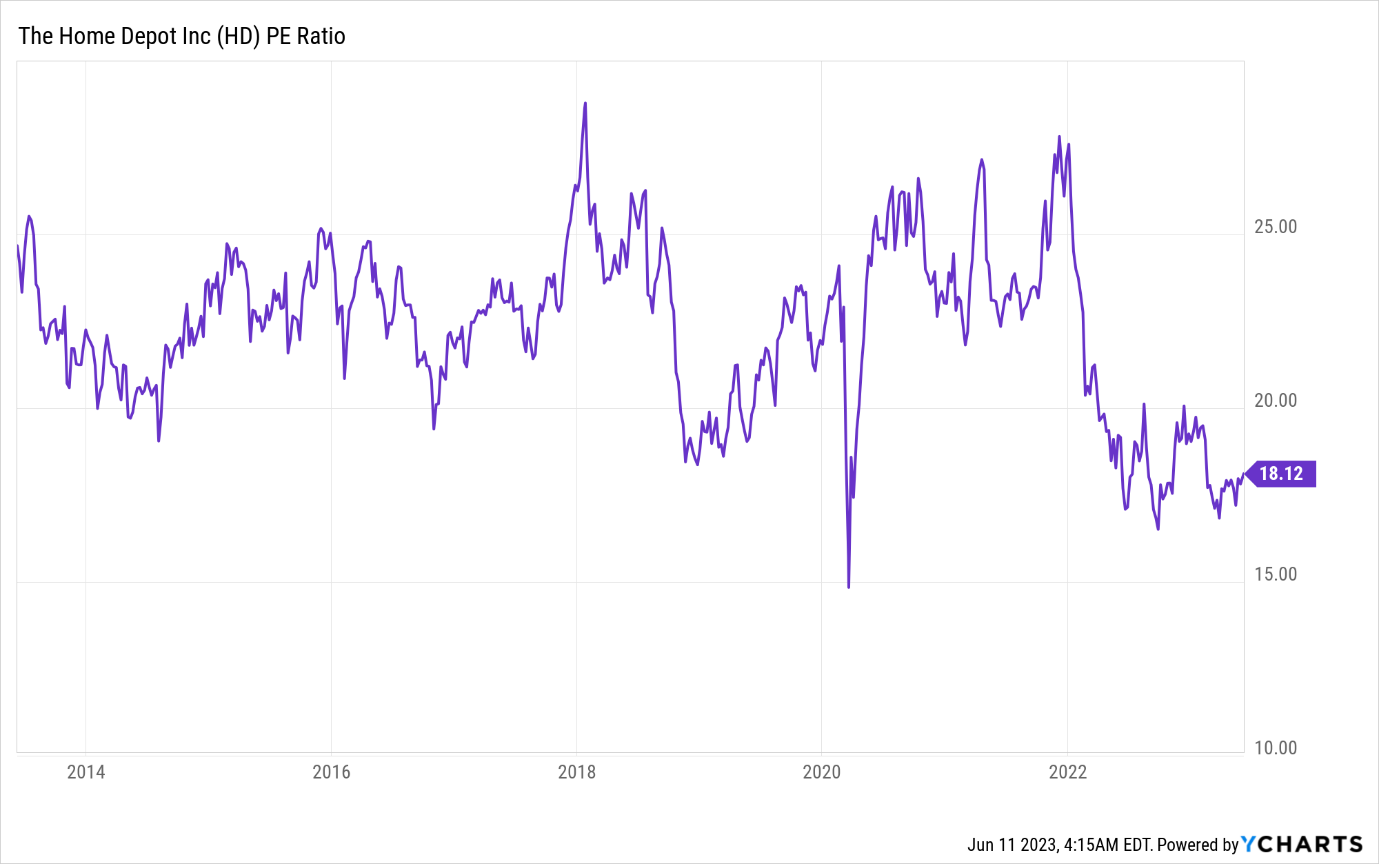

Home Depot (NYSE: HD)

Home Depot is the world’s largest home improvement retailer and operates 2,324 retail stores across 50 US states as well as Guam, 10 Canadian provinces, and Mexico.

Source: Y-Charts

The company’s shares have declined by 5% year to date and its price-to-earnings valuation is almost touching its lowest level in 10 years at 18.1 times.

Home Depot’s latest quarter ending 30 April 2023 saw net sales dip by 4.2% year on year to US$37.3 billion.

Net profit fell by 8.5% year on year because of higher finance costs and depreciation expenses.

An analysis of sales showed that customer transactions had declined by 4.8% year on year to 390.9 million, possibly due to high inflation in the US.

However, the average ticket size inched up 0.2% year on year to US$91.92.

Despite the weaker profit, Home Depot generated a positive free cash flow of US$4.7 billion, higher than the US$3 billion generated in the prior year.

Ted Decker, CEO of the company, remains positive on Home Depot’s long-term outlook and is confident that the company can grow its share in a large and fragmented market.

If you’re wondering about how you can leverage AI in your investment portfolio, and how it can boost your portfolio, good news! We just released an urgent Special Free Report to cover everything you need to know about AI and its implications for investors. Find out which listed companies are actively using AI to power their businesses and what you should do to prepare for the AI boom. Click here to download your free report now.

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclosure: Royston Yang owns shares of Adobe and PayPal.