According to a Forbes study, streaming services have become a staple in American households, with 99% of US households paying for at least one or more streaming services.

Taking a look at Netflix’s (NASDAQ: NFLX) subscription numbers, the three-year compound annual growth rate (CAGR) for paying subscribers in the USA and Canada stood at 3.7%.

This trend exists beyond the US.

Other regions, such as Latin America and the Asia Pacific, exhibit even stronger subscriber growth rates of 8% and 21.0%, respectively, highlighting the increasing global penetration of streaming media.

While the industry benefits from increased demand, it now also faces a challenge due to the need for competitive pricing and a diverse content slate.

Returning to the Forbes study, it was discovered that 45% of users in America cancelled a streaming service due to high cost.

Given the competitiveness of this industry, there are bound to be winners and losers.

This dynamic was further displayed by Bob Iger, CEO of Disney (NYSE: DIS), who attributed Disney Plus’s US$4 billion operating loss to over-aggressive expansion.

Here are two big winners of the streaming industry that you can consider adding to your buy watchlist.

Netflix

Netflix is the undisputed leader of the streaming industry.

Initially a DVD rental company, Netflix has successfully evolved with the entertainment industry and established itself as a pioneer in the online media streaming industry.

The company’s breakthrough year was 2013, marked by the success of the “Netflix Original Series”, propelling it to reach 50 million subscribers worldwide in 2014.

Now, the streaming provider has over 270 million paying subscribers, with a 10-year compound annual growth rate (CAGR) of 19.3%.

Subscriber growth was attributed to the introduction of new exclusive shows, such as “Berlin”, which attracted 56.7 million views, and the continuation of beloved series, such as “Avatar: The Last Airbender”, garnering over 63 million views.

Financial performance for the first quarter of fiscal year 2024 (1Q 2024) was impressive as well.

Revenue grew by 15.9% year on year, from US$8.2 billion to US$9.5 billion.

Net profit surged by over 78.7% year on year to US$2.3 billion.

Netflix also generated a positive free cash flow of US$2.1 billion for the quarter.

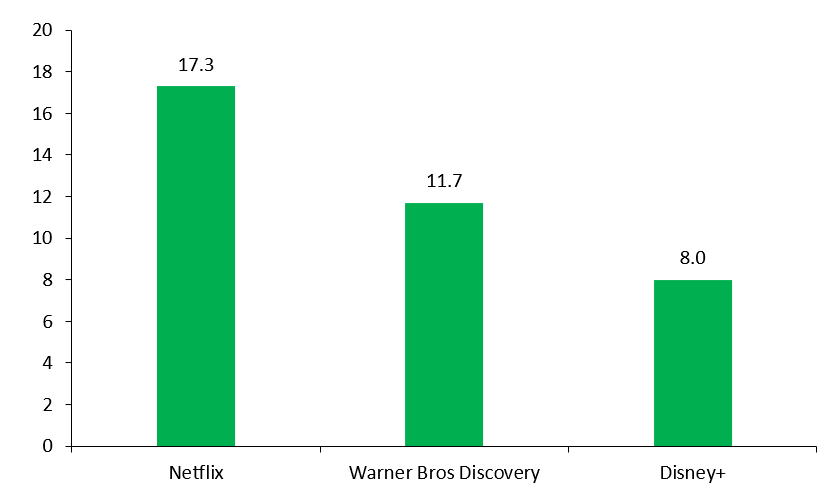

In terms of Average Revenue per User (ARPU), Netflix boasts one of the highest in its domestic market (USA and Canada). See the image below.

Source: Author’s Calculation

Quoting media veteran John Malone, “Scale is — very powerful when you’re producing something that has a high fixed and very low variable cost.”

Netflix’s operating margin is at an impressive 28.1%, significantly surpassing its largest competitor, Disney, with an operating margin of only 0.8% for its streaming business.

Armed with high operating margins and the highest ARPU among its competitors, Netflix is a very profitable business to invest in.

Netflix is planning to spend US$17 billion on content development this year, with the vast majority allocated to original content. ]

Several original TV series that users will be eagerly anticipating include “Arcane Season 2” in November this year and “Black Mirror Season 7” next year.

iQIYI (NASDAQ: IQ)

iQIYI is one of China’s leading providers of online entertainment video services.

It has carved out its own segment of market audience that are focused predominantly on Chinese films and series.

As a subsidiary of tech giant Baidu (SEHK: 9888), iQIYI is able to leverage Baidu’s existing technology to create a leading streaming platform powered by advanced AI, big data analytics and other core proprietary technologies.

As of 1Q 2024, iQIYI’s research and development accounted for only 5.4% of its total revenue. This is slightly lower than Netflix’s, which stood at 7.5%.

Unfortunately, iQIYI stopped reporting quarterly subscriber numbers and ARPU from 1Q 2024 onwards.

As of 2023, the Chinese streaming platform has amassed an average of 111.9 million subscribers.

The company reported US$1.1 billion in total revenue for 1Q 2024, a 5% year on year decrease.

Membership service revenue was US$664.6 million, a 13% year on year decline. This decline was largely due to exceptionally high revenue recorded in the same period the previous year.

However, net profit stood at US$90.8 million, a 6% increase year on year.

The company also generated a free cash flow of US$126.8 million.

iQIYI is focused on enhancing the use of AI to boost revenue received from its advertising services, which reached a historical high in 1Q 2024.

Its content distribution business has also achieved a historical high, highlighting its domestic popularity and the success of its original series.

Content distribution revenue hit a historical high this quarter and grew 27% year on year, highlighting the popularity of iQIYI’s original series among Chinese consumers.

Drama continues to be iQIYI’s best-performing category, maintaining the top position in viewership share for the past nine quarters.

We have just revealed the top 7 US tech stocks poised for remarkable growth. In today’s fast-paced market, betting on these giants could mean more money in your pocket. With a focus on solid fundamentals and innovative prowess, these selections should earn a place in your portfolio. Click here to grab your FREE report now and start investing in the future, today.

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclosure: Aw Kai Rui does not own any of the stocks mentioned in this article.