Singapore Exchange Limited (SGX: S68) or SGX has paid a dividend since its fiscal year 2001.

But I have only owned its stock since 2018.

SGX is in my personal portfolio for one key reason: its dividends. The stock exchange operator does have a long dividend track record. However, that alone does not guarantee that it will continue paying out a dividend.

Today, I would like to do a quick 3 step dividend health check-up to see whether I can count on SGX to continue paying me in the coming years.

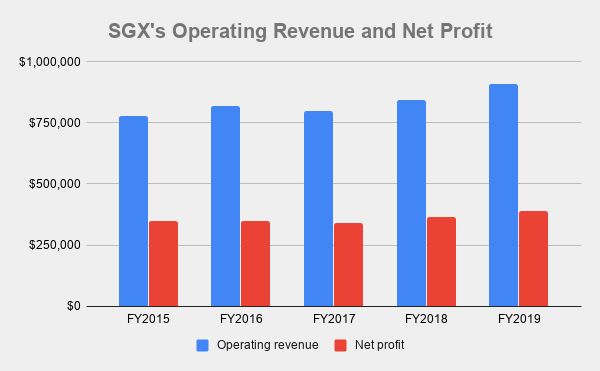

Check #1: Operating revenue and net profits

Revenue is the lifeblood of any company.

A business is only valid when there are dollars coming through its doors. SGX recorded solid sales growth between fiscal 2015 and fiscal 2019, as seen in the graph below.

Source: SGX earnings report and annual report

Much of the topline growth flowed down to the bottom line as well. Net profit grew by around 3% per year over the same five-year period.

Fiscal 2020’s first quarter was particularly strong with revenue growing by 19% and net profit soaring 25%.

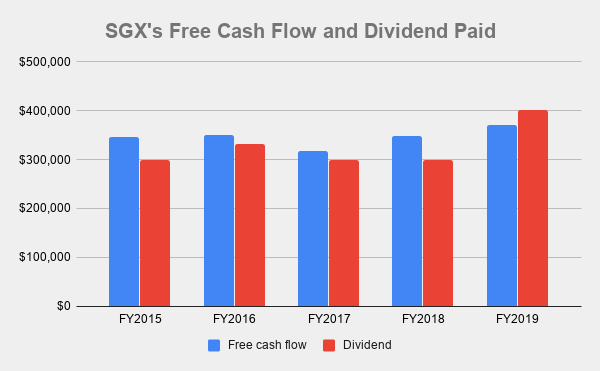

Check #2: Free Cash Flow

As the saying goes: revenue is vanity, profit is sanity, and cash is reality.

Dividends payouts are at its most reliable when they are funded by cold, hard cash.

Source: SGX earnings report and annual report

For the most part, the cash flow that is flowing into SGX has exceeded the dollars needed to support its dividend. The only exception is fiscal 2019 where free cash flow fell short.

I am not worried, though.

In the first quarter of fiscal 2020, SGX generated almost S$110 million in free cash flow and plans to pay out about S$80 million in dividends. So, its dividend continues to be well-funded.

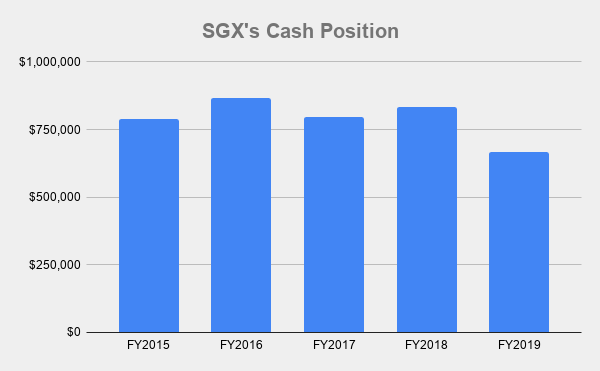

Check #3 Cash in the bank

The final pit-stop is an inspection of the cash on SGX’s balance sheet.

Source: SGX earnings report and annual report

SGX maintains a rock-solid balance sheet with an average cash position of S$790 million between fiscal 2015 and fiscal 2019.

To be sure, there was a minor dip in fiscal 2019. However, as of 30 September 2019, SGX’s cash position has moved back up to about S$786 million.

Get Smart: Business and financials, together

There are two major stock market trends happening around the world.

For one, start-up companies are remaining private longer compared to the past.

Case to point: When Amazon.com (NASDAQ: AMZN) came public in 1997, the online retailer was valued at around US$440 million. In 2004, Google filed for its IPO and had a market cap of US$23 billion. And by the time Facebook (NASDAQ: FB) debuted in the stock market, the company had a price tag of over US$100 billion.

At the same time, the pool of companies listed is shrinking. SGX is no exception. It’s getting harder to attract companies to get listed in Singapore.

Against this backdrop, CEO Loh Boon Chye is re-positioning SGX as an international multi-asset exchange. SGX has also found some success in areas such as China index derivatives, iron ore trading, and REITs.

For me, the company’s move appears to mirror that of the wealth management industry which is demanding a wider range of financial products from around the world.

The world is digitising. The playing ground may expand — but the competition that is coming could global or regional. Remaining relevant is key, and that is what I would like to see SGX do.

If you’d like to learn more investing concepts, and how to apply them to your investing needs, sign up for our free investing education newsletter, Get Smart! Click HERE to sign up now.

None of the information in this article can be constituted as financial, investment, or other professional advice. It is only intended to provide education. Speak with a professional before making important decisions about your money, your professional life, or even your personal life. Disclosure: Chin Hui Leong owns shares of Singapore Exchange, Amazon, Alphabet and Facebook.